1 Growth Stock Down 20% to Buy Right Now

December 1, 2025

The market is getting nervous about Meta’s spending plans.

Although the market is just off its all-time high, you wouldn’t know it based on some of the fear in one part of the market. There is talk of a bubble forming in artificial intelligence (AI), fueled by huge spending on the technology.

One stock that has seen the brunt of the market’s worry about hefty AI spending is Meta Platforms (META 1.26%). The company is starting to extend itself a bit by spending more money than its cash flows are providing, requiring it to take on debt to fund its aspirations. This has the market extremely concerned, which is why the stock was about 20% off its all-time high.

However, I think right now is an excellent buying opportunity, and long-term investors will be able to benefit from Meta’s build-out plans a few years down the road, making today’s stock price a bargain.

Image source: Getty Images.

Meta Platforms is using AI to improve its ad business

Meta is the parent company of multiple social media sites, including Facebook (its former company name) and Instagram. The company also has a Reality Labs division that’s focused on bringing augmented reality and virtual reality devices to the consumer, although this segment has been a money pit. Management spends far more on this division than it generates, but it’s more than made up for by its strong ad business.

In the third quarter, $50.1 billion of its $51.2 billion in total revenue came from ads. The Family of Apps division (which encompasses the ad revenue) generated $25 billion in operating profits, while Reality Labs lost $4.4 billion.

However, if the company can launch a product that incorporates generative AI into an everyday device that’s not a computer or cellphone, as with the smart glasses it’s developing, the fortunes of the Reality Labs division could flip. But there’s no guarantee of that.

Meta Platforms

Today’s Change

(-1.26%) $-8.18

Current Price

$639.77

The backbone of the business will likely always be its social media platforms, and it has already seen improvements from AI. CEO Mark Zuckerberg said the technology has caused users to spend 5% more time on Facebook and led to better ad conversions. This has led to revenue rising 26% year over year in the third quarter.

Few companies of Meta’s size can claim such rapid growth, making it one of the top growth stocks in the market. The problem is, Wall Street isn’t happy with its spending plans.

Spending big on AI infrastructure

Meta plans on $70 billion to $72 billion in capital expenditures (capex) during 2025, mostly centered around data center construction. For 2026, it expects the dollar amount to be significantly higher than it was from 2024 to 2025. With capex totaling $39.2 billion in 2024, that indicates 2026’s figure will be more than $100 billion.

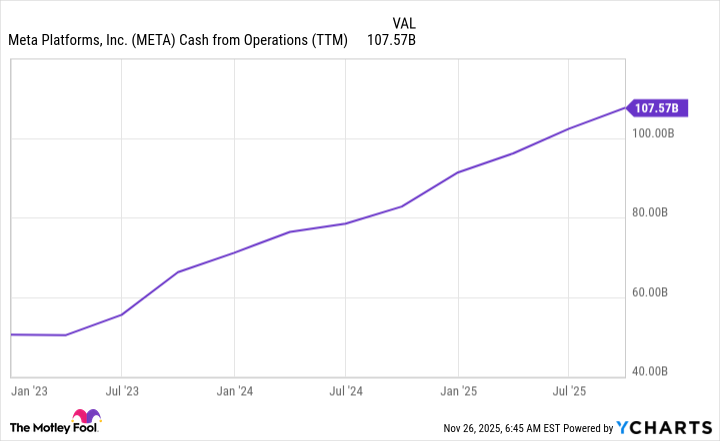

Over the past 12 months, the business generated about $107 billion in cash from operations. This means that its capex plans will consume nearly all of the cash it generates.

META Cash from Operations (TTM), data by YCharts; TTM = trailing 12 months.

That’s a red flag for the market and is why the stock is down so much. However, management may have a plan to cut costs. Recently, a report surfaced that said Meta was in talks with Alphabet to buy Alphabet’s tensor processing units (TPUs). These are specialized chips that can compete with Nvidia‘s graphics processing units (GPUs) at a lower price point, but at the cost of flexibility.

If it buys TPUs from Alphabet, Meta could get more computing power at a lower price or lower the expected cost of its data center construction. Either way, this development could be a big deal for Meta.

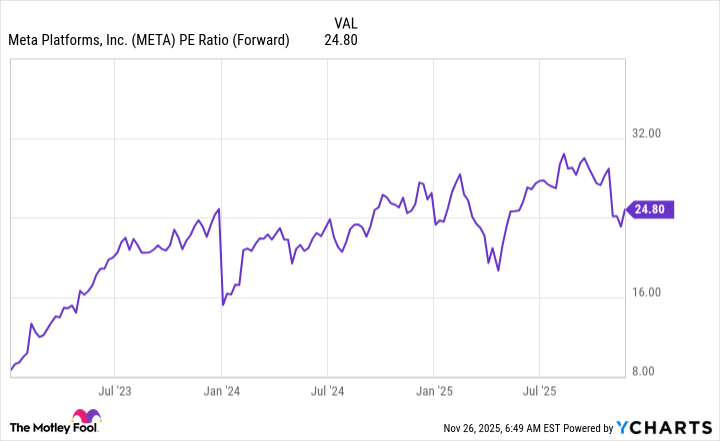

Despite this positive news, its stock has barely budged and trades for 25 times forward earnings.

META PE Ratio (Forward) data by YCharts; PE = price to earnings.

That’s not necessarily cheap, but it is cheaper than it was over recent months. I think the market will come around to the stock in 2026, as some payoff from AI spending may be realized. Even if it doesn’t, the spending will eventually decrease, and Meta will go back to being the monster cash-flow machine it has always been.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}