Energy Transition Market

March 4, 2025

Quick Navigation

Report Overview

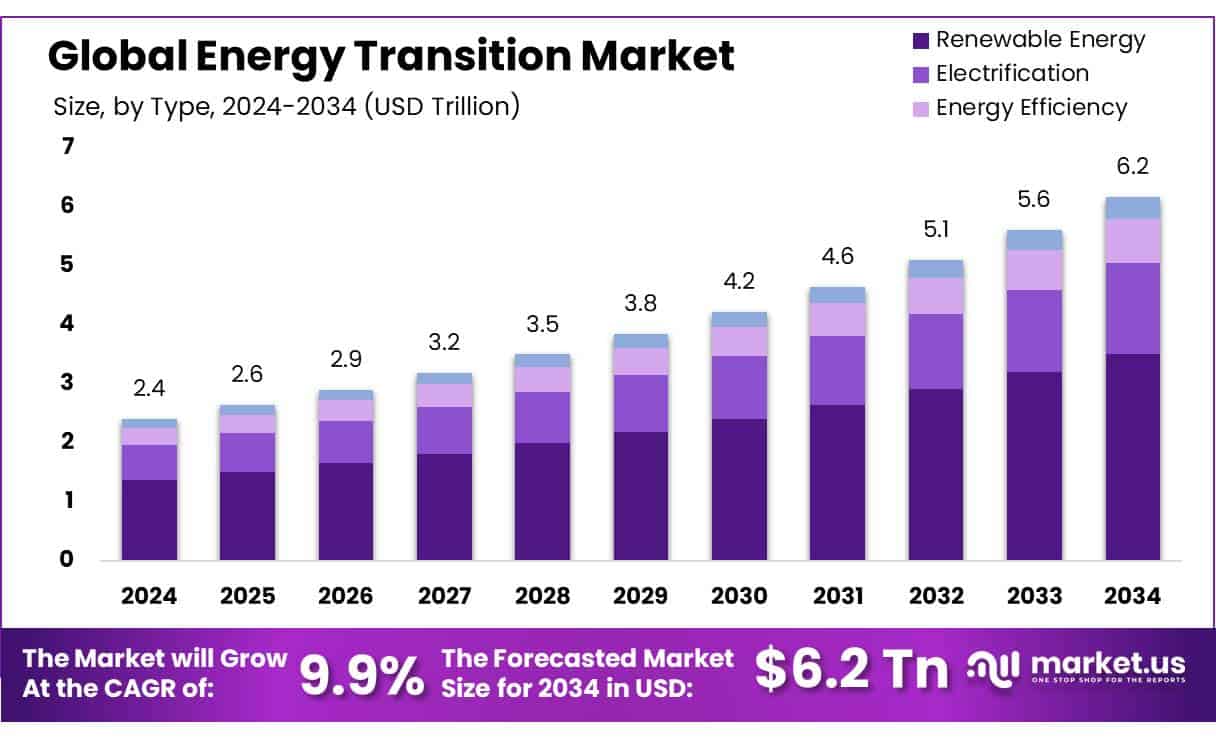

The Global Energy Transition Market size is expected to be worth around USD 6.2 Tn by 2034, from USD 2.4 Tn in 2024, growing at a CAGR of 9.9% during the forecast period from 2025 to 2034.

The Energy Transition Market, critical to this transformation, encompasses the shift from non-renewable sources of energy like oil, coal, and natural gas to renewable sources such as wind, solar, and hydroelectric energy. This transition is not merely a technological overhaul but a comprehensive socio-economic challenge that integrates advances in energy efficiency, the incorporation of renewable resources, and the development of supportive infrastructure like smart grids and energy storage solutions.

The technological advancements and a strong legislative framework advocating for greener policies. According to the International Energy Agency (IEA), renewable energy technologies are set to account for almost 95% of the net increase in global power capacity through 2026. Solar and wind energy lead this expansion, indicative of a broader trend towards decentralization and digitization of energy systems.

Government initiatives continue to play a crucial role in shaping the market. For instance, the European Union’s Green Deal and the United States’ renewed commitments to rejoin the Paris Agreement underpin robust governmental support, driving forward the global agenda for an energy-efficient, sustainable future.

Significant investments are funneling into the sector, with global spending on energy transition technologies projected to exceed $500 billion annually. This investment is spurred by both private sector innovation and public sector funding, demonstrating a unified approach towards achieving the objectives laid out in international agreements like the Paris Accord.

Key Takeaways

- Energy Transition Market is anticipated to expand from USD 2.4 trillion in 2024 to approximately USD 6.2 trillion by 2034, reflecting a (CAGR) of 9.9%.

- Renewable Energy dominated the market in 2024, accounting for over 57.3% of the market share.

- Energy Storage Systems accounted for 42.7% of the market share in 2024, highlighting their essential role in managing the intermittency of renewable energy sources and ensuring consistent grid stability.

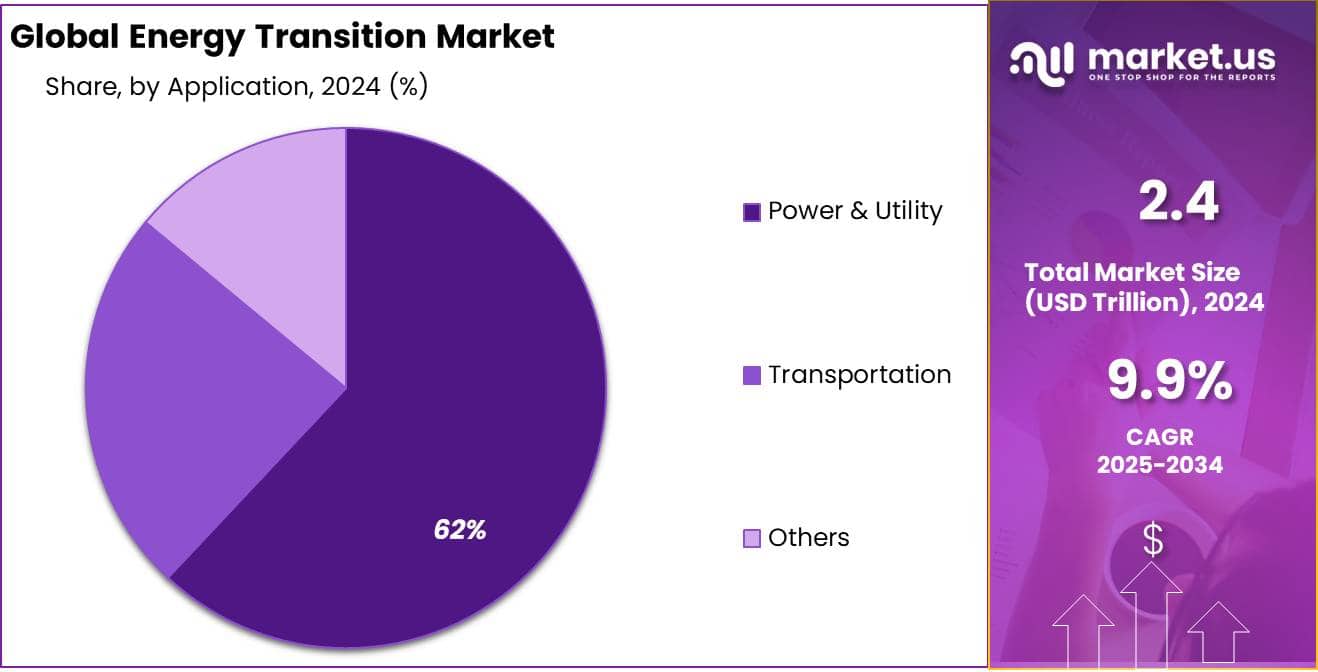

- The Power & Utility sector captured more than 62.3% of the market share in 2024, underlining its significant contributions to adopting and integrating renewable technologies into the energy grid.

- In 2024, the Asia-Pacific region led the Energy Transition Market with a 46.1% share, equivalent to around USD 1.1 trillion.

By Type

In 2024, Renewable Energy held a dominant market position, capturing more than a 57.3% share of the Energy Transition Market. This significant portion reflects a growing commitment from both governments and private sectors to reduce reliance on fossil fuels and combat climate change. The surge in renewable energy investments can be attributed to technological advancements and more favorable policy frameworks, which have collectively improved the efficiency and cost-effectiveness of renewable resources like solar, wind, and hydro power.

The year witnessed a marked increase in the installation of wind farms and solar panels, driven by their decreasing cost and more robust infrastructure support. This trend is indicative of the sector’s rapid evolution and its critical role in shaping a sustainable energy future. As the market expands, renewable energy’s share is projected to increase further, highlighting its pivotal role in the global strategy towards energy transition. This shift not only supports environmental goals but also stimulates economic growth by creating jobs in new and emerging sectors of the energy market.

By Technology

In 2024, Energy Storage Systems held a dominant market position, capturing more than a 42.7% share of the Energy Transition Market. This substantial share underscores the critical role that storage technologies play in integrating renewable energy sources into the grid effectively. The need for robust energy storage solutions has grown exponentially as fluctuations in renewable energy production require balancing to maintain grid stability.

Throughout the year, advancements in battery technologies, particularly lithium-ion and alternative chemistries like solid-state batteries, have driven market growth. These developments have helped improve the efficiency, safety, and lifespan of storage systems, making them more attractive for both commercial and residential applications. As renewable energy deployment increases, the demand for energy storage is expected to rise, ensuring a steady growth trajectory for this segment of the market. This trend highlights the essential nature of energy storage systems in achieving a sustainable and resilient energy future.

By Application

In 2024, Power & Utility held a dominant market position, capturing more than a 62.3% share of the Energy Transition Market. This segment’s strong performance reflects its crucial role in the shift toward sustainable energy sources. Utilities are increasingly investing in renewable energy projects and upgrading their infrastructure to support the integration of these new technologies into the energy grid.

The focus has been on enhancing grid capacity and flexibility to accommodate a higher proportion of renewable energy, like wind and solar, which can vary in output depending on weather conditions. This adaptation is essential for maintaining reliability and stability in power supply as the sector moves away from traditional fossil fuels. The ongoing developments in smart grid technology and energy management systems also support this transition, enabling more efficient distribution and consumption of power.

Key Market Segments

By Type

- Renewable Energy

- Electrification

- Energy Efficiency

- Others

By Technology

- Energy Storage Systems

- Electric Vehicles (EVs)

- Smart Grids

- Carbon Capture and Storage (CCS)

- Others

By Application

- Power & Utility

- Transportation

- Others

Drivers

Government Policies Propel Renewable Energy Growth

One of the primary driving factors for the energy transition is the enactment of supportive government policies and regulations aimed at reducing carbon emissions. These initiatives are critical as they provide both the framework and financial support necessary for the development and adoption of renewable energy technologies.

For instance, the European Union’s ambitious Green Deal aims to make Europe the first climate-neutral continent by 2050. This initiative includes significant funding for renewable energy projects and infrastructure improvements, demonstrating a strong commitment to transitioning away from fossil fuels. According to the European Commission, the EU plans to double its renewable energy capacity by 2030, which represents a major push toward meeting these goals.

In the United States, the Department of Energy has launched various programs to accelerate the adoption of clean energy. One notable initiative is the Solar Energy Technologies Office’s investments, which aim to cut solar costs by half again by 2030, making solar energy more accessible and affordable for a broader range of consumers and businesses. These targeted investments are part of a broader strategy to support the U.S.’s goal of achieving a 100% clean electricity sector by 2035, as outlined by the Biden administration.

Such policies not only encourage the growth of renewable energy sectors but also stimulate economic activity through job creation in new industries. Furthermore, they play a crucial role in enhancing national energy security by reducing dependence on imported fuels. With governments around the world setting more aggressive targets for reducing greenhouse gas emissions, the drive towards renewables is expected to continue gaining momentum, making it a pivotal time for the energy transition.

Restraints

High Initial Costs Impede Energy Transition Progress

A major restraining factor in the energy transition is the high initial costs associated with deploying renewable energy technologies. These costs include not only the installation of equipment like solar panels and wind turbines but also the necessary upgrades to existing infrastructure to accommodate these new energy sources.

For example, while the price of solar photovoltaic (PV) panels has dropped significantly over the past decade, the overall cost of setting up a comprehensive solar power system remains substantial. These expenses can be prohibitive for smaller businesses and residential areas, especially in less economically developed regions. The initial investment required for renewable energy systems often involves not just the technology itself but also land acquisition, grid connection, and potential upgrades to ensure compatibility with current systems.

The International Renewable Energy Agency (IRENA) highlights that while renewable energy costs have been decreasing, the financial barriers still pose significant challenges for widespread adoption. In their report, IRENA points out that achieving a lower cost threshold is essential for more extensive deployment, especially in emerging markets where funding is not as readily available.

Moreover, the integration of renewable energy sources into national grids requires substantial investment in smart grid technologies, which are crucial for managing the variability and decentralization of renewable energy. This adds another layer of expense that can slow down the pace of energy transition.

These financial hurdles are acknowledged by governments worldwide, prompting initiatives to subsidize the cost and provide incentives for renewable energy adoption. Despite these efforts, the high upfront costs remain a significant barrier, necessitating continued innovation and financial strategies to lower these barriers and make renewable energy more accessible to a broader audience. Without addressing these economic challenges, the transition to a sustainable energy future may be slower than needed to meet global climate goals.

Opportunity

Electrification of Transportation: A Catalyst for Energy Transition

A significant growth opportunity within the energy transition is the electrification of the transportation sector. This shift not only helps reduce greenhouse gas emissions but also increases the demand for renewable energy sources, creating a substantial push toward a more sustainable energy economy.

The transportation sector, traditionally reliant on fossil fuels, is a major contributor to carbon emissions globally. However, the recent surge in electric vehicle (EV) adoption is setting the stage for transformative changes. For instance, the International Energy Agency (IEA) reports that the global EV market has been growing rapidly, with sales doubling in the past year alone. This trend is expected to continue, driven by advancements in battery technology, decreasing costs, and increasing consumer preference for sustainable alternatives.

Governments worldwide are supporting this shift through various incentives and regulations. The European Union, for instance, has set ambitious targets for reducing vehicle emissions, proposing legislation that would effectively ban the sale of new internal combustion engine vehicles by 2035. Such policies significantly boost the EV market and, by extension, the demand for renewable energy, as more EVs require more power to be generated from clean sources.

Moreover, the expansion of EV infrastructure, such as charging stations powered by solar or wind energy, presents further opportunities for growth in the renewable sector. This infrastructure expansion not only supports the increased use of EVs but also integrates more renewable energy into the grid, thereby promoting a circular energy economy.

Trends

Decentralization and Digitalization of Energy Systems

A major trend shaping the future of the energy transition is the decentralization and digitalization of energy systems. This movement is driven by the increasing deployment of small-scale renewable energy sources, such as rooftop solar panels and community wind farms, which contribute to a more distributed energy landscape.

Decentralization allows consumers to become prosumers—producers and consumers of electricity—thereby enhancing energy security and reducing dependence on large-scale, centralized power plants. This shift is facilitated by digital technologies that enable smart grids and advanced metering infrastructure to manage energy flow more efficiently and integrate diverse energy sources seamlessly.

Digitalization plays a crucial role in this trend by providing the tools needed to optimize energy usage and maintain grid stability when integrating intermittent renewable energy sources. Smart grids use real-time data analytics to predict energy demand and adjust supply accordingly, which not only improves the efficiency of energy distribution but also enhances the reliability of renewable energy.

For instance, according to the U.S. Department of Energy, investments in smart grid technologies have led to significant improvements in grid management, allowing for greater renewable integration. These investments are part of a broader government initiative to modernize the nation’s energy infrastructure and support the transition to a more sustainable energy system.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region held a commanding position in the Energy Transition Market, capturing 46.1% of the market share with a valuation of approximately $1.1 trillion. This dominance is largely driven by the substantial investments in renewable energy sources such as solar, wind, and hydroelectric power across major economies, including China, India, and Japan.

China, in particular, continues to be a global leader in the renewable energy sector, aggressively pursuing its goals to decrease carbon intensity and increase the share of non-fossil fuels in primary energy consumption. India follows closely, with significant government initiatives aimed at expanding its renewable capacity to meet the growing energy demands of its vast population while also adhering to its climate commitments. Japan, with its well-established technological base, focuses on innovative energy solutions like hydrogen fuel cells and energy storage technologies to achieve its carbon neutrality goals.

The region’s market strength is also bolstered by favorable government policies, including subsidies and tax incentives that encourage both local and foreign investments in green energy projects. Additionally, the increasing urbanization and industrialization in APAC necessitate robust energy solutions that are sustainable and efficient, further propelling the market’s growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

GE Vernova GE Vernova, a pivot of General Electric in renewable energy, focuses on advancing technologies in wind, solar, and grid solutions. It leverages GE’s longstanding industrial expertise to meet growing global energy demands sustainably. Vernova aims to drive innovation and efficiency, positioning itself as a leader in the energy transition market through cutting-edge developments and scalable energy solutions.

Iberdrola, S.A. Iberdrola, S.A. stands as a global powerhouse in renewable energy, particularly in wind and solar. Based in Spain, the company has expanded its footprint globally, investing heavily in sustainable energy projects to support its commitment to carbon neutrality. Iberdrola’s strategy emphasizes innovation and sustainability, making significant impacts on reducing global carbon emissions.

NextEra Energy, Inc. NextEra Energy, Inc., based in the U.S., is renowned for its extensive portfolio in wind and solar energy generation. It is one of the largest renewable energy producers in the world, with ambitious plans to expand its renewable capacity. NextEra Energy focuses on sustainable energy solutions that support both economic and environmental goals.

Constellation Constellation, an Exelon company, offers a wide range of energy services, including renewable energy and energy management solutions for residential and commercial customers. It is committed to reducing carbon footprints and promoting clean energy, reflecting its strong dedication to environmental stewardship and innovation in energy services.

Top Key Players

- GE Vernova

- Iberdrola, S.A.

- NextEra Energy, Inc.

- Constellation

- First Solar

- Ørsted A/S

- Dongfang Electric Corporation

- ABB

- Eaton

- Siemens AG

- Danfoss

- Enel X S.r.l.

- Ameresco

- Daikin Industries Ltd.

- Orion Energy Systems, Inc.

Recent Developments

GE Vernova reported robust figures for 2024. The company secured orders worth $44 billion, generating revenues of $35 billion. These financial achievements were complemented by a significant margin expansion across all segments and an impressive free cash flow of $1.7 billion.

In 2024, Iberdrola, S.A. solidified its position as a leader in the energy transition sector with strategic investments and robust financial performance. The company invested a record €17 billion, boosting its net profit significantly to €5.612 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.4 Tn |

| Forecast Revenue (2034) | USD 6.2 Tn |

| CAGR (2025-2034) | 9.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Renewable Energy, Electrification, Energy Efficiency, Others), By Technology (Energy Storage Systems, Electric Vehicles (EVs), Smart Grids, Carbon Capture and Storage (CCS), Others), By Application (Power and Utility, Transportation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | GE Vernova, Iberdrola, S.A., NextEra Energy, Inc., Constellation, First Solar, Ørsted A/S, Dongfang Electric Corporation, ABB, Eaton, Siemens AG, Danfoss, Enel X S.r.l., Ameresco, Daikin Industries Ltd., Orion Energy Systems, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}