Billionaire Stephen Mandel’s Largest Holding Is Down 15% From Its All-Time Highs. Is It a

January 5, 2026

Meta Platforms had a rough Q4, but that could change in the new year.

Investors have access to all sorts of data, including the holdings that billionaire hedge fund managers have.

At the end of each quarter, any money manager with greater than $100 million in assets must disclose their holdings to the Securities and Exchange Commission (SEC) in a Form 13F, and that list is then made available to the public 45 days later. So, any information we have about these funds is as of Sept. 30, but it can still provide valuable insights, especially if something notable happened between now and then.

One billionaire I follow is Stephen Mandel, the manager of Lone Pine Capital Holdings. He has a significant stake in a notable big tech company, Meta Platforms (META +1.82%). As of Sept. 30, 7.1% of his total portfolio was in Meta’s stock — the largest position he holds. That’s significant because Meta has performed poorly since Sept. 30 and is down around 10%. While this may concern some investors, Mandel could be scooping up shares due to the market’s short-term pessimism.

A buy from Mandel could signal investors that Meta is a smart buy now, but we won’t know about it until around March 15. Should you scoop up shares of Mandel’s largest holding before we know for sure that he did? Let’s see if the reward is greater than the risk.

Image source: Getty Images.

The market didn’t like Meta’s guidance for 2026

Meta Platforms is the parent company of social media platforms including Facebook, Instagram, Threads, and WhatsApp. Nearly all of its revenue comes from advertising on these platforms, which can be a boom-and-bust industry. Right now, the ad industry is strong because the economic outlook is solid. If the economic outlook weakens, advertising spending is the first place companies pull back on, which harms Meta’s business.

Advertisement

Meta Platforms

Today’s Change

(1.82%) $11.83

Current Price

$662.24

Meta’s CEO and founder, Mark Zuckerberg, is always looking for the next big thing and isn’t afraid to spend serious capital to find it. A few years ago, he thought it was the metaverse, which prompted the company’s name change from Facebook. Now, he seems to be fixated on generative artificial intelligence (AI) and the various form factors to bring it from the computer screen to everyday interactions.

The most prevalent place where Meta is developing this is in its glasses, as it thinks it can bring a product to market that provides generative AI capabilities for real-world situations. Meta is currently spending a lot to develop these glasses, although that could be shifting.

Meta is rumored to be cutting the budget of its Reality Labs division by 30% in 2026, which is a welcome shift for investors, as this division has spent a lot of money and made nearly nothing. However, it’s unlikely that Meta will sit on that cash.

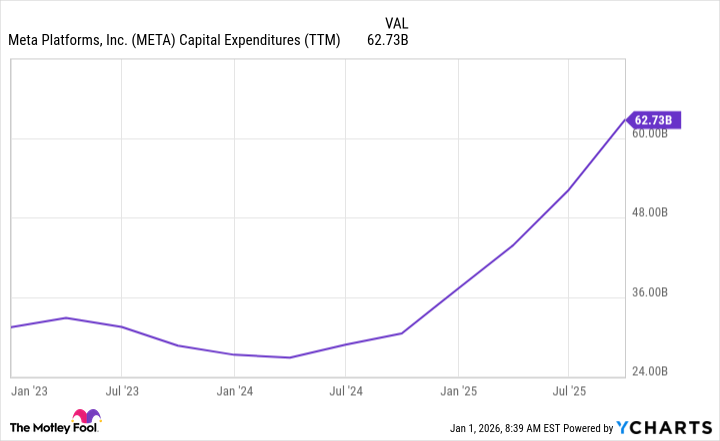

Instead, it will likely spend it on increasing its artificial intelligence computing capacity. Meta is taking a dual approach of building out its own data centers and renting computing capacity from others. This isn’t cheap, and Meta’s capital expenditures have exploded as a result.

META Capital Expenditures (TTM) data by YCharts

But that’s just the beginning. Meta stated in its third-quarter earnings release that its “capital expenditures dollar growth will be notably larger in 2026 than 2025.” That likely means Meta’s capital expenditures will rise above $100 billion for the year, which the market didn’t like, so it sold off the stock.

However, if Meta can develop a sustainable AI advantage, this investment could pay off, which is why Mandel may have been buying shares in the aftermath of the sell-off.

Meta’s stock is cheaply priced

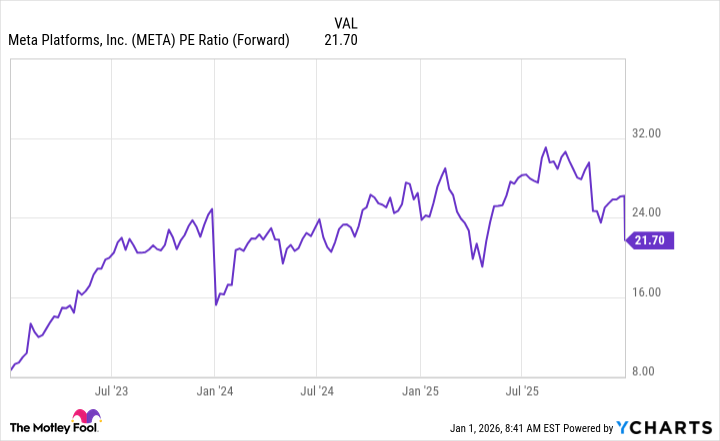

Following the sell-off, Meta’s stock now trades at a bargain price.

META PE Ratio (Forward) data by YCharts

At 21.7 times forward earnings, Meta is now cheaper than the S&P 500, which trades for 22.3 times forward earnings. This is a significant discount from where it once traded, and it looks like a compelling buying opportunity, especially because Meta’s base business crushed it during the third quarter.

In Q3, Meta’s revenue rose an outstanding 26% year over year. That shows huge business strength, and that momentum could drive the stock higher in 2026, even with higher capital expenditures.

I think Meta is an excellent stock to buy right now, and I won’t be surprised to see multiple billionaires add to their positions once Q4 filings come out. But in the meantime, Meta looks like a great buy, and investors should take advantage of the sale price before it recovers in 2026.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}