After Big AI Investments: Will Amazon, Google, and Meta Run Out of Cash Flow?

February 8, 2026

As the arms race for AI infrastructure construction enters the ‘deep waters,’ an unsettling turning point for investors has emerged: In order to support the demand for AI computing power, Amazon, Google, and Meta are facing the risk of depleting or even overdrawing their free cash flow.

According to a research report released by JPMorgan on February 5, 2026, the total capital expenditure of the four major U.S. cloud giants—Amazon, Google, Meta, and Microsoft—is expected to reach $645 billion in 2026, a staggering year-on-year surge of 56%, with new spending reaching an astonishing $230 billion.

For investors, 2026 may be the year to closely monitor the balance sheets of tech giants.

For investors, 2026 may be the year to closely monitor the balance sheets of tech giants.

Google’s 97% growth rate and Amazon’s ‘cash deficit’

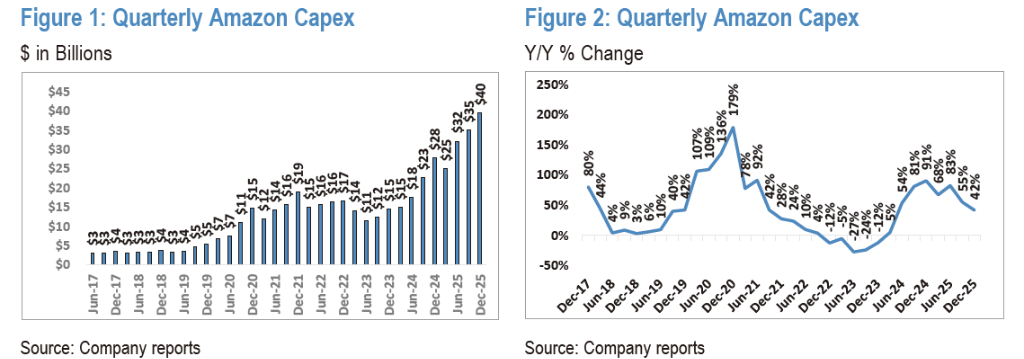

In this wave of infrastructure frenzy, Google’s investment has been extremely aggressive.

In 2026, Google’s capital expenditure guidance has been raised to between $175 billion and $185 billion, representing a year-on-year increase of up to 97%. Its funds are pouring heavily into servers and technical infrastructure.

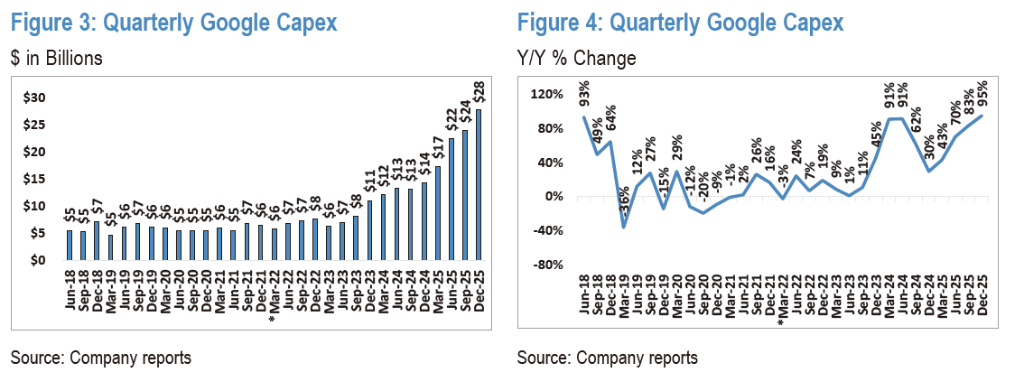

If Google is merely ‘spending wildly,’ then Amazon could be described as ‘mortgaging its future.’

In 2026, Amazon’s capital expenditure guidance is about $200 billion (a year-on-year increase of 52%). However, the crux of the issue lies in the fact that Amazon’s cash earnings can no longer cover its expenditures—according to analysts at S&P Global Market Intelligence, Amazon’s operating cash flow (OCF) in 2026 is projected to be approximately $178 billion.

This means that Amazon’s capital expenditure will exceed its operating cash flow, resulting in a substantial net cash outflow (Burn Cash). Additionally, according to The Information, Amazon is in talks to invest tens of billions of dollars in OpenAI, which will further deplete its cash reserves.

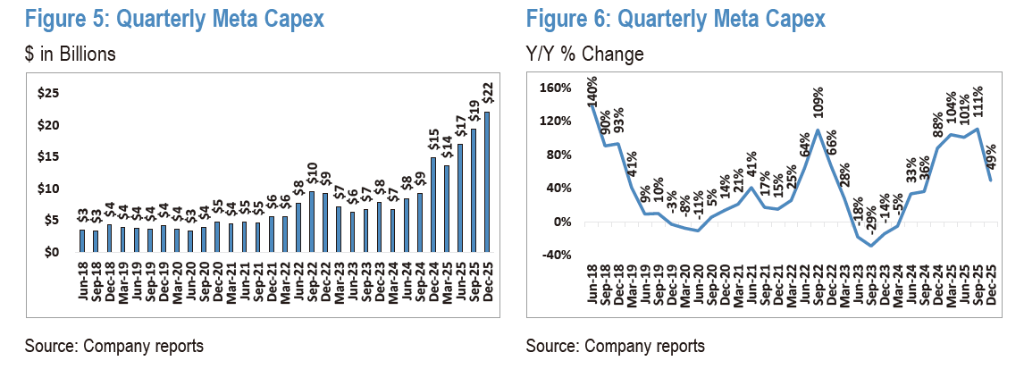

Meta’s situation is also far from optimistic. Its capital expenditure in 2026 is expected to grow by 75% to between $115 billion and $135 billion. Although it is not directly ‘overspending’ like Amazon, this massive expenditure will nearly ‘wipe out’ Meta’s free cash flow, turning its once comfortable financial position into a precarious one.

Shareholder returns under pressure, Microsoft may be the ‘exception’

As the cash flow reservoir dries up, shareholder return programs are facing adjustment pressures.

Over the past few years, tech giants have strongly supported their stock prices through large-scale share repurchases. However, in 2026, this engine is likely to stall:

Repurchase reduction: Last year, Meta spent $26 billion on share buybacks, but with free cash flow expected to shrink significantly this year, its repurchase efforts are likely to be forced down.

Dividend pressure: Google and Meta paid approximately $10 billion and $5 billion in dividends respectively last fiscal year. They should still be able to afford these dividends this year, but it will further squeeze an already tight cash flow.

Amazon will not face the same issue, as it has not conducted any share buybacks since 2022 and has never paid dividends. Given the cash deficit expected in 2026, the likelihood of it restarting buybacks is minimal.

Facing funding gaps, giants are beginning to leverage the flexibility of their balance sheets:

Google: Despite a surge in expenditures, Google remains in a ‘zero net debt’ state (cash $127 billion > debt $47 billion). S&P Global noted that even if Google were to add $200 billion in net debt, it would not trigger a downgrade of its AA+ credit rating.

Amazon: Despite facing a cash flow deficit, Amazon still held $123 billion in cash at the end of last year and issued $15 billion in bonds in November. Recently, it has filed a registration statement with the SEC, preparing for further large-scale bond issuance.

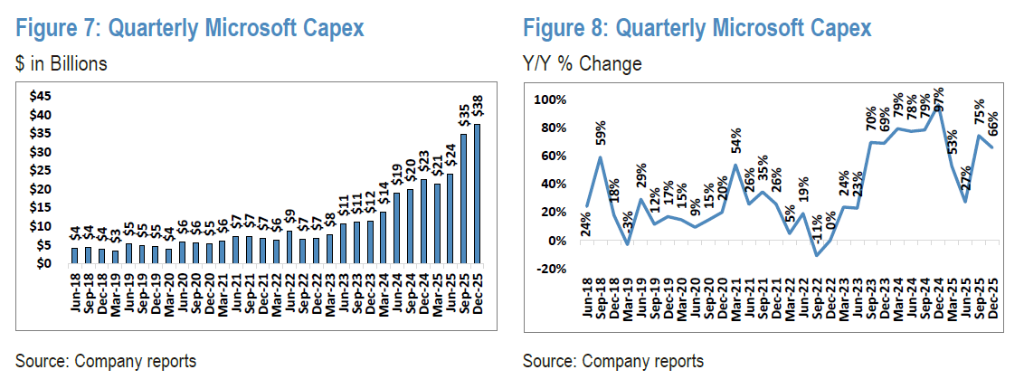

Amidst all the ‘cash burning,’ Microsoft has demonstrated unique financial resilience.

Although Microsoft’s capital expenditure for the fiscal year 2026 (ending June) is expected to exceed USD 103 billion (an increase of over 60%), analysts predict that it will still generate approximately USD 66 billion in free cash flow, sufficient to cover its massive expenditures.

However, despite the likelihood of Microsoft generating substantial free cash flow, it faces constraints that other companies do not—namely, a higher commitment to dividend payouts. Microsoft distributed USD 24 billion in dividends last fiscal year and has already raised its dividend by 10% this year.

Conclusion: Beware of the ‘Oracle Trap’.

For investors, 2026 will be a year of closely monitoring balance sheets.

Oracle provides a cautionary tale—its net debt has surged to USD 88 billion, more than twice its EBITDA, to fund data center construction. This excessive leveraging of the balance sheet has drawn market punishment, with its stock price falling 27% this year.

Now, a bill of USD 645 billion has been placed on the table.

As Silicon Valley giants attempt to use today’s cash flow or even future debt to purchase a ticket to the AI era, if this high-stakes gamble fails to translate into tangible revenue growth in the future, the potential cash flow crisis of 2026 might merely be the prelude to a valuation reset.

This article is reproduced from ‘Wall Street News’; edited by Chen Siyu from Zhitong Finance.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}