Assessing Tesla (TSLA) Valuation As Investor Narratives Clash On Future Growth Potential

June 1, 2026

Advertisement

Tesla stock performance snapshot

Tesla (TSLA) continues to draw investor attention, with the stock up about 6% over the past month and roughly 6% over the past 3 months, despite a year to date decline of around 5%.

See our latest analysis for Tesla.

That recent 6.4% 30 day share price return and 6% 90 day share price return contrasts with a year to date decline of about 5%. At the same time, the 1 year total shareholder return of 21.4% and 3 year total shareholder return of 91.1% highlight how sentiment has shifted over different time horizons.

If Tesla has you thinking about where growth or volatility could show up next, it may be worth scanning for other AI focused opportunities using 60 profitable AI stocks that aren’t just burning cash

With Tesla trading near its quoted analyst price target and its intrinsic value estimate suggesting a small premium, the key question is simple: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 29.3% Undervalued

According to the most followed narrative on Tesla, a fair value of about $588 per share sits well above the last close at $415.88. This frames the stock as materially undervalued against that long term view.

Tesla’s first paid robotaxi service is set to launch in Austin, Texas, in July 2025. Unlike Waymo’s hardware-intensive, geofenced model, Tesla’s approach relies on scalable software and an expanding fleet of self-driving customer vehicles.

Curious what justifies that higher fair value? The narrative leans heavily on aggressive shifts into autonomy, energy storage, and humanoid robotics, with margins and growth assumptions that resemble a software and AI platform rather than a traditional automaker.

Result: Fair Value of $588.18 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this bullish “physical AI” pitch still hinges on smooth robotaxi rollout and ambitious Optimus scaling, where regulatory setbacks or execution missteps could quickly challenge the story.

Find out about the key risks to this Tesla narrative.

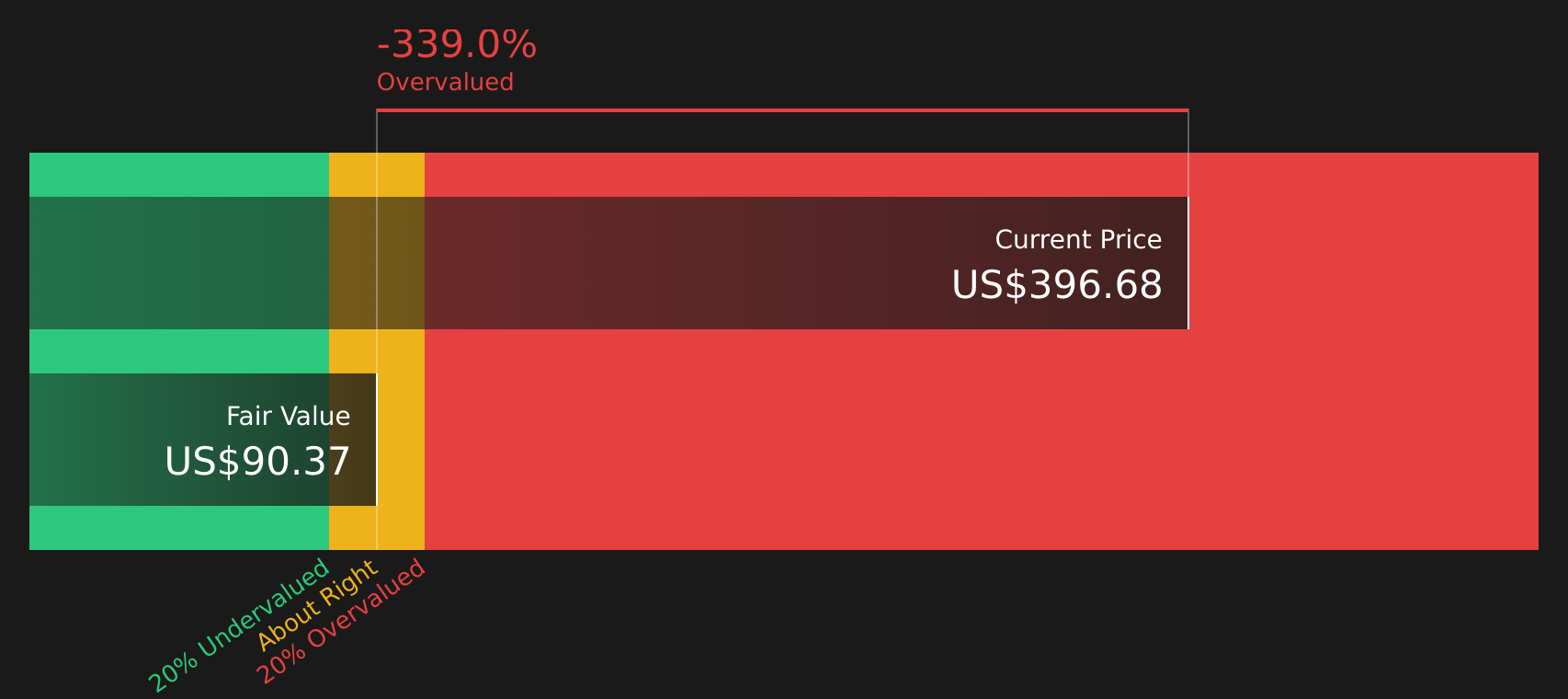

Another view on Tesla’s valuation

The most followed user narrative points to a fair value of about $588 per share and calls Tesla undervalued. Our DCF model tells a very different story, with an estimated future cash flow value of $90.72 per share, which frames the current $415.88 price as expensive. Which lens do you trust more for such a complex story?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With both bullish and cautious views in play, now is the time to look through the numbers yourself and decide where you stand, starting with 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If Tesla has sharpened your interest in the market, do not stop here. Broaden your watchlist with focused stock ideas that fit your style.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}