Meta Platforms Will Be a $2 Trillion Company On This Date

May 24, 2026

Meta Platforms (NASDAQ:META | META Price Prediction | META Price Prediction) delivered a strong earnings beat, yet shares drift lower. Q1 2026 revenue jumped 33.08% to $56.311 billion, EPS came in at $10.44 versus a $6.6587 estimate, and CEO Mark Zuckerberg said the company is “on track to deliver personal superintelligence to billions of people.”

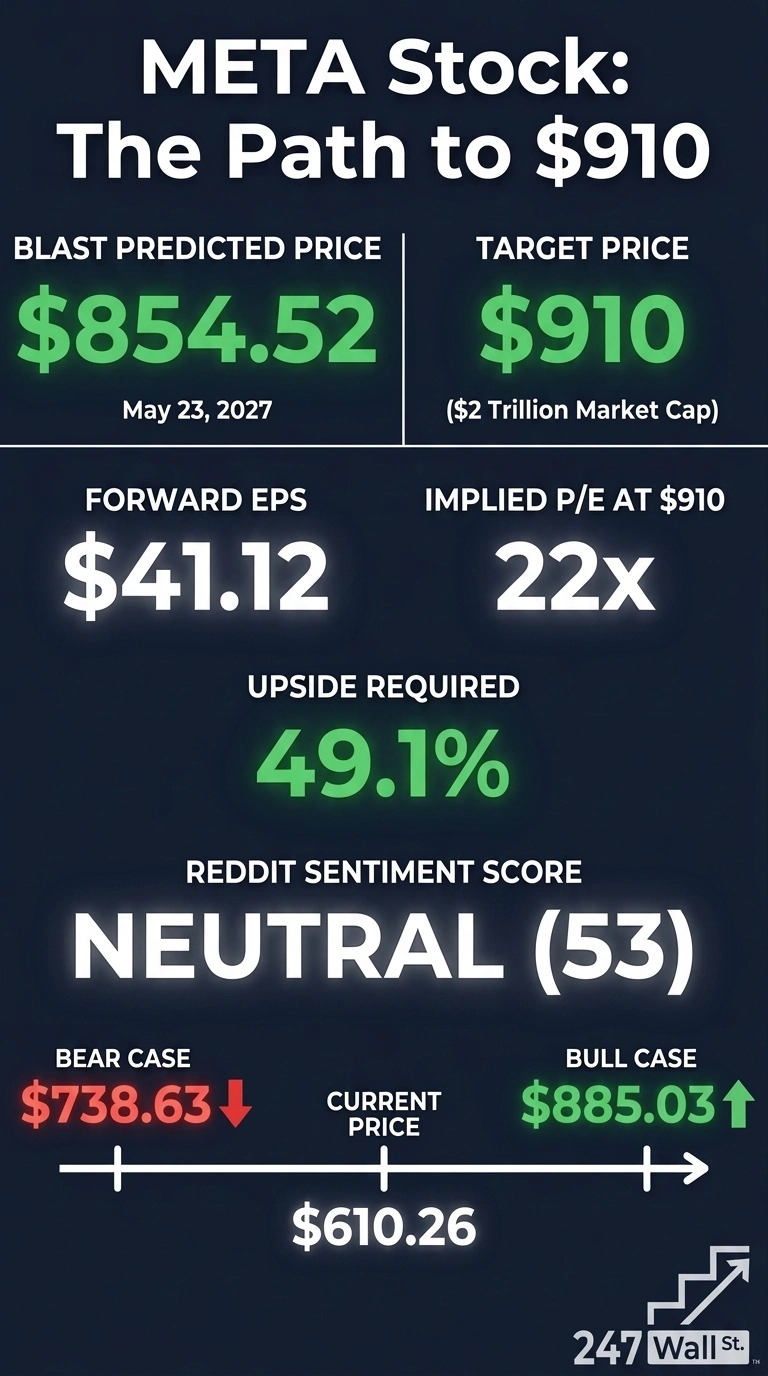

Shares trade at $610.26 with a market cap of $1.549 trillion. Can Meta clear $910 per share, the level that turns it into a $2 trillion company, by 2027?

Why Meta Shares Are Stuck Despite Strong Revenue Growth

The disconnect is striking. Meta is down 7.47% year to date, down 9.55% over the past month, and flat over one week.

Management raised full-year 2026 capital expenditures to $125 to $145 billion, up from $115 to $135 billion, with total expenses at $162 to $169 billion. Investors saw expenses up 35% year over year, a $4.03 billion Reality Labs operating loss, and youth litigation trials ahead, and took profits. The stock dropped from $671.77 at the earnings filing to $608.745 the next day. A great business is being punished for spending aggressively on AI.

Wall Street Sees 35% Upside. Our Model Says 40%

Wall Street is firmly bullish. The consensus target sits at $826.60 with 9 Strong Buys, 47 Buys, 7 Holds, and zero Sells. Our base case at 24/7 Wall St. lands at $854.52, implying 40.03% upside, with a bull case of $885.03 and a bear case of $738.63.

With 89% of analysts bullish and quarterly earnings growth running at 62.4% year over year, even consensus looks conservative. The Street is anchoring to last year’s multiple instead of next year’s earnings.

The Path to $910 Per Share

Reaching $910 from today’s price of $610.26 requires a 49.1% gain. At 2.196 billion shares outstanding, that price tags Meta at roughly $2 trillion. With forward EPS of $41.12, a price of $910 implies a forward P/E of 22x. Our base case of $854.52 already implies 18x, meaning the target requires 4x additional multiple expansion.

That is achievable. Meta trades at a trailing P/E of just 22 while compounding earnings at 62.4%. Catalysts are concrete. Family of Apps daily active people hit 3.56 billion, ad impressions rose 19%, and price per ad climbed 12%.

Zuckerberg called Q1 “a milestone quarter with strong momentum across our apps and the release of our first model from Meta Superintelligence Labs.” The single biggest risk: if AI capex fails to translate into incremental advertising revenue or new product monetization by 2027, multiple expansion stalls.

Where Meta Trades Today vs Its Earnings Power

At $610.26 against forward EPS of $41.12, the stock trades at roughly 15x forward earnings. That is cheap for a business growing earnings 62.4% and posting operating margins of 40.6%. Shares sit between a 52-week high of $794.38 and a low of $520.26. Meta is up 422.52% over ten years. Today’s compressed multiple, paired with accelerating EPS, is exactly the kind of setup that re-rates when sentiment shifts.

Is $910 Realistic?

Hitting $910 by 2027 requires a 49.1% gain, putting Meta at roughly $2 trillion.

Three things need to go right: ad pricing must keep compounding above 10%, Reality Labs losses need to stabilize rather than balloon further from $4.03 billion per quarter, and Meta Superintelligence Labs needs at least one monetizable product. A regulatory penalty or youth litigation loss would derail it. We’ve outlined the blueprint for how Meta could reach $910 in 2027.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}