Alberta’s Dead Pipeline Walking

May 9, 2026

Asia’s push for energy sovereignty is about to gut Alberta Premier Danielle Smith’s pipeline ambitions, and PM Mark Carney’s apparent interest in enabling them.

May 8 was the 12th anniversary of the first edition of The Energy Mix, and I had mapped out a Weekender post on the changes—and the progress on climate change and the energy transition—over the last dozen years.

Then I spotted this brilliant synthesis piece by our friend Markham Hislop at Energi Media, focusing on the countries in Asia that we’ve long been told will be the buyers for expanded Canadian oil and gas production. It quickly became clear that the anniversary musings would have to wait.

Until recently, energy security meant securing a reliable supply of oil at a reasonable price. That definition is now changing. Across Asia, governments are increasingly pursuing a different goal: energy sovereignty.

Energy sovereignty means buying electric technologies like solar panels, wind turbines, batteries, EVs, nuclear reactors, and transmission infrastructure, then generating more energy domestically for decades. The upside is reliable, affordable energy without excessive dependence on foreign suppliers, volatile global markets, or vulnerable shipping routes.

Asia is leading this shift. The global oil shock triggered by the closure of the Strait of Hormuz is accelerating it. That sound you hear is the death knell for a new pipeline from Alberta to the West Coast.

Will Asian oil demand disappear overnight? Of course not. The region still consumes roughly 40 million barrels of oil per day out of a global total of around 105.5 million barrels per day.

But how much oil will Asia consume in 2050? Another important question is whether Asian governments intend to remain permanently dependent on rising imports of foreign crude oil through 2050. Increasingly, the answer appears to be no.

What If OPEC is Wrong?

The debate matters enormously for Canada.

Alberta Premier Danielle Smith, federal Natural Resources Minister Tim Hodgson, and much of the Canadian oil industry broadly align with the Organization of the Petroleum Exporting Countries’ long-term outlook. In OPEC’s World Oil Outlook 2025, global oil demand rises to roughly 124 million barrels per day by 2050. Most of that growth comes from Asia.

That forecast underpins the economic logic for a new Alberta-to-Pacific pipeline.

But if OPEC is wrong—if Asian demand peaks and begins declining in the 2030s—then Canada risks building a multi-decade export megaproject into a structurally weakening market.

And taxpayers could be exposed to serious costs for a stranded asset.

Recent statements from industry groups and Ottawa, combined with federal plans to expand support for “projects of national interest,” suggest public subsidies could eventually play a major role in financing a new pipeline. Alberta taxpayers could face an even larger burden if the provincial government participates directly.

Given what is at stake, one might expect pipeline advocates to present detailed evidence supporting their assumptions about long-term Asian demand growth.

Instead, much of the public debate simply assumes that future demand growth is inevitable.

The evidence, however, increasingly points in the opposite direction.

China’s 2025 Energy Law: Rethinking Energy Security

China’s 2025 Energy Law may be the strongest evidence against Canada’s assumption of endlessly rising Asian demand for imported oil. In 2024, China imported roughly 11 million barrels of crude oil per day, worth about US$325 billion annually. Those purchases required spending coveted U.S. dollars and exposed the Chinese economy to geopolitical risk, shipping disruptions, and volatile global commodity markets.

In the past decade alone, oil prices were disrupted in 2015 and 2016, then again in 2020 because of the Covid-19 pandemic, again in 2022 when Russia invaded Ukraine, and this year because the U.S. and Israel attacked Iran. The lesson for Asia is that oil is expensive and volatile.

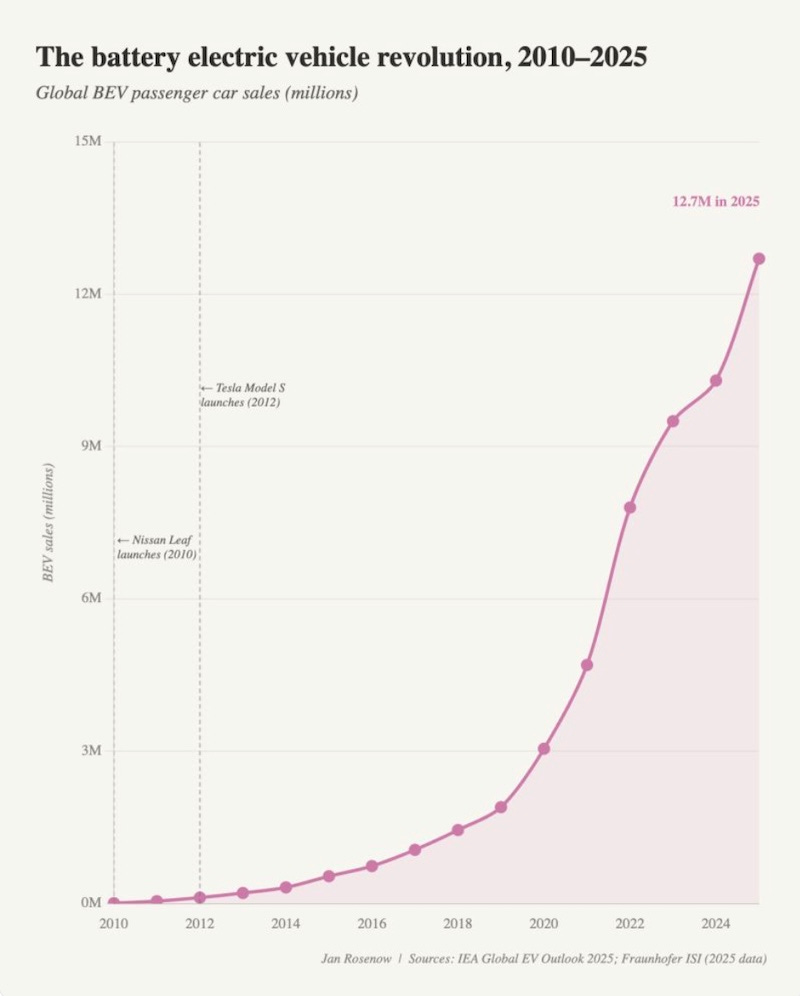

In the past, oil importers had no alternatives. Now they do. Electric vehicles and the technologies required to support them give options to countries like China and India. Increasingly, governments are embracing those alternatives.

In the case of China, the 2025 Energy Law formally integrates energy security, domestic energy supply, electrification, renewable energy, grid modernization, and industrial policy into a unified national framework. In effect, Beijing is codifying “energy sovereignty” as state policy.

The law prioritizes expansion of non-fossil energy sources, accelerated electrification, improved energy efficiency, strategic reserve capacity, and the development of resilient domestic energy systems. Renewable energy, batteries, electric vehicles, transmission infrastructure, and electricity system modernization are treated as instruments of national security and economic competitiveness.

This isn’t about emissions and climate policy. It is all about national security, economic competitiveness, and markets.

The strategic logic becomes even clearer when viewed alongside Beijing’s broader industrial strategy. China already dominates global battery manufacturing, EV production, solar manufacturing, and high-voltage transmission technology. It is rapidly electrifying transport, expanding high-speed rail, deploying nuclear power, and building renewable energy capacity at a scale unmatched anywhere in the world.

The International Energy Agency now explicitly attributes part of China’s slowing oil demand growth to EV adoption and electrified transport systems.

Taken together, the Energy Law and China’s industrial strategy suggest the country at the centre of Canada’s “Asian demand” thesis is pursuing one of the world’s most aggressive state-led oil-substitution programs.

China is not behaving like a country preparing for permanent dependence on imported crude. It is behaving like a country attempting to reduce that dependence over time.

In OPEC’s World Oil Outlook 2025, Chinese oil demand continues growing modestly through 2050, adding less than two million barrels per day. But the International Energy Agency’s World Energy Outlook 2024 Announced Pledges Scenario tells a radically different story in which demand peaks before 2030 then declines steadily due to EV adoption, high-speed rail, electrification, efficiency improvements, and structural economic changes.

China is not just another Asian market. It is the foundational assumption underpinning years of Canadian arguments about growing Asian demand for imported crude. If China’s oil demand plateaus and begins declining in the 2030s, the economic rationale for long-lived export infrastructure is shredded.

India’s Energy Strategy: Managing Oil Dependence

India is often presented as the great counterargument to concerns about long-term Asian oil demand. And at first glance, the case seems compelling. India is the world’s fastest-growing major economy, vehicle ownership remains relatively low, and oil demand is still rising rapidly. OPEC’s World Oil Outlook 2025 projects India will account for more than eight million barrels per day of incremental global oil demand growth by 2050.

But that headline number obscures a second, equally important reality: India’s government is simultaneously pursuing one of the world’s largest state-led campaigns to reduce crude import dependence.

India imports roughly 85% of the crude oil it consumes. The national government has repeatedly described oil import dependence as a strategic and macroeconomic problem. This makes the country acutely vulnerable to global price shocks, shipping disruptions, and geopolitical instability. New Delhi’s policy response now spans electrified rail, EV deployment, ethanol blending, solar expansion, compressed biogas, battery manufacturing, and energy efficiency.

The scale of India’s electrification push is already significant. The country has become one of the world’s fastest-growing solar markets and is rapidly expanding its electricity infrastructure to support industrial growth and rising consumer demand. India is also aggressively electrifying two- and three-wheel transportation, which dominates much of its urban mobility system. Electric scooters and motorcycles are especially important because they directly displace gasoline demand in one of the world’s largest transport markets.

At the same time, India is electrifying one of the world’s largest rail systems. Indian Railways has stated its intention to become a net-zero transporter and has rapidly expanded electrified track capacity in recent years. India’s ethanol blending program follows the same logic: reduce oil import costs and improve energy security.

None of this means India stops consuming oil. But India is simultaneously building the infrastructure, industrial capacity, and policy framework needed to moderate long-term import dependence. That creates a far more uncertain outlook for future crude demand growth than Canadian pipeline advocates acknowledge.

OPEC and the IEA offer widely divergent views of India’s oil future.

OPEC’s World Oil Outlook 2025 projects Indian oil demand rising by roughly 8.2 million barrels per day by 2050, implying total consumption of about 13 to 14 million barrels per day. By contrast, the IEA’s WEO 2024 Announced Pledges Scenario showed India’s oil demand rising more modestly, then plateauing or easing back toward today’s levels by mid-century.

The point here is that long-term Indian oil demand is highly scenario-dependent. The pipeline boosters’ case depends on accepting a bullish OPEC-style growth path while discounting scenarios in which electrification, efficiency, and policy commitments sharply limit long-term oil-demand growth.

Japan and South Korea: Energy Security Through Electrification

Japan’s post-Fukushima vulnerability to imported oil fundamentally reshaped its strategic thinking.

The 2011 nuclear disaster forced the shutdown of much of Japan’s nuclear fleet, triggering a massive increase in fossil fuel imports. Japan became one of the world’s largest importers of LNG, coal, and oil. That left the economy highly exposed to volatile global fuel prices, Middle East instability, and geopolitical supply disruptions.

Japan currently imports roughly 2.4 million barrels of crude oil per day, down dramatically from peak levels above five million barrels per day in the 1990s. More than 90% of those imports still come from the Middle East.

Tokyo’s energy strategy has been explicit: reduce long-term dependence on imported fossil fuels through electrification, efficiency, public transit, EVs, renewable energy, and nuclear restarts.

Japan’s 2025 Strategic Energy Plan repeatedly links lower fossil fuel dependence to national security and economic resilience following the price shocks triggered by the Ukraine war and Middle East instability. Japan is not eliminating oil consumption. But one of Asia’s largest importers is clearly pursuing a long-term strategy to reduce structural dependence on imported crude.

South Korea is moving in a remarkably similar direction. Like Japan, it is a major industrial economy with minimal domestic hydrocarbon resources and deep dependence on imported oil and LNG. South Korea currently imports roughly 2.9 million barrels of oil per day, making it one of the world’s largest crude importers despite its relatively small population.

And like Japan, Seoul’s vulnerability to global energy shocks has increasingly pushed energy security to the centre of national economic strategy. The government’s 11th Basic Plan for Electricity Supply and Demand explicitly aims to reduce dependence on imported fossil fuels through expansion of nuclear power, renewable energy, electrification, efficiency improvements, and grid modernization.

South Korea’s industrial strategy is equally important. Seoul is aggressively investing in batteries, EV manufacturing, semiconductors, and electrified industry to compete economically and to reduce long-term exposure to volatile global fuel markets.

The pattern matters because Japan and South Korea together consume more than five million barrels of imported crude oil per day. Yet both countries are openly pursuing long-term strategies designed to moderate or reduce fossil fuel dependence over time.

Neither economy is abandoning oil. But both are systematically building industrial systems intended to rely more heavily on domestically generated electricity and less heavily on imported hydrocarbons.

Other Asia

The same strategic logic increasingly extends across the rest of Asia’s major importing economies. Indonesia, Turkey, Thailand, Taiwan, Singapore, and Malaysia together consume roughly 6.5 million barrels of oil per day, a market larger than Japan.

Yet all six countries are pursuing policies aimed, to varying degrees, at reducing long-term dependence on imported hydrocarbons.

The motivations differ. Some are driven by trade deficits and fuel-import costs. Others are responding to industrial competition, geopolitical risk, or concerns about energy security. But the direction of travel is remarkably consistent: more electricity, more domestic energy production, and less vulnerability to global oil markets.

Indonesia offers one of the clearest examples. President Prabowo Subianto has explicitly stated that Indonesia intends to reduce and eventually eliminate fuel imports over time through EV deployment, domestic battery manufacturing, biofuels, and expanded electricity infrastructure.

Thailand is pursuing a similar strategy through its “30@30” EV policy, which aims for 30% of domestic vehicle production—cars, buses, two and three-wheelers—to be electric by 2030.

Taiwan increasingly treats electricity security as national security because of the island’s semiconductor industry and vulnerability to imported fuel disruptions.

Singapore’s long-term strategy combines electrification, public transit, regional power imports, and an eventual phaseout of internal combustion engine vehicles.

Malaysia’s National Energy Transition Roadmap promotes electrification, renewable energy, EV adoption, and industrial modernization alongside continued oil and gas production.

Turkey is aggressively expanding renewable energy, nuclear power, and EV manufacturing, partly to reduce pressure from imported energy costs on its balance of payments.

None of these economies are abandoning oil, and in several cases oil demand may continue rising for years. But collectively they illustrate a broader regional trend that Canadian pipeline debates ignore: many Asian governments are actively pursuing long-term strategies designed to moderate or reduce structural dependence on imported hydrocarbons.

The Emerging Asian Consensus

China, India, Japan, South Korea, and much of Southeast Asia are pursuing different versions of the same broad strategy: replace imported hydrocarbons with domestically generated electricity wherever possible.

The policies vary from country to country. China emphasizes batteries, EVs, renewables, and industrial dominance. India focuses on rail electrification, solar, ethanol blending, and low-cost transport electrification. Japan and South Korea combine nuclear power, efficiency, and industrial electrification. Southeast Asian economies are increasingly building EV manufacturing capacity and electricity infrastructure.

But the strategic logic is so very similar.

Imported oil represents economic vulnerability. Electricity increasingly represents energy sovereignty. That does not mean Asian countries will stop consuming oil, but it does mean the long-standing assumption of permanently rising dependence on imported crude oil is beginning to weaken.

And that distinction matters enormously for Canada.

The debate is not whether Asia will still use oil in 2050. The debate is whether Asian economies will require steadily growing imports of Canadian heavy crude through 2050 despite mounting evidence that many governments are actively trying to reduce hydrocarbon dependence.

That is a much harder proposition to prove.

Petrochemicals Will Not Save Long-Term Oil Demand

Petrochemicals are often presented as the ultimate backstop for long-term Asian oil demand. Even as transportation electrifies, the argument goes, Asia’s expanding middle class will continue consuming plastics, fertilizers, synthetic fibres, chemicals, packaging, and industrial materials that require hydrocarbon feedstocks.

There is truth in that claim.

Most long-term oil demand scenarios — including those from the IEA and OPEC — show petrochemicals becoming an increasingly important source of incremental oil demand as gasoline growth slows.

But there is a fundamental arithmetic problem for long-term oil bulls: petrochemicals are simply too small a share of total oil demand to offset large-scale transport electrification indefinitely.

Roughly half of global oil consumption today is tied to transportation fuels, while petrochemicals account for only about 12 to 15%. Even strong petrochemical growth cannot fully compensate for structural declines in gasoline and diesel demand once EV adoption reaches sufficient scale across China, Japan, South Korea, and eventually India and Southeast Asia.

The IEA is already documenting the early stages of this transition as EVs, electrified rail, and efficiency improvements begin suppressing oil demand growth in Asia’s largest economies. BloombergNEF estimates that at least three million barrels per day of oil demand has been destroyed by EVs.

The likely result is not an abrupt collapse in Asian oil consumption, but a plateau followed by a gradual decline beginning sometime in the early to mid-2030s as transport demand destruction increasingly overwhelms petrochemical growth.

Electric Transportation Is the Pipeline Killer

A recent Oxford Institute for Energy Studies presentation suggests that lower oil demand created by the Strait of Hormuz blockade may not be temporary. The oil shock is accelerating the structural transition already under way in Asia. The researchers warn that “the longer the disruption persists, the greater the risk of larger demand adjustment.”

That is the key point. Oil shocks no longer simply produce higher prices followed by recovery. Increasingly, they accelerate the search for alternatives. And Asia has already been searching for alternatives for years. The search is not merely for temporary replacement barrels to survive the current crisis.

Thanks largely to China, EVs are becoming cheaper, more reliable, and more widely available. Virtually every category of road transportation is now electrifying: cars, buses, scooters, motorcycles, delivery vehicles, taxis, and eventually freight transport. For consumers trying to reduce costs and governments trying to reduce oil imports, electric transportation is increasingly the obvious policy choice.

That reality fundamentally weakens the long-term economic rationale for another Alberta-to-Pacific oil pipeline.

Asia will still consume large volumes of oil for decades. But many of Asia’s largest economies are simultaneously building industrial systems designed to reduce structural dependence on imported crude. That is the central contradiction at the heart of Canada’s pipeline debate.

Pipeline advocates assume a permanently rising Asian demand for imported oil. Asian governments themselves increasingly appear to be planning for something very different.

Chart of the Week

Fossil Industry Disavows Canada-Alberta MOU as Climate Groups Defend Carbon Pricing, Methane Rules

BYD Eyes 20 Dealership Locations After Canada Greenlights Chinese EV Imports

Black Smoke, Broken Equipment Fuel Health Concerns at LNG Canada’s Kitimat Facility

Feds Want Pipeline Projects Reviewed by Energy Regulator Instead of Impact Agency

Canada’s Home Retrofit Fund Must Avoid Another ‘Boom-Bust Cycle’, Experts Warn

‘Keystone Light’: Wyoming Oil Tycoons Try to Revive Controversial Pipeline from Alberta

No End in Sight for Rising Gas Plant Costs, Analysts Warn

Scotiabank Discloses Energy Finance Ratio, with 60% Going to Fossil Fuels

Canada’s Home Retrofit Fund Must Avoid Another ‘Boom-Bust Cycle’, Experts Warn

IKEA’s Plug-In Solar Signals a Shift in Europe, Not Yet in Canada

Russia and U.S. amplifying Alberta separatist narratives to stoke division, distrust: report (Canadian Broadcasting Corporation)

Disinfluencers Never Let A Crisis Go To Waste, Hormuz Strait Edition (Climate Action Against Disinformation)

Gas prices won’t return to pre-war levels any time soon (Axios)

Ukraine Said It Hit Major Oil Refinery Deep Inside Russia (Bloomberg)

Trump admin kills Canadian-owned wind project — and demands investment in fossil fuels instead (Canada’s National Observer)

U.S. pension fund threatens to divest TotalÉnergies stake over offshore wind exit (Financial Times)

Clean power captures 91% of new U.S. grid capacity as 2025 installations hit 50 GW (PV Magazine)

Flood-related collapse of bridge isolates Pinehouse, Sask. (Canadian Broadcasting Corporation)

Tropical Rainforest Loss Slowed in 2025, but Fire is a Growing Threat to Forests Worldwide (World Resources Institute)

Roofs wanted! Inside Toronto’s push to supercharge rooftop solar (Toronto Star)

‘I thought this was impossible:’ Green grid in Australiarides through transmission failure with no fossil fuels (RenewEconomy)

Thieves Are Stealing Chile’s Solar Panels and Cashing In on the Black Market (Bloomberg)

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}