Do Green Bonds Work?

September 30, 2024

New research finds that relatively few green bonds initiate novel low-carbon projects.

It certainly sounds like a good idea. By putting money into a green bond, an investor supports renewable energy, energy efficiency and other low-carbon projects.

“Financial markets can help solve the climate challenge by meeting the growing demand for low-carbon projects around the world…New financial tools like green bonds are helping drive more capital to these projects.” –Michael Bloomberg

But do green bonds actually drive capital to novel low-carbon projects? Over $3 trillion in green bonds have been issued to date, so this is important to understand.

For today’s post, I want to dig into a new working paper by NYU researchers Pauline Lam and Jeffrey Wurgler that looks closely at a decade of evidence from U.S. corporate and municipal green bonds. Their results are sobering and, in my view, raise important questions about whether green bonds are doing what we think they are doing.

—

What Does the Paper Do?

A bond is a loan taken out by a company, government, or other issuer. An investor buys the bond and, in exchange, the issuer pays interest at predetermined intervals and then returns the loan to the investor at the maturity date. Green bonds are just the same as traditional bonds except the money goes toward green projects.

There is no universally accepted standard for what is considered a “green” project so part of the goal for Lam and Wurgler is to try to better understand how the money from green bonds is being used. Going line-by-line through company reports, SEC filings, company websites, direct correspondence, and other sources, they reviewed and categorized 100+ recent green bonds.

To narrow their focus, they looked only at the first green bond from each issuer. This focus on “first-issues” was in part by necessity because their approach is so time-intensive, but also because these bonds tend to be better documented than subsequent issues.

Their dataset goes from 2013 to 2022, but for most issuers the first green bond occurred sometime in 2019, 2020, or 2021. The average corporate green bond in their dataset is for $580 million with a maturity of 10 years and annual yield of 2.4%. The average municipal green bond in their dataset is smaller (about $90 million) with a somewhat longer maturity (12 years), and 2.1% yield (municipal bonds tend to have tax advantages).

—

Categorizing Green Bonds

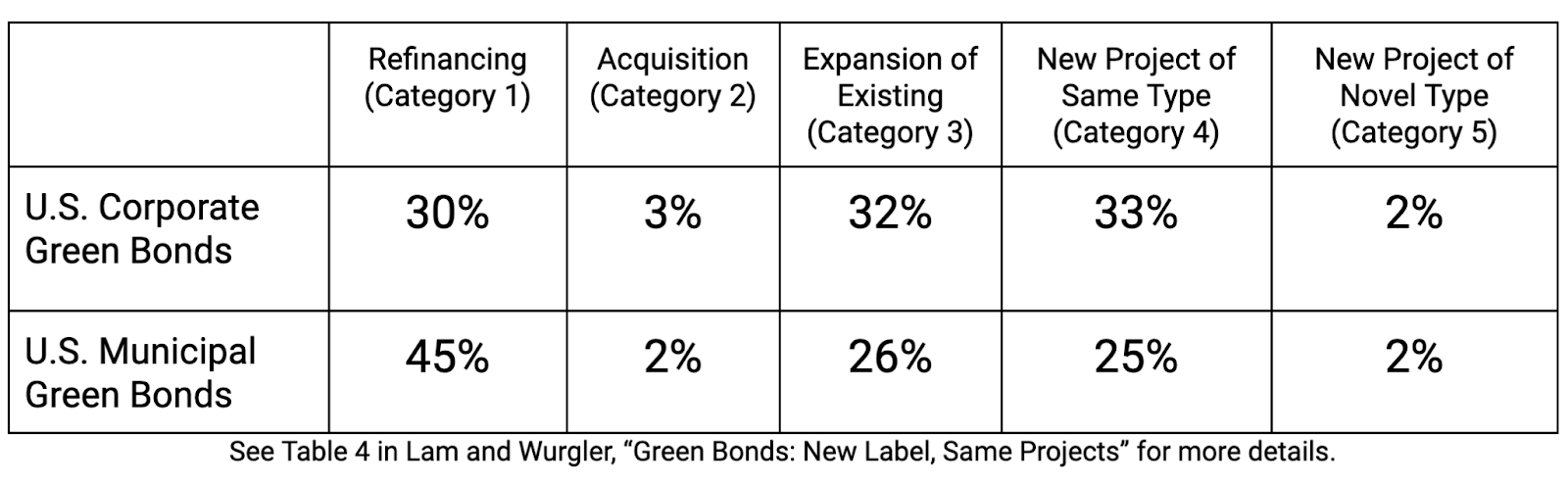

Lam and Wurgler classified each green bond into one of five categories based on what they call “project additionality”. Here are the five categories along with examples:

- Refinancing. In 2019, Piedmont Operating Partnership issued a green bond to repay debt, including debt related to Galleria Office Towers, a LEED Certified building.

- Acquisition. In 2016, Ramsey County issued a green bond to acquire an existing resource recovery facility from another county, highlighting the environmental benefits associated with waste management.

- Expansion of Existing Project. In 2018, Duke Energy issued a green bond for solar projects under construction or already operating.

- New Project of Same Type. In 2020, Analog Devices issued a green bond for a new LEED certified building similar to an existing building owned by the company.

- New Project of Novel Type. In 2022, Amgen issued a green bond for an electric vehicle pilot program.

For the purposes of the blog, I’ve provided only highly-stylized examples but the working paper has much more detail about their approach and additional detail about these and other examples.

Before continuing, I want you to guess what percentage of green bonds fall into these five categories. Keep in mind that from the perspective of driving new capital into green projects, we would like to see a lot of category 5.

—

Main Results

Lam and Wurgler find the opposite. The biggest takeaway from the paper is that only 2% of green bonds go to new projects of a novel type (category 5). As the table below illustrates, this is true for both corporate and municipal bonds.

Instead, most of the money goes to less new, less novel purposes. They find that a large percentage of green bonds go for refinancing (category 1). I found this pretty surprising. I suppose the justification is to emphasize to investors that the issuer was already “green” but I don’t think this is what Michael Bloomberg has in mind when he talks about green bonds driving capital to low-carbon projects.

In addition, more than half of green bonds go to expansion of existing projects (category 3) and new projects of the same type (category 4). Both categories indicate a high risk of being non-additional, that is, green bonds going for projects that would have happened otherwise. The title of Lam and Wurgler’s paper is “Green Bonds: New Label, Same Projects” and, unfortunately, it does seem like a lot of these bonds are more about labeling than innovation. Keep in mind also that these are first-issues, so these are the green bonds that are likely most scrutinized, best documented, and – one might have thought – most likely to coincide with a new direction for the issuer.

The authors then go on to test whether investors differentiate between more-additional and less-additional bonds. They find no evidence for a premium for bonds that finance more clearly additional projects. Nor is there a larger stock market bounce for a company when it announces green bonds to pay for projects that are more additional. Nor do green exchange traded funds (ETFs) tilt toward more-additional bonds. In short, they find no evidence that investors know or care about additionality.

—

Takeaway

The results point to a disconnect between theory and practice. In theory, green bonds are driving capital toward novel green projects, providing a crucial financial mechanism for the innovations needed for the energy transition. In practice, however, green bonds seem to be going mostly for business as usual. There are some truly novel projects, but the lion’s share of financing seems to be mostly relabeling what was already happening.

It is also worth highlighting that none of this addresses the question of enforcement. Other researchers have written about the potential for abuse of green bonds. For example, that an issuer does a bait-and-switch, claiming that the proceeds will be for some green project, only to later use the proceeds for a non-green project. This enforcement issue is a completely different and separate issue, but raises further questions about whether green bonds are doing what we think they are doing.

More research is needed. I’m a big fan of Lam and Wurgler’s labor-intensive bond-by-bond approach but they, admittedly, are able to examine only a small fraction of the enormous global green bond market. I’m sure they would welcome other researchers performing similar studies in other countries, other time periods, and with related financing mechanisms.

—

Follow us on Bluesky and LinkedIn, and subscribe to our email list to keep up with future content and announcements.

Suggested citation: Davis, Lucas. “Do Green Bonds Work?” Energy Institute Blog, September 30, 2024, https://energyathaas.wordpress.com/2024/09/30/do-green-bonds-work/

—

By default comments are displayed as anonymous, but if you are comfortable doing so, we encourage you to sign your comments.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}