You’re reading this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news. We no longer send these by email as we did in the past, but we post this and all of the newsletters on our website here.

Friends,

Cannabis stocks have retreated substantially since earlier this month and are now down in October. The New Cannabis Ventures Global Cannabis Stock Index, which closed at a value of 7.03, is down 8.5% in October. The year-to-date gain is only 2.2%. After declining four over four consecutive years, the market is close to extending the streak of declines.

MSOS closed at 4.44, which was a 1.5% discount to its NAV, and it has dropped 7.3% in October but is up 16.5% year-to-date. Last week, it was at 5.40, up 41.7% year-to-date and 12.7% in October when I warned about the upcoming financial reports. I discussed the month-to-date returns of the 9 MSOs in the American Cannabis Operators Index, and they ranged from +4.4% to +35.8% then. Now, they are lower, with six of them showing losses.

Looking at the largest 7 positions in MSOS, all in excess of 5%, with two, Curaleaf and Trulieve, above 21%, the best performer is Verano, up 7.7% in October. The three largest positions are all down, with Curaleaf down 3.9%, Trulieve down 8.8% and Green Thumb Industries down 9.9%.

Year-to-date, the three largest positions are very divergent, with one down double-digit and two up substantially:

Looking at the other four large holdings, which range in size from 5.6% to 7.7%, they are all double-digit gainers:

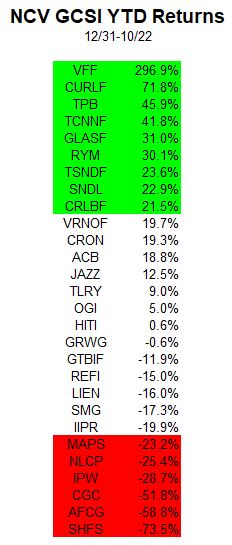

- Glass House Brands: +31.0%

- TerrAscend: + 23.6%

- Cresco Labs: +21.5%

- Verano Holdings: +19.7%

These 7 largest positions in MSOS are all in the Global Cannabis Stock Index, though with much lower holding percentages for a few and lower for all. While they have rallied for the most part in 2025, all of them have declined since the elections last November. As I discussed in last week’s newsletter, the current financials are not exciting at all. What is driving them? Potential rescheduling, which, if it happens, could wipe out 280E taxation.

There is more to the cannabis sector than just the MSOs, some of which have soared since the end of June. The index currently has members from five other sub-sectors, but just one is from Biotech, just one is from THC Beverage and just one is from Canadian Retailers. MSOs make up 26.1% of the index, which is below Ancillaries at 39.1% and above Canadian LPs at 23.8%. I actually like the Ancillaries and still recommend that investors look at the cannabis REITs, which I last discussed here on 8/14.

Earlier this year, I was a big fan of the Canadian LPs, but my exposure in my model portfolio at 420 Investor is in just two names and is slightly lower than the index exposure. Canopy Growth, which I have disliked for a while, is one of the Canadian LPs in the index that I am avoiding. It is down 51.8% in 2025, but it has increased 28.2% since the end of July and 59.0% since April 8th, its all-time closing low. I expect this one to make a new all-time low. The other Canadian LP that worries me is Tilray Brands, which is up 9.0% year-to-date but very expensive in my view. It has quadrupled since its all-time low four months ago. I think it could pull back sharply.

Looking at all 28 members of the Global Cannabis Stock Index, the returns have averaged 11.7% year-to-date, far ahead of the index itself. The median return has been 7.0%, also ahead of the index return:

As I said above, the Global Cannabis Stock index is up just 2.2% year-to-date, which is worse than the return on cash. Stocks outside of the sector are up, with the S&P 500 returning almost 15% so far this year. Cannabis stocks could face pressure if stocks pull back again. I have shared some other reasons too, such as 280E taxation does not end. The cannabis sector is lacking institutional buying and strong growth. It has been pushed by traders recently, but this may not end 2025 well. Be careful!

Sincerely,

Alan

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we published this past week:

Exclusives

To get real-time updates, follow Alan on X.com. You can also share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor calendar.

Based in Houston, Alan leverages his experience as founder of online community

420 Investor, the first and still largest due diligence platform focused on the publicly-traded stocks in the cannabis industry. With his extensive network in the cannabis community, Alan continues to find new ways to connect the industry and facilitate its sustainable growth. At

New Cannabis Ventures, he is responsible for content development and strategic alliances. Before shifting his focus to the cannabis industry in early 2013, Alan, who began his career on Wall Street in 1986, worked as an independent research analyst following over two decades in research and portfolio management. A prolific writer, with over 650 articles published since 2007 at

Seeking Alpha, where he has 70,000 followers, Alan is a frequent speaker at industry conferences and a

frequent source to the media, including the NY Times, the Wall Street Journal, Fox Business, and Bloomberg TV. Contact Alan:

Twitter |

Facebook |

LinkedIn |

Email

Get Our Sunday Newsletter

In This Article:

Canopy Growth, CGC, Cresco Labs, CRLBF, Curaleaf, curlf, glasf, glass house brands, Green Thumb Industries, gtbif, msos, tcnnf, Terrascend, Tilray Brands, TLRY, trulieve, TSNDF, Verano Holdings, vrnof, WEED

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You’re reading this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news. We no longer send these by email as we did in the past, but we post this and all of the newsletters on our website here.

Friends,

Cannabis stocks have retreated substantially since earlier this month and are now down in October. The New Cannabis Ventures Global Cannabis Stock Index, which closed at a value of 7.03, is down 8.5% in October. The year-to-date gain is only 2.2%. After declining four over four consecutive years, the market is close to extending the streak of declines.

MSOS closed at 4.44, which was a 1.5% discount to its NAV, and it has dropped 7.3% in October but is up 16.5% year-to-date. Last week, it was at 5.40, up 41.7% year-to-date and 12.7% in October when I warned about the upcoming financial reports. I discussed the month-to-date returns of the 9 MSOs in the American Cannabis Operators Index, and they ranged from +4.4% to +35.8% then. Now, they are lower, with six of them showing losses.

Looking at the largest 7 positions in MSOS, all in excess of 5%, with two, Curaleaf and Trulieve, above 21%, the best performer is Verano, up 7.7% in October. The three largest positions are all down, with Curaleaf down 3.9%, Trulieve down 8.8% and Green Thumb Industries down 9.9%.

Year-to-date, the three largest positions are very divergent, with one down double-digit and two up substantially:

Looking at the other four large holdings, which range in size from 5.6% to 7.7%, they are all double-digit gainers:

These 7 largest positions in MSOS are all in the Global Cannabis Stock Index, though with much lower holding percentages for a few and lower for all. While they have rallied for the most part in 2025, all of them have declined since the elections last November. As I discussed in last week’s newsletter, the current financials are not exciting at all. What is driving them? Potential rescheduling, which, if it happens, could wipe out 280E taxation.

There is more to the cannabis sector than just the MSOs, some of which have soared since the end of June. The index currently has members from five other sub-sectors, but just one is from Biotech, just one is from THC Beverage and just one is from Canadian Retailers. MSOs make up 26.1% of the index, which is below Ancillaries at 39.1% and above Canadian LPs at 23.8%. I actually like the Ancillaries and still recommend that investors look at the cannabis REITs, which I last discussed here on 8/14.

Earlier this year, I was a big fan of the Canadian LPs, but my exposure in my model portfolio at 420 Investor is in just two names and is slightly lower than the index exposure. Canopy Growth, which I have disliked for a while, is one of the Canadian LPs in the index that I am avoiding. It is down 51.8% in 2025, but it has increased 28.2% since the end of July and 59.0% since April 8th, its all-time closing low. I expect this one to make a new all-time low. The other Canadian LP that worries me is Tilray Brands, which is up 9.0% year-to-date but very expensive in my view. It has quadrupled since its all-time low four months ago. I think it could pull back sharply.

Looking at all 28 members of the Global Cannabis Stock Index, the returns have averaged 11.7% year-to-date, far ahead of the index itself. The median return has been 7.0%, also ahead of the index return:

As I said above, the Global Cannabis Stock index is up just 2.2% year-to-date, which is worse than the return on cash. Stocks outside of the sector are up, with the S&P 500 returning almost 15% so far this year. Cannabis stocks could face pressure if stocks pull back again. I have shared some other reasons too, such as 280E taxation does not end. The cannabis sector is lacking institutional buying and strong growth. It has been pushed by traders recently, but this may not end 2025 well. Be careful!

Sincerely,

Alan

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we published this past week:

Exclusives

To get real-time updates, follow Alan on X.com. You can also share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor calendar.

Get Our Sunday Newsletter

In This Article:

Canopy Growth, CGC, Cresco Labs, CRLBF, Curaleaf, curlf, glasf, glass house brands, Green Thumb Industries, gtbif, msos, tcnnf, Terrascend, Tilray Brands, TLRY, trulieve, TSNDF, Verano Holdings, vrnof, WEED

Related News:

Big Cannabis Companies Are Set to Report Q3 Financials

Don’t Get Excited About the Q3 MSO Financial Reports

Michigan Cannabis Sales Sank in September

Florida’s Medical Cannabis Market Is Struggling