2 Undervalued, High-Quality Companies to Buy in 2026 and Hold Forever

January 20, 2026

Meta Platforms and Walt Disney are compelling buys for value investors in the new year.

At its core, long-term investing is all about finding quality companies, buying them for reasonable prices, and letting gains compound over time. But many top growth stocks fetch premium valuations — especially after three consecutive years of more than 15% gains in the S&P 500.

Granted, some of these leaders can grow into their valuations over time. But investors looking for stocks trading at a discount to the S&P 500 may have to venture beyond high-profile artificial intelligence (AI) names.

Here’s why Meta Platforms (META 2.64%) and Walt Disney (DIS 0.62%) stand out as two undervalued stocks to buy in January.

Image source: Getty Images.

This “Magnificent Seven” stock is a bargain

Meta Platforms generates most of its revenue from advertising on its Family of Apps (Instagram, Facebook, WhatsApp, and Messenger). For the three months ended Sept. 30, 2025, Family of Apps generated $50.08 billion in advertising revenue and $24.97 billion in operating income — for an operating margin of 49.9%.

To illustrate just how elite that is, consider that Alphabet‘s Google Services (which consists of Google Search, YouTube ads, Google Network, and Google subscriptions, platforms, and devices) generated $87.05 billion in revenue for the three months ended Sept. 30, 2025 and $33.53 billion in operating income for an operating margin of 38.5%.

Advertisement

Meta has done a masterful job of boosting engagement through curated short-form video content and targeted ads, making it an appealing destination for ad spending. Its Family of Apps is truly one of the best business models on the planet. So you may be wondering why investors have soured on the stock, with Meta down 12.6% in the last six months compared to an 11.2% gain in the S&P 500.

Meta Platforms

Today’s Change

(-2.64%) $-16.37

Current Price

$603.88

Meta has a lot of moving parts outside its core Family of Apps that have investors on edge. It continues to burn through money with Reality Labs, which reported an operating loss of $13.17 billion for the nine months ended Sept. 30, 2025.

Reality Labs consists of metaverse investments, the Meta Quest headset, Ray-Ban Meta smart glasses, AI research, and other virtual reality/augmented reality bets. It’s basically Meta’s massively unprofitable research and development arm, which the market tolerates because Family of Apps is so profitable. But Meta could soon strain its margins because of its massive AI spending.

Meta owns and operates its own network of data centers and works with public clouds. Meta’s AI and data center budget is ballooning as it delivers AI features like Meta AI assistants across its Family of Apps and builds out its Llama 4 AI models.

In its third-quarter earnings release, Meta boosted its 2025 capital expenditure (capex) guidance from a range of $66 billion to $72 billion to a new range of $70 billion to $72 billion. Just three years ago in 2022, Meta spent $32.04 billion in capex.

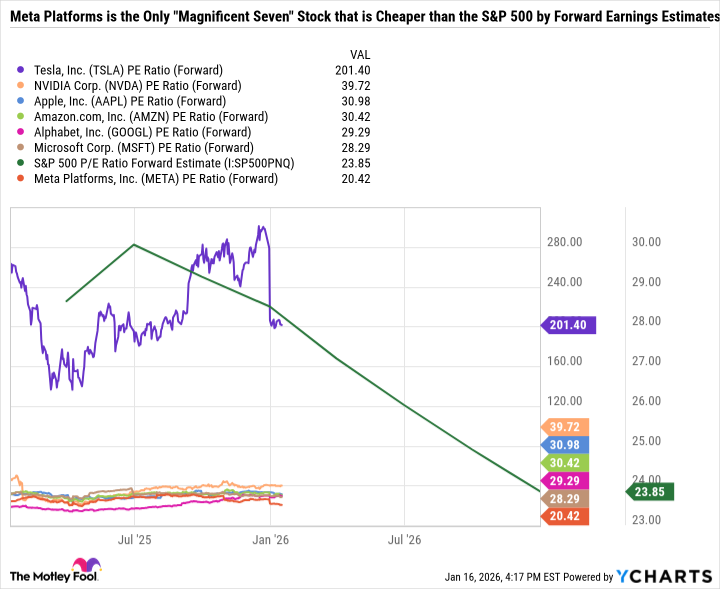

Meta can afford to swing for the fences on AI thanks to its high margins and cash flow. Meta’s risks are already reflected in its valuation, as it is the least expensive Magnificent Seven stock by forward earnings and the only one trading at a discount to the S&P 500.

TSLA PE Ratio (Forward) data by YCharts

Disney has become too cheap to ignore

Disney’s latest animated feature, Zootopia 2, just surpassed Frozen 2 to become Walt Disney Animation Studios’ highest-grossing film, with global box office earnings of $1.46 billion as of 2025’s end. Disney is overcoming the narrative that its creative days are behind it, with several box office hits in recent years, from Zootopia 2 to Inside Out 2.

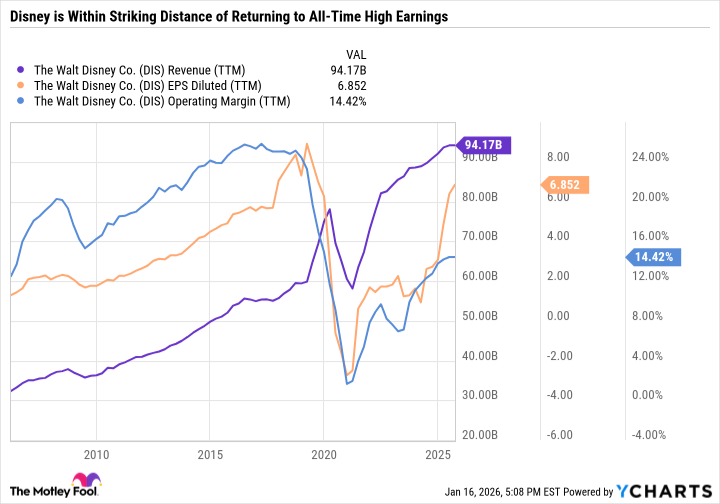

This is big news for Disney, which endured a box office glut that started roughly after Avengers: Endgame in 2019 and carried forward until 2025. Part of the issue was the COVID-19 pandemic, but the bigger problem was an overabundance of Marvel and Star Wars films. As you can see in the following chart, Disney’s earnings are still below pre-pandemic highs, but have dramatically improved in recent years thanks to rising revenue and margins

DIS Revenue (TTM) data by YCharts

At just 16.8 times forward earnings, Disney is looking like an impeccable bargain for long-term investors. It is back in a box office groove that is likely to keep on rolling with the highly anticipated releases of Avengers: Doomsday and Toy Story 5 later this year. Disney+ is now consistently profitable, and the Parks and Experiences segment continues to boom despite pullbacks in consumer spending.

Disney is investing its most profitable ideas with a blend of streaming and theatrical release content, global park renovations and expansions, the opening of Disneyland Abu Dhabi (roughly in the early 2030s) and the possibility of a fifth theme park at Walt Disney World after 2035.

Walt Disney

Today’s Change

(-0.62%) $-0.69

Current Price

$110.51

Disney is firing on all cylinders, which should help its earnings and margins improve and more than offset declines from its linear networks (cable) business. Netflix‘s big bet on Warner Bros. Discovery showcases the importance of intellectual property in streaming and entertainment, which Disney has in spades.

Throw in a modest 1.3% dividend yield, and Disney looks like one of the best value stocks for investors to scoop up in January.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}