Archer Aviation Is Still Under $7. Here’s Whether Long-Term Investors Should Pounce.

April 25, 2026

Archer Aviation (ACHR 1.21%), a pioneer in the nascent electric vertical takeoff and landing (eVTOL) space, is nearing a turning point.

Once just a radically cool idea — who doesn’t want flying taxis? — Archer is moving out of the ideation phase into a company that could very well put paying passengers into the air before the end of 2026, or in the early months of 2027.

Indeed, one might argue that Archer has suddenly become the leader in the eVTOL space after its “Means of Compliance” (MOC) for its Midnight aircraft was 100% accepted by the FAA. Its rival, Joby Aviation (JOBY +0.12%), has been stuck at 97% acceptance of its MOC for about three years. That makes Archer the first U.S. company to achieve this milestone.

And yet — Archer is still only half the valuation of Joby, and at $6 per share, it’s trading only 25% higher than its 52-week low of $4.80. For long-term investors who can stomach near-term volatility, the recent sell-off might make this the best time to buy Archer. Here’s why.

Archer Aviation

Today’s Change

(-1.21%) $-0.07

Current Price

$5.70

Archer Aviation’s manufacturing edge gives it long-term strength

When most people talk about Archer’s potential, they usually talk about its certification timeline. That is, when it will get the FAA’s blessing to allow paying passengers to ride in its sleek Midnight aircraft for urban mobility.

Certainly, certification is a hurdle Archer needs to overcome. Without it, there’s no hope this company will survive. But the question of certification has become less of an “if” and more of a “when,” especially with support from the White House to accelerate eVTOL deployment.

At this point in 2026, investors should be asking which company will scale production after it has FAA certification. And on that front, Archer’s approach may give it an initial edge.

You see, unlike Joby, which wants to manufacture nearly all of its eVTOL parts in-house, Archer has partnered with specialized suppliers to handle major parts of the production process. For example, it’s buying lithium-ion batteries from Molicel, whose high power density is exactly what an eVTOL needs for range and rapid charging.

Image source: Stellantis.

Archer also has a major partnership with Stellantis (STLA 2.77%), whose manufacturing expertise will help it produce eVTOLs at a mass scale, as well as with Honeywell (HON 0.56%) for control actuation and thermal management systems.

True, Joby’s in-house approach could give it more control over its aircraft’s performance and quality. The downside, however, is that Joby will likely spend more on R&D in the near term, while rival Archer is using capital to produce more aircraft and build an eVTOL infrastructure. In the tight race between these two pioneers, that leverage of expertise might give Archer the edge to take the lead.

Should investors buy Archer today?

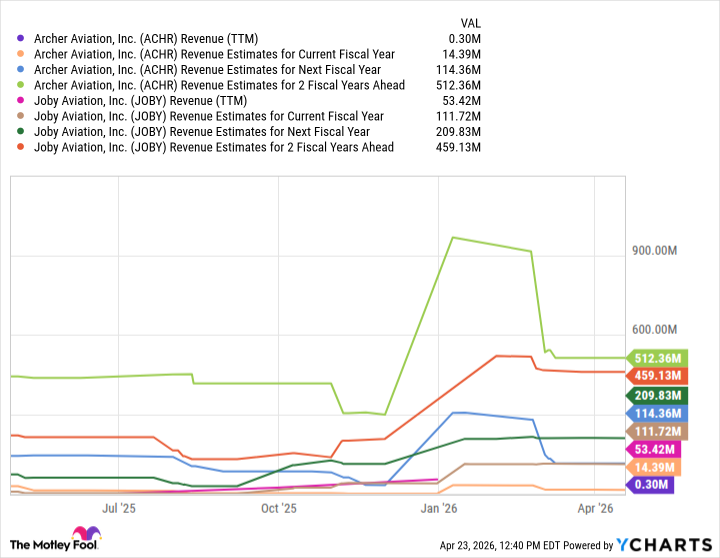

Archer’s market valuation (roughly $4.3 billion) is about half of Joby’s (about $8.5 billion), yet Archer’s strategic partnerships and manufacturing capacity could have it generating more revenue than Joby within two years, as the chart below demonstrates.

Data by YCharts

The eVTOL space, which could be worth trillions, is likely big enough to include both Archer and Joby. But over the next five years, Archer is likely going to close the gap and take the lead. That could make the return from today’s price immense in comparison to an investment in Joby.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}