A Conservative Group Offers a Radical Analysis of Climate Change

March 17, 2025

A recent report by the Institute and Faculty of Actuaries (IFoA) presents a radically different perspective from that provided by the International Panel on Climate Change (IPCC) on the risks associated with global heating.

Adapting the standard methodologies that actuaries use to determine the solvency of banks, pension funds, insurance companies, and other critical financial institutions, the IFoA, the regulatory body for actuaries in the UK, applied their risk management expertise to assessing climate impacts. They worked with a group of earth scientists at the University of Exeter to expand their risk analysis beyond the financial to include ecological and social risks. They included this broader systemic approach because they explicitly acknowledged that the financial focus was much too narrow and ignored the role nature and social features contribute to economic activities.

They expanded the notion of financial solvency to explore what they call “planetary solvency,” the capacity of earth’s systems to maintain the biosphere on which all life depends.

They cite two reasons for integrating ecological and social dimensions into their risk management work. These dimensions can significantly impact economic activities, but current economic models exclude such considerations. For example, severe storms caused by global heating can disrupt supply chains for extended periods. The second reason is that social or ecological risks can rise to such catastrophic levels that economic activity becomes irrelevant. At some level of heating, humans cannot survive.

The report concludes: “The risk of Planetary Insolvency looms unless we act decisively. Without immediate policy action to change course, catastrophic or extreme impacts are eminently plausible, which could threaten future prosperity.”

The Function of Actuaries

Actuaries typically analyze financial risks to ensure that an institution can remain solvent and continue operating well into the future, despite the likely risks it will encounter along the way. Their analyses consider worst-case scenarios, even ones with low probability of occurrence, especially if the worst cases are extreme or catastrophic.

Actuaries use the concept of “risk appetite” to identify the level of acceptable risk, given that risks are often uncertain but inevitable. A very low level of risk tolerance is used to ensure that these financial institutions, upon which millions of people depend, are solvent.

For example, in Europe, the amount of capital that an insurance company is required to hold is set at a level designed to withstand an extreme loss scenario that would occur only once in 200 years. This is equivalent to no more than a 0.5 percent chance of becoming insolvent in any one year.

The IFoA report makes some important comments about the respective roles of science and risk management, and how they are different but complementary. The IPCC relies heavily on science rather than formal risk management approaches.

Science is essentially concerned with accurate measurement and identifying underlying laws of nature. The conservatism inherent in the scientific process, while possibly identifying extreme but uncertain risks, emphasizes the certainties that research can provide.

By contrast, risk management, based on information provided by science and expert perspectives, determines the level of risk associated with various scenarios, and the probability of those scenarios occurring. Risk management focuses on extreme risks, not out of doom and gloom, but to understand the circumstances that could give rise to such extremes, and thus come to understand how to avoid them. Risk management accepts uncertainty and provides a transparent means of dealing with it.

In order to keep the uncertainties associated with extreme risks to a minimum, actuaries conduct frequent reviews of risk levels as new information becomes available. They don’t wait for the certainties associated with science but use updated information to adjust their levels of risk tolerance.

Risk management methodologies can deal with uncertainties in a way that science does not. They provide decision makers with valuable insights regarding necessary actions to avoid catastrophic impacts. Waiting for the certainties that science can provide could easily be too late for the required action.

The risk management approach assists decision makers to determine the urgency of specific actions, whether to slam on the brakes when a child runs into the road, or to slow down at a pedestrian crossing.

Actuaries are not merchants of pessimism, but of prudence. They base their analyses on the highest estimate of economic loss and reduce that estimate only when evidence becomes available that it is over-stated. This is a much more precautionary approach than focusing on what is perceived as most likely. Prudence increases the likelihood of avoiding extreme or catastrophic impacts, even if they are uncertain.

The Actuarial Critique of the IPCC

The IFoA actuaries shift the focus from financial solvency to planetary solvency, asking how to avoid the breakdown of earth systems that provide humanity with all the resources needed to survive and thrive.

They thus critique the IPCC process from an actuarial perspective, concluding: “Global risk management practices for policymakers are inadequate, we have accepted much higher levels of risk than is broadly understood…..Unmitigated climate change and nature-driven risks have been hugely underestimated.”

One obvious example of this inadequate risk management from the IPCC is its setting of a carbon target that has only a 50 percent chance of keeping global heating below 1.5 degrees C. This is the level where several significant negative impacts are thought to accelerate.

This means that the IPCC has accepted a level of risk associated with climate breakdown that is 100 times higher than for European insurance companies going insolvent.

Furthermore, this carbon target was established in 2018 and has not been revised since, despite the now well-established increased heating and associated risks that have exceeded the conservative IPCC projections. The science-based projections are inherently conservative, and have consistently underestimated later measurements associated with global temperature increases, sea level rise, extreme events, ocean current changes, and ice melts.

Not only does the IPCC fail to conduct annual revisions of such critical goals, it also ignores several features of the science that are now well established. Multiple tipping points have been clearly identified and more research data regarding them are available. Tipping points define thresholds beyond which negative changes may be irreversible.

Unfortunately, tipping points are not included in the IPCC scenarios because there is still too much uncertainty associated with the precise thresholds for their occurrence and their severity from a strictly scientific perspective. More research is needed.

But the potential consequences of earth systems breaking down—planetary insolvency in risk management terms—is very real. The science does not deal with the uncertainty, but risk management methodology does.

Inclusion of the tipping points in the risk management approach allows for their interactions to be considered as well as their direct impacts. As the biosphere is an integrated whole, changes in one tipping point can easily cascade to other areas, resulting in catastrophic impacts.

The risk management approach also allows for the ecological tipping points to be considered in terms of their relationship to social and economic impacts. This has rarely been undertaken in narrow financial impact studies of climate change, resulting in gross underestimations of the economic impact of global heating.

The combined impact of these various tipping points is to lower the temperature at which extreme social and economic impacts may occur. The interplay of geopolitical tensions regarding resource or migration conflicts on climate impacts is also ignored in the IPCC process. The risk management approach can integrate these dynamics into its assessment.

Because risk management has reliable techniques for dealing with the inherent uncertainties associated with these extreme scenarios, they provide invaluable information for decision makers to take appropriate actions. But decision makers are not using these sophisticated risk management tools in the IPCC. It’s both ironic and terrifying that less comprehensive and prudent methodologies are used to evaluate the stability of the earth systems that underlie our entire wellbeing than are currently applied to pensions and insurance.

Better Risk Assessment

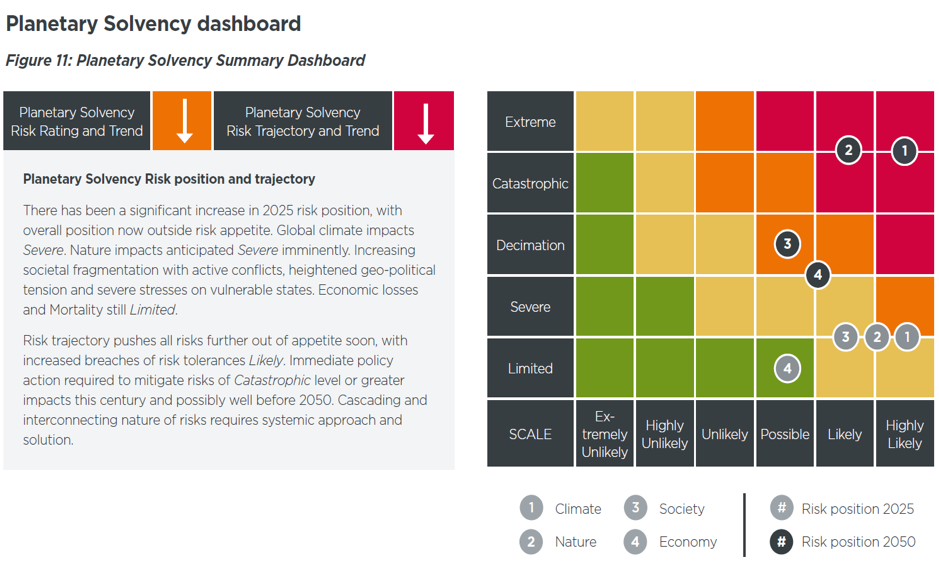

The IFoA team did an example exercise to indicate what a more appropriate risk assessment could provide. Their Planetary Solvency Dashboard indicates current risk levels for climate, nature, society and economy.

Their analysis indicates that the world is currently outside the risk tolerance (green space) for all areas other than Economy. And the situation projected for 2050 ranges from Decimation for Economy to Extreme or Catastrophic for all other areas.

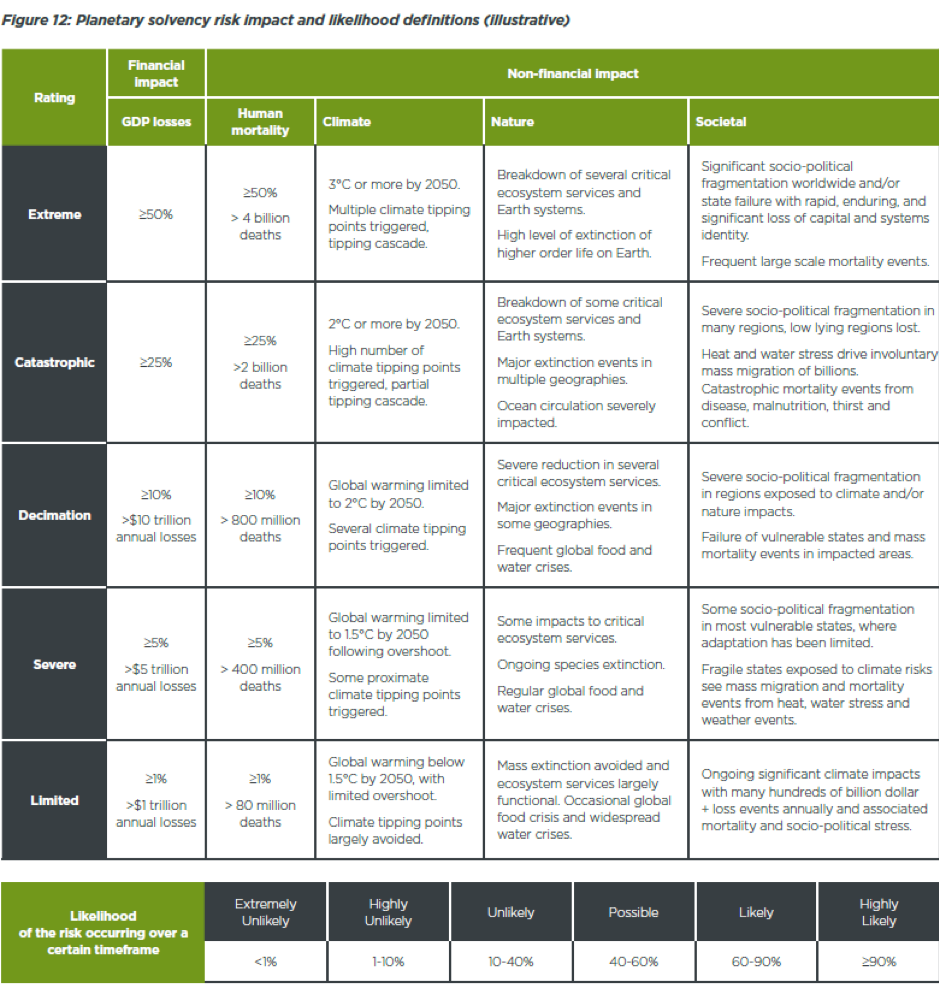

Relevant terms are defined in the next table. Note the 25% reduction in GDP associated with the Catastrophic designation.

The Planetary Solvency Dashboard describes a much more serious assessment of the financial, climate, ecological, and social risks than the ones that guide the IPCC and financial institutions. If banks, insurance companies, and pension funds paid heed to these Dashboard results, they would have to significantly reevaluate their current operations.

Given the urgency of the IFoA report, bank and pension fund investments in fossil fuels would have to shrink rapidly. Investments in any activities that are disrupting ecosystem services would also have to be significantly curtailed.

The implications of the Dashboard summary extend beyond the financial sector. Corporations reliant on fossil fuels—or whose operations cannot avoid disrupting natural systems, such as mining operations or land development of any kind—would also have to reexamine their future prospects to continue operating. They would have to justify, if possible, that their continued operation provided significant benefits to society that offset the biosphere disruption they cause. Otherwise, they would lose their social license to operate.

Adopting an actuarial approach to planetary solvency would also realign government priorities. Governments would have to provide the policy frameworks for companies operating within a safe climate space. Governments would also have to step up their efforts to support policies that alleviated the inevitable social challenges that are already evident. Migration, gross inequality, and population size all deserve considerably more effort and international cooperation to avoid the projected risks identified in the Dashboard analysis.

A wide range of international financial disclosure procedures would need to be upgraded to Planetary Solvency standards. These would include the International Financial Reporting Standards (IFRS), the Generally Accepted Accounting Principles (GAAP), the European Union Transparency Directive, the International Public Sector Accounting Standards (IPSAS), and the requirements for listing on national stock exchanges, to name just a few. All of these institutions currently use levels of risk tolerance that grossly underestimate planetary solvency.

The Way Forward

The actuarial report identifies a number of actions to bring about a more realistic appraisal of our state of planetary solvency. Such information would ensure that decision makers in national and supra-national institutions, especially the UN Security Council, have the most comprehensive and useful information available.

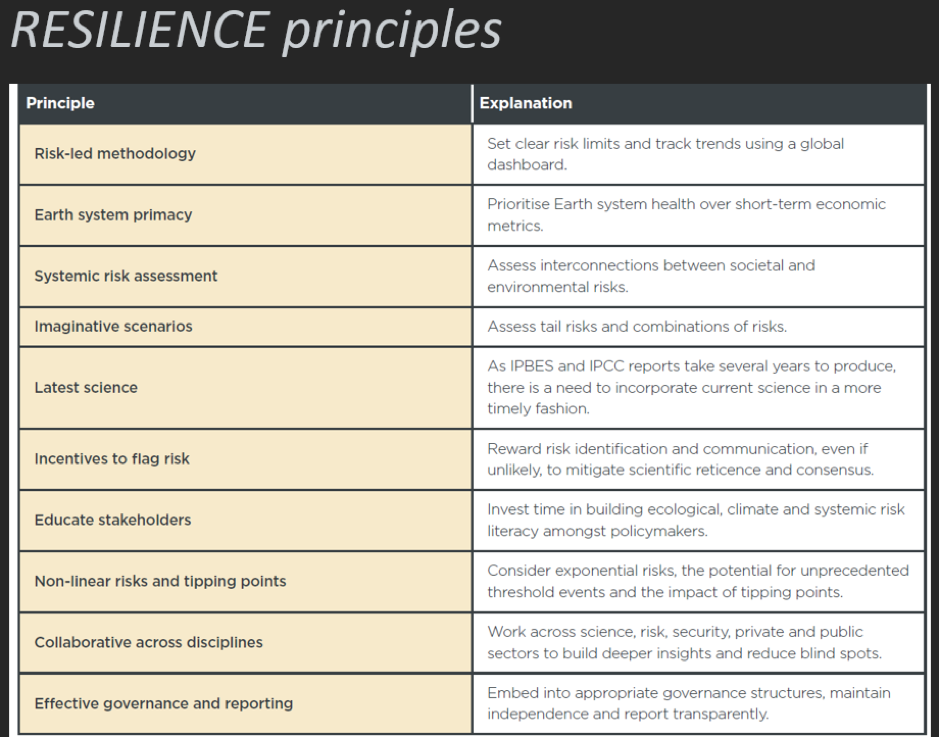

The actuaries recommend establishing an independent agency to provide annual Planetary Solvency assessment using the precautionary methodologies of risk management. They suggest updating financial solvency approaches with agreed-upon climate, ecological and social goals. And they propose a set of resilience principles that can act “as guidelines for effective civilisational risk management.”

The financially astute actuaries involved in this report state that the “current market-led approach to mitigating climate and nature risks is not delivering. There is an increasing risk of severe societal disruption (Planetary Insolvency), as our economic system drives further global warming and nature degradation.”

People everywhere trust actuaries with their pensions and investments. Perhaps it’s time to trust their expertise regarding the risks to earth systems as well.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}