Beyond the Middle Market: Private Equity Investing for a More Demanding Regime

May 5, 2026

For much of the past decade, the middle market, generally defined as companies with enterprise values roughly between $250 million and $2 billion, has held a favored position in private equity portfolios. The logic was straightforward: entry valuations were often lower, buyers were more fragmented, leverage could amplify returns and operational improvements appeared easier to identify and implement. In a world of cheap capital and relatively quick exits, that combination worked well.

That playbook is less reliable today.

Private equity has entered a more demanding phase. Cheap financing, multiple expansion and relatively fast exits are no longer a dependable engine of returns. Bain & Co. put it plainly in its 2026 global private equity report: “As the new cycle gains steam, the maturing industry has hit an inflection point. The basis of competition has shifted dramatically.” These are not cosmetic changes. They alter where edge is most likely to persist and how portfolios are likely to be built.

The core thesis of this article is simple: in a higher-cost-ofcapital, slower-exit and higher-dispersion environment, the historic middle-market advantage is less dependable. In this regime, differentiated capabilities, particularly around scale, navigating complexity, structuring and repeatable operating execution, matter more. Portfolio construction should reflect that reality.

That final point is critical. This is not just a debate about market segments. It is a portfolio-construction problem. Diversifying across many managers in the same segment does not create differentiation. In many cases, it does the opposite — which raises the question: how should private equity portfolios be constructed in a more dispersed environment?

Why the Traditional Middle-Market Edge Is Less Structural Today

The middle market still matters. It remains a large, diverse and important part of the private equity ecosystem. In 2025, middle-market deal value reached $410.7 billion in the US — the highest since 2021 — across an estimated 4,018 transactions,[1] underscoring that the segment remains active and meaningful. Even so, the key question is no longer whether the middle market is thriving. It is whether the advantages once associated with it remain intact, and whether they are still durable enough to anchor a portfolio thesis. Several developments suggest they are not.

First, there is rising competition. The middle-market opportunity set is no longer a lightly covered corner of private markets — a growing number of sponsors, lenders and intermediaries are now competing for a finite pool of high-quality assets. Information and access have become more institutionalized, with intermediated processes increasingly common and global buyout dry powder now exceeding $1 trillion.[2]

One of the historical foundations of the middle-market case was cheaper entry. In an earlier era, lower prices and less competition often meant lower leverage multiples, more conservative structures and more room for operational upside. Some of those characteristics still exist, but they are less structural and less dependable today. The real question is not whether middle-market assets can still be bought at lower absolute multiples than large-cap assets; they often can. In a market that is more intermediated, more transparent and more crowded, it is much harder to assume that pricing advantage still reliably translates into stronger risk-adjusted outcomes.

Leverage and multiple expansion are also less helpful than they once were — together they accounted for roughly 59% of returns between 2010 and 2022.[3] That had more to do with the environment than with manager skill. With borrowing costs now higher, lenders more focused on cash-flow durability and refinancing risk more visible, the margin for error is thinner. Bain’s observation that “12 is the new 5” captures the new math of how much more EBITDA growth is now required when leverage is no longer doing the same work it once did.

Not all parts of the market are equally exposed to these dynamics. Middle-market transactions increasingly rely on private credit for financing, whereas larger transactions retain broader access to syndicated and public markets. As capital conditions tighten and financing becomes more selective and expensive, that divergence narrows the set of viable transactions, constrains leverage and increases the importance of underwriting discipline and operational execution.

Slower exits compound these pressures. Distributions as a percentage of NAV have remained below 15% for a record four consecutive years.[4] McKinsey found that fiveyear rolling distributions as a share of AUM hit their lowest recorded level in 2025. Hamilton Lane’s data also show longer paths to liquidate NAV and a rising share of exited buyouts held more than seven years. As liquidity narrows, buyer universes matter more. Larger, better-prepared businesses often have access to more monetization routes — strategic sales, broader sponsor universes, IPOs, minority stake sales or partial realizations — while smaller assets can become more dependent on a thinner financialbuyer channel. Managers can no longer assume that a cooperative exit market will offset mediocre underwriting.

The conclusion is not that the middle market no longer works. It is that segment exposure alone is no longer a durable advantage. The harder question is whether that advantage remains sustainable at the portfolio level in a more mature, competitive and less forgiving environment.

A Higher Bar in a Higher-Dispersion World

These structural changes create a higher bar for private equity managers. They also raise an uncomfortable but necessary portfolio-construction question: what happens when investors diversify broadly within a segment whose returns are becoming more dispersed?

Return dispersion is now central. What appears to be a recovery in overall deal activity and exit volumes masks a widening gap between the best-positioned firms and everyone else. Outcomes are increasingly shaped less by exposure to the asset class and more by deliberate choices about how firms source deals, create value from operational improvements, build leadership and operate through longer and more complex holding periods.[5] In that environment, manager selection becomes the primary driver of results.

In private markets, institutional investors often behave as if they are searching for the “lottery ticket,” the small investment that will deliver outsized returns. But in a highreturn-dispersion, low-persistence environment, that is a tremendously difficult strategy to execute consistently. More broadly, the reward for success in investing increasingly reflects scale. In public markets, investors have done the opposite, concentrating capital in larger, more established companies.

A portfolio of 20 to 40 middle-market managers concentrated in the same segment is likely to produce a median outcome. In other words, broad diversification within a single segment does not just reduce risk — it can systematically produce average results. That is not a risk — it is arithmetic. Diversification reduces idiosyncratic risk, but it also compresses differentiation. Too much diversification in a high-dispersion segment creates a paradox: the portfolio looks prudent, but its very construction pushes the result toward average.

Broad middle-market exposure, absent real differentiation, increasingly looks like beta rather than alpha. The relevant questions are therefore not simply whether large-cap or middle-market private equity is “better.” They are: where does persistent edge exist; which types of managers are structurally better equipped for this environment; and how should those capabilities be combined in a portfolio to maximize the probability of above-median outcomes and a more asymmetrical return setup?

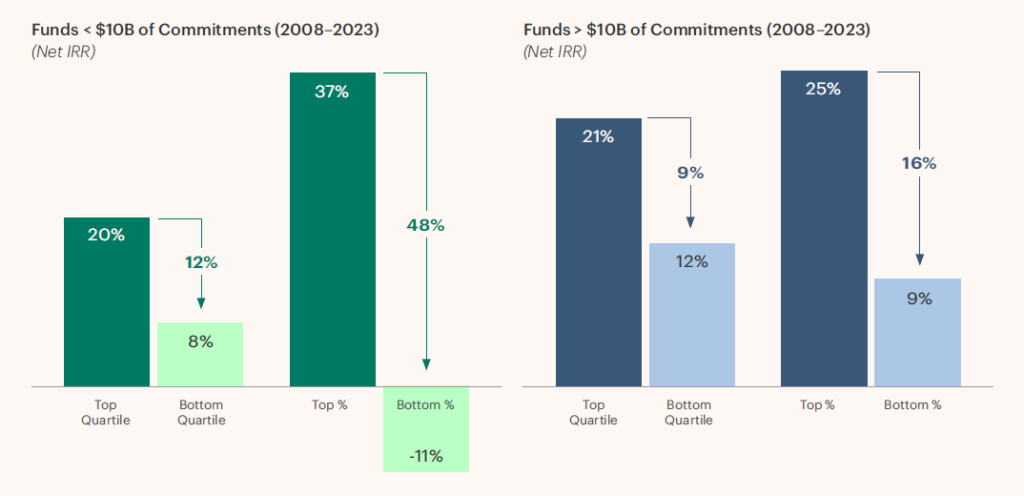

Smaller Funds, Larger Spreads: Manager Selection Matters

Source: Cambridge Associates Benchmark Calculator (via Refinitiv) as of December 2025. Reflects aggregated data for large-cap focused “Buyout Funds” as defined by Cambridge Associates for vintages over last 15 years (2008, 2013, 2018, 2023). “Smaller funds” refers to buyout funds with commitments of less than $10 billion of commitments, as reflected in Cambridge Associates benchmarking data.

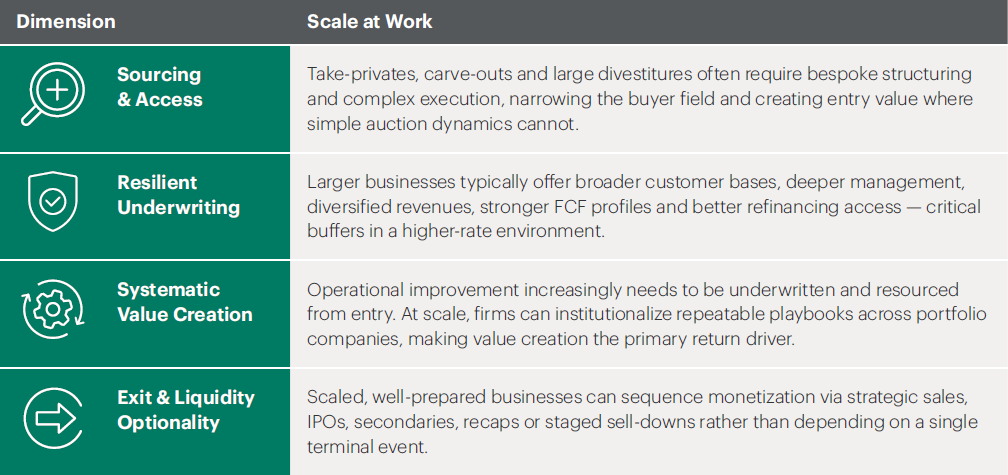

Where Persistent Edge Exists Today — Scale Expands the Toolkit

The clearest answer is that scale expands the toolkit.

This is not an argument that bigger is always better, nor that size alone creates alpha. It is an argument that, in the current regime, scale can create advantages that are harder to replicate. As McKinsey puts it, “the sheer size of the vehicle matters.” Scaled managers are advantaged not because they are bigger, but because they have more ways to create value — and more ways to avoid losing.

First, scale reduces competition in complex transactions. Take-privates, carve-outs, large corporate divestitures and capital-intensive situations tend to involve fewer credible buyers, more bespoke structuring and more execution complexity. The rebound in take-private activity reflects a growing willingness to pursue these transactions, particularly where discounted public assets or separation situations offer more room for differentiated underwriting. Complexity creates entry value in places where simple auction dynamics do not.

Second, scale improves resilience — through diversification, cash flow and access to capital. Larger businesses often have broader customer bases, deeper management benches, more diversified revenue streams, better refinancing access and more options around capital structure. The point is not that large automatically means safe. It is that underwriting discipline, balance-sheet flexibility and downside protection matter more than simple reliance on smaller company size.

Third, at scale, operational improvement becomes repeatable, not situational. Value creation can no longer be treated as an afterthought. It must be underwritten, resourced and executed from entry. Operational improvement is no longer a secondary lever — it is increasingly the primary driver of returns.

will enjoy perfect optionality. It is that optionality itself has become more valuable, and scaled platforms are often better positioned to create it.

How Scale Changes the Dynamic

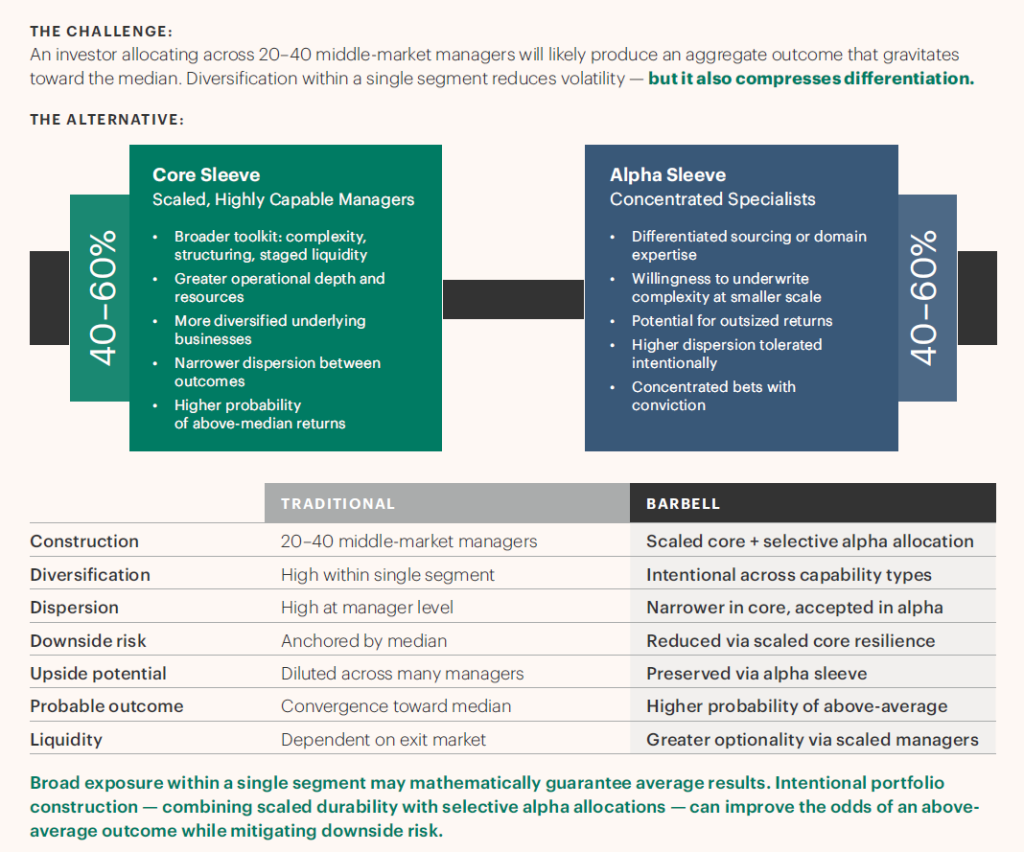

Portfolio Implications: Why a Barbell Approach Can Improve the Odds

Once the market is viewed through this lens, differences in portfolio construction come into focus.

A broad, homogeneous portfolio of middle-market managers will likely produce median results. The answer is not to abandon the middle market. It is to construct more deliberately, capturing the segment’s strengths while managing its limitations.

That is where a barbell framework becomes useful. This is not a distinction between alpha and non-alpha. It is a distinction between different forms of alpha — repeatable, scaled alpha on one side and more concentrated, idiosyncratic alpha on the other. One side of the barbell is a core sleeve of scaled, highly capable managers — designed to generate repeatable, structural alpha with lower dispersion — firms with broader toolkits, deeper operating infrastructure, better access to complex opportunities, more financing flexibility and more resilient exit pathways.

Improving the Odds: A Barbell Approach to Portfolio Construction

These managers may not always generate the most dramatic outliers, but they can increase the probability of above-median outcomes while reducing aggregate downside risk.

On the other side sits a more concentrated sleeve of specialist managers — where alpha is higher variance but potentially higher magnitude — managers with differentiated sourcing, expertise, repeatable specialization or a clear ability to underwrite complexity at smaller scale. McKinsey puts the condition crisply: “Not everyone can be big. But those that are not big had better be specialized.” That is the right positioning for smaller managers in the current environment. The case is no longer broad middlemarket beta, it is selective specialist alpha.

That combination is structurally stronger than a portfolio of undifferentiated funds. The scaled core can provide durability, stronger downside protection and broader liquidity routes. The specialist sleeve preserves upside and concentrated alpha potential where genuine differentiation exists. The barbell combines two forms of alpha — one more repeatable, one more variable — to improve the asymmetry of the overall portfolio: more downside resilience on one side, more targeted upside on the other.

This is also why overdiversification within a single segment is often counterproductive. In public markets, investors do not build resilient portfolios by owning only one capitalization tier, one factor or one style. Private equity should be no different. Company size, strategy and manager capability all matter. A portfolio that combines scaled durability with selectively chosen specialist alpha is more likely to behave like a portfolio designed for today’s regime rather than yesterday’s.

Conclusion

Private equity remains a compelling asset class. But the conditions that once made the middle market feel structurally advantaged are less reliable than they used to be.

Competition is broader. Cheap leverage is gone. Exit timelines have lengthened. Dispersion has widened. Bain’s framing of the new deal math, McKinsey’s view that “the sheer size of the vehicle matters,” and the broader market observation that successful investors increasingly gravitate toward scale all point in the same direction. The premium has shifted toward capabilities that are harder to replicate: disciplined underwriting, repeatable operational execution, the ability to navigate complex situations and flexibility around capital structure and exits.

That shift changes how private equity portfolios need to be built. Broad exposure within a single segment may feel diversified, but in a high-dispersion market it increases the probability of average results. A more intentional approach — pairing a scaled core of resilient managers with a smaller set of true middle-market specialists — better reflects where edge is most likely to persist.

Segment labels matter less than capability and portfolio construction.

The debate, then, is no longer simply where private equity used to work best. It is where the odds are best today — and how portfolios need to be built to capture them.

Important Disclosure Information

All information contained in this material is as of May 2026 unless otherwise

indicated.

This material is for informational purposes only and should not be treated as research.

This material should not be copied, distributed, published, or reproduced, in whole

or in part, or disclosed by any recipient to any other person without the express

written consent of Apollo Global Management, Inc. (together with its subsidiaries,

“Apollo”).

The views and opinions expressed in this material are the views and opinions of

Apollo Analysts. They may not reflect the views and opinions of Apollo and are

subject to change at any time without notice. Further, Apollo and its affiliates

may have positions (long or short) or engage in securities transactions that are not

consistent with the information and views expressed in this material. There can be

no assurance that an investment strategy will be successful. This material does not

constitute an offer of any service or product of Apollo. It is not an invitation by or on

behalf of Apollo to any person to buy or sell any security or to adopt any investment

strategy, and shall not form the basis of, nor may it accompany nor form part of,

any right or contract to buy or sell any security or to adopt any investment strategy.

Nothing in this material should be taken as investment advice or a recommendation

to enter into any transaction.

Hyperlinks to third-party websites in this material are provided for reader

convenience only. There can be no assurances that any of the trends described in

this material will continue or will not reverse. Past events and trends do not imply,

predict or guarantee, and are not necessarily indicative of future events or results.

Unless otherwise noted, information included in this material is presented as of

the dates indicated. This material is not complete and the information contained

in this material may change at any time without notice. Apollo does not have any

responsibility to update the material to account for such changes. Apollo has not

made any representation or warranty, expressed or implied, with respect to fairness,

correctness, accuracy, reasonableness, or completeness of any of the information

contained in this material (including but not limited to information obtained

from third parties unrelated to Apollo), and expressly disclaims any responsibility

or liability thereof. The information contained in this material is not intended

to provide, and should not be relied upon for, accounting, legal or tax advice or

investment recommendations. Investors should make an independent investigation

of the information contained in this material, including consulting their tax, legal,

accounting or other advisors about such information. Apollo does not act for you and

is not responsible for providing you with the protections afforded to its clients.

Certain information contained in this material may be “forward-looking” in nature.

Due to various risks and uncertainties, actual events or results may differ materially

from those reflected or contemplated in such forward-looking information. As

such, undue reliance should not be placed on such information. Forward-looking

statements may be identified by the use of terminology including, but not limited

to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”,

“intend”, “continue” or “believe” or the negatives thereof or other variations thereon

or comparable terminology.

The Standard & Poor’s 500 Index (S&P 500) is a market-capitalization weighted

index of the 500 largest US publicly traded companies and one of the most common

benchmarks for the broader US equity markets. Index performance and yield data are

shown for illustrative purposes only and have limitations when used for comparison

or for other purposes due to, among other matters, volatility, credit or other factors

(such as number of investments, recycling or reinvestment of distributions, and types

of assets). It may not be possible to directly invest in one or more of these indices

and the holdings of any strategy may differ markedly from the holdings of any such

index in terms of levels of diversification, types of securities or assets represented and

other significant factors. Indices are unmanaged, do not charge any fees or expenses,

assume reinvestment of income and do not employ special investment techniques

such as leveraging or short selling. No such index is indicative of the future results of

any strategy or fund.

Investing involves risk including loss of principal. Alternative investments often are

speculative, typically have higher fees than traditional investments often include a

high degree of risk and are appropriate only for eligible long-term investors who are

willing to forgo liquidity and put capital at risk for an indefinite period of time. They

may be highly illiquid and can engage in leverage and other speculative practices that

may increase volatility and risk of loss.

References to downside protection are not guarantees against loss of investment

capital or value.

This material may reference trade names, trademarks, or service marks of companies

that are not owned by Apollo or Apollo funds, or that may be held as investments

by Apollo or one or more Apollo funds. The use or display of these companies’ trade

names, trademarks, or service marks is not intended to imply any relationship with,

or endorsement or sponsorship of Apollo, by such companies. All company names

and logos are trademarks of their respective holders.

Past performance is not necessarily indicative of future results.

Additional information may be available upon request.

[1] PitchBook 2025 Annual US PE Middle Market Report

[2] Bain & Company, Global Private Equity Report 2026

[3] McKinsey & Company, Global Private Markets Report 2026

[4] Bain & Company, Global Private Equity Report 2026

[5] McKinsey & Company, Global Private Markets Report 2026

`;

});

$(‘.wdm-author-info’).html(html);

});

jQuery(document).ready(function($){

var podcastItem = $(“.wp-block-latest-posts__list li:nth-child(3)”);

var readMoreLink = $(“.wp-block-latest-posts__list li:nth-child(3) .excerpt-cta”);

$(podcastItem).children().attr(“target”, “_blank”).attr(“href”, “https://www.apolloacademy.com/the-view-from-apollo/?title=Private Equity: Alpha”);

$(readMoreLink).children().attr(“target”, “_blank”).text(“Listen Now”).attr(“href”, “https://www.apolloacademy.com/the-view-from-apollo/?title=Private Equity: Alpha”);

var podcastItem2 = $(“.wp-block-latest-posts__list li:nth-child(1)”);

var readMoreLink2 = $(“.wp-block-latest-posts__list li:nth-child(1) .excerpt-cta”);

$(podcastItem2).children().attr(“target”, “_blank”).attr(“href”, “https://www.apolloacademy.com/the-view-from-apollo/?title=Private%20Equity%20Portfolios”);

$(readMoreLink2).children().attr(“target”, “_blank”).text(“Listen Now”).attr(“href”, “https://www.apolloacademy.com/the-view-from-apollo/?title=Private%20Equity%20Portfolios”);

});

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}