Concentrating Solar Power (CSP) Market

November 28, 2025

Quick Navigation

Report Overview

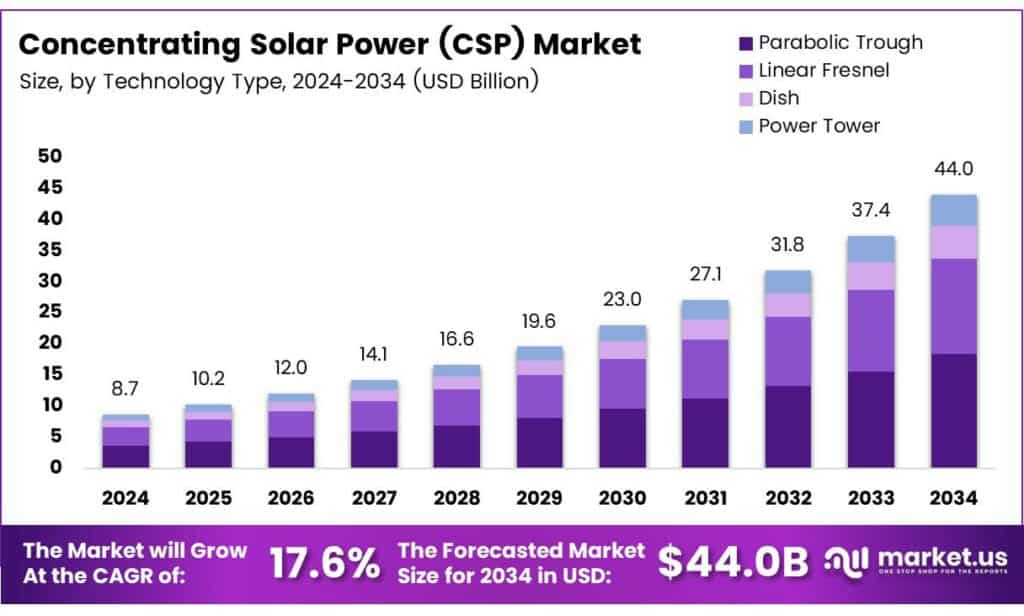

The Global Concentrating Solar Power (CSP) Market size is expected to be worth around USD 44.0 billion by 2034, from USD 8.7 billion in 2024, growing at a CAGR of 17.6% during the forecast period from 2025 to 2034.

Concentrating Solar Power (CSP) is a thermal-based solar technology using mirrors to concentrate sunlight and generate heat for electricity. Unlike photovoltaic systems, CSP integrates thermal energy storage, enabling dispatchable renewable power. Therefore, the CSP market supports grid stability while aligning with long-duration clean energy strategies. CSP adoption rises where land availability, high solar irradiation, and policy backing intersect.

The Concentrating Solar Power (CSP) Market addresses growing demand for firm, utility-scale renewable energy. Globally, energy planners increasingly value technologies supplying power beyond daylight hours. Consequently, CSP fits well in hybrid renewable portfolios with batteries, transmission upgrades, and clean baseload planning for utilities and governments. CSP supports industrial heat applications, desalination, and grid balancing.

- India’s COP26 announcement, the country targets 50% energy decarbonization and 500 GW fossil-fuel-free capacity by 2030. Government-backed solar parks will accelerate CSP deployment by offering land, transmission, water, and roads. These parks enable grid-connected CSP plants ranging from 20 MW to 100 MW, according to India’s COP26 commitments.

Further, according to TERI’s discussion paper, Roadmap to India’s 2030 Decarbonization Target, achieving 500 GW non-fossil capacity is feasible but storage-dependent. TERI highlights CSP with thermal storage as a solution delivering power on demand. Therefore, CSP development becomes essential to meeting India’s 2030 decarbonization goals under tightening energy transition timelines.

CSP presents a strategic opportunity for energy transition planning. Countries targeting net-zero pathways recognize CSP’s ability to provide evening and night-time renewable power. Hence, CSP complements intermittent renewables while reducing grid congestion. This positioning enhances transactional interest from utilities seeking reliability-focused renewable assets.

Key Takeaways

- The Global CSP Market is projected to grow from USD 8.7 billion in 2024 to USD 44.0 billion by 2034, at a 17.6% CAGR.

- Parabolic Trough dominates the market with a 56.2% share due to proven large-scale deployment.

- Storage-based CSP systems lead with a 62.3% share, reflecting demand for dispatchable power.

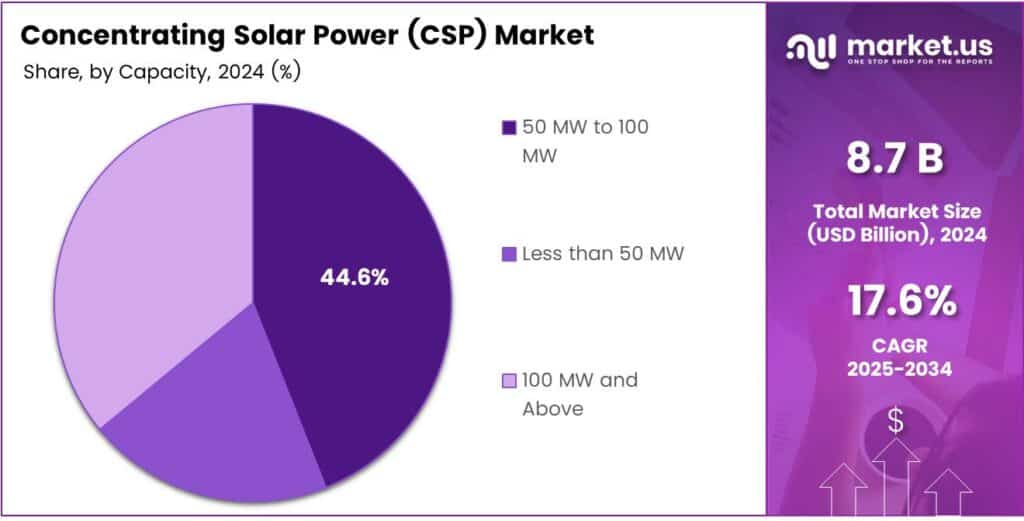

- Projects in the 50 MW to 100 MW range hold the largest share at 44.6%.

- Utilities account for a dominant 76.8% market share, driven by grid-scale electricity needs.

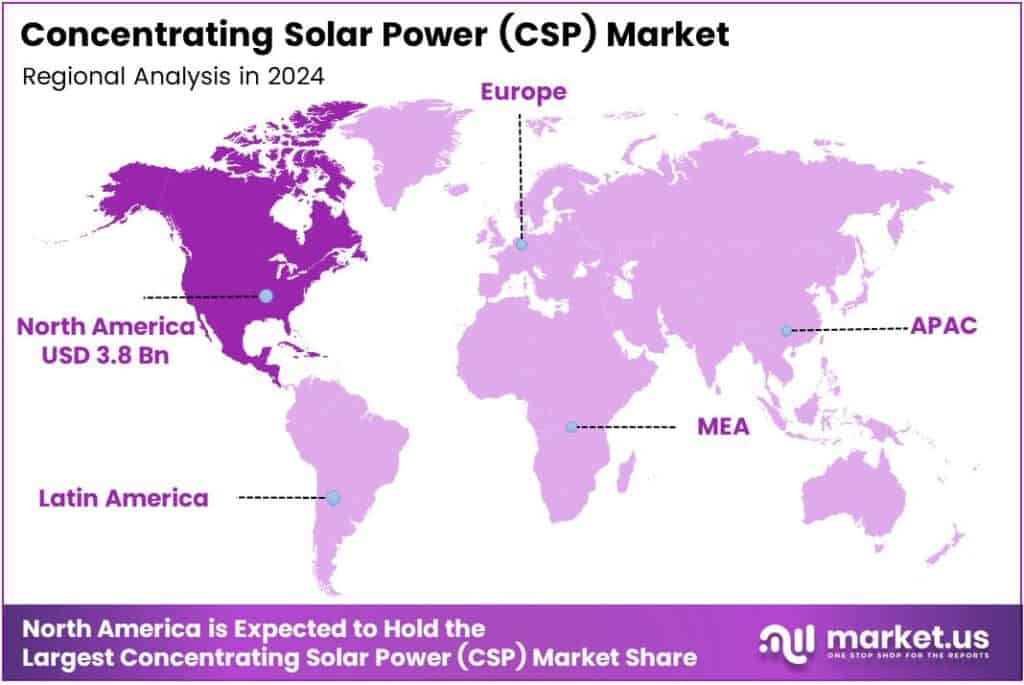

- North America is the leading region, holding 43.8% of the market valued at USD 3.8 billion.

By Technology Analysis

Parabolic Trough dominates the segment with a 56.2% share due to its commercial maturity and proven large-scale deployment.

In 2024, Parabolic Trough held a dominant market position in the By Technology Analysis segment of the Concentrating Solar Power (CSP) Market, with a 56.2% share. It benefits from established supply chains and a long operational history. Consequently, utilities prefer it for predictable output and lower technical risks.

Linear Fresnel technology follows with moderate adoption, driven by simpler design and lower material requirements. However, efficiency limitations slightly restrict its application scope. Still, developers increasingly consider it for cost-sensitive projects with available land and lower thermal requirements.

Dish systems remain niche due to smaller capacity suitability and higher per-unit costs. Even so, they attract interest for remote or off-grid applications. Their modular nature supports decentralized energy generation where grid connections remain limited.

Power Tower technology continues to gain attention due to higher operating temperatures and better storage integration potential. Yet, high capital costs slow widespread adoption. Gradually, innovation and scale improvements are strengthening its long-term commercial outlook.

By Operation Type Analysis

Storage leads the segment with 62.3% share, supported by demand for dispatchable renewable power.

In 2024, Storage held a dominant market position in the By Operation Type Analysis segment of the Concentrating Solar Power (CSP) Market, with a 62.3% share. It ensures energy availability after sunset. As a result, grid operators prioritize CSP plants equipped with thermal storage systems.

Stand-alone systems maintain relevance where immediate power generation is sufficient. However, their dependency on daylight limits flexibility. Still, they serve regions with stable solar patterns and lower grid stability requirements effectively and economically.

By Capacity Analysis

50 MW to 100 MW dominates with a 44.6% share, balancing scalability and investment feasibility.

In 2024, 50 MW to 100 MW held a dominant market position in the By Capacity Analysis segment of the Concentrating Solar Power (CSP) Market, with a 44.6% share. This range suits utility needs while maintaining financial viability. Consequently, it attracts both public and private investments.

Less than 50 MW projects cater to localized demand and pilot installations. Although smaller in scale, they support technology demonstration and regional energy security. Gradually, such projects help build operational experience for newer markets.

100 MW and Above capacity projects represent large national energy initiatives. Despite higher capital intensity, they deliver economies of scale. Over time, supportive policies and financing mechanisms are encouraging gradual expansion in this segment.

By Application Analysis

Utilities dominate with a strong 76.8% share due to large-scale power generation needs.

In 2024, Utilities held a dominant market position in the By Application Analysis segment of the Concentrating Solar Power (CSP) Market, with a 76.8% share. Utilities value CSP for grid stability and long-duration output. Therefore, most CSP investments target centralized power plants.

EOR applications adopt CSP for steam generation in oil recovery operations. This supports fuel savings and emission reduction. Gradually, energy-intensive oil fields are integrating CSP to enhance operational efficiency. Desalination uses CSP for thermal energy in water treatment processes.

Although adoption remains limited, water-scarce regions increasingly explore this option. Over time, energy-water integration strengthens project feasibility. Other applications include industrial heat and hybrid systems. While smaller in scale, they showcase CSP’s versatility.

Key Market Segments

By Technology

- Parabolic Trough

- Linear Fresnel

- Dish

- Power Tower

By Operation Type

- Stand-alone

- Storage

By Capacity

- Less than 50 MW

- 50 MW to 100 MW

- 100 MW and Above

By Application

- Utilities

- EOR

- Desalination

- Others

Emerging Trends

Thermal Energy Storage Advancements Shape Key CSP Market Trends

The most important trend in the CSP market is the increasing focus on thermal energy storage. Developers are extending storage duration to supply electricity for longer hours. This trend strengthens CSP’s role as a flexible renewable source supporting grid reliability.

- Dry-cooling technology is gaining attention as well. To address water scarcity, newer CSP projects increasingly use air-cooled systems. This trend allows deployment in arid regions while meeting environmental requirements. Digital monitoring and automation are also shaping the market. The total global installed CSP capacity reached 7.2 GW, with 350 MW of new CSP generation capacity added to the grid that year.

Finally, government-backed mega projects are setting benchmarks. Large CSP plants with integrated storage are proving technical viability at scale. These projects help build confidence, encourage learning, and support long-term market development worldwide.

Restraints

High Capital Cost and Long Construction Timelines Restrain CSP Market Expansion

The biggest restraint for the Concentrating Solar Power market is its high upfront cost. CSP plants require mirrors, receivers, thermal storage, and large land areas. These factors increase initial investment compared with solar PV and wind projects. Long construction timelines also slow adoption.

CSP plants are complex to design and build, often taking several years from approval to commissioning. This creates delays in revenue generation and discourages private investors seeking faster returns. Water usage is another concern, especially in desert regions where CSP potential is highest.

Traditional wet-cooling systems consume significant water, raising environmental and social challenges. Although dry-cooling options exist, they add extra cost and reduce efficiency. Policy uncertainty further restrains growth. CSP depends heavily on long-term power purchase agreements and government support.

Drivers

Rising Demand for Clean, Dispatchable Renewable Power Drives CSP Market Growth

Concentrating Solar Power is mainly driven by the need for clean electricity that can also support the grid after sunset. Unlike solar PV, CSP systems store heat and produce power when required. This makes them attractive for countries facing evening peak demand and grid stability challenges.

- Many sun-rich regions depend on imported fossil fuels. CSP plants use local solar resources and reduce fuel imports. Governments in the Middle East, North Africa, and parts of Asia view CSP as a strategic asset for reducing exposure to fuel price volatility. The global CSP capacity rose by 400 MW to reach 6.7 GW — part of this growth was driven by new plants designed with thermal storage and hybrid configurations.

Climate commitments are also pushing adoption. Countries working toward net-zero targets need technologies that cut emissions from power generation. CSP produces electricity without direct emissions and fits well into national decarbonization roadmaps focused on utility-scale projects.

Growth Factors

Hybrid Energy Systems Create Strong Growth Opportunities for the CSP Market

One of the biggest opportunities for CSP lies in hybrid projects. Combining CSP with solar PV, wind, or battery storage creates reliable, round-the-clock renewable power plants. These hybrids can replace fossil fuel baseload power in remote or weak grid regions.

Emerging markets present another opportunity. Countries in Africa, the Middle East, and South Asia have high solar radiation and rising electricity demand. CSP can meet large-scale power needs while supporting economic development and job creation. Industrial heat applications offer new revenue streams. CSP can provide high-temperature heat for desalination, hydrogen production, and industrial processes.

This expands its role beyond electricity and improves overall project viability. Technology standardization is also opening doors. As components become more standardized and locally manufactured, costs can decline. This creates room for wider adoption and attracts both public and private investment into CSP infrastructure.

Regional Analysis

North America Dominates the Concentrating Solar Power (CSP) Market with a Market Share of 43.8%, Valued at USD 3.8 Billion

North America leads the CSP market due to early technology adoption, strong federal clean-energy funding, and grid reliability needs. In this region, CSP holds a dominant share of 43.8%, with the market valued at around USD 3.8 billion, supported by thermal storage integration and utility-scale solar investments. Long-term decarbonization targets and transmission upgrades continue to reinforce regional demand.

Europe remains a key CSP region, driven by strict carbon-reduction mandates and long-standing solar thermal expertise. Southern European countries support CSP deployment for grid stability, especially where solar irradiance is high. Policy-backed renewable targets and hybrid solar-storage systems sustain steady regional growth.

Asia Pacific is emerging as a growth hub for CSP, supported by rising electricity demand and large-scale solar park development. Governments promote CSP to complement photovoltaic capacity and improve dispatchability. Growing interest in thermal energy storage strengthens long-term adoption potential.

The U.S. represents a major contributor within North America, supported by federal tax incentives and renewable energy mandates. CSP facilities with thermal storage enhance grid resilience during peak demand hours. Continued infrastructure spending and clean-energy policy alignment sustain the country’s strategic role in CSP deployment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In the global Concentrating Solar Power market, Abengoa is often viewed as a benchmark for complex, integrated CSP projects. The company’s experience with large-scale parabolic trough and tower plants positions it as a technology and EPC reference, especially in grid-connected, dispatchable solar power. Its track record helps de-risk new projects for investors and regulators in emerging CSP regions.

Siemens Energy plays a critical role more on the technology and systems side than as a project developer. Its turbines, control systems, and grid integration solutions are central to making CSP plants reliable and compatible with modern, flexible power systems. This gives Siemens Energy influence over performance standards, efficiency targets, and lifetime economics of CSP assets.

Acciona brings strong credentials as an integrated renewable infrastructure player, combining project development, construction, ownership, and operations. In CSP, it leverages multi-technology experience across wind, PV, and storage to structure bankable hybrid projects. This integrated positioning allows Acciona to respond to policy shifts, tenders, and corporate PPAs where CSP must compete within broader clean-energy portfolios.

Aalborg CSP is strategically important in niche but fast-growing applications such as industrial process heat, district heating, and hybrid solar-thermal systems. Rather than chasing only mega-scale power plants, the company focuses on thermal system design and heat-exchanger expertise. This opens opportunities in decarbonizing heat for industry and cities, where CSP’s high-temperature capability can complement electrification and help create diversified, long-term demand for CSP technology.

Top Key Players in the Market

- Abengoa

- Siemens Energy

- Acciona

- Aalborg CSP

- ACWA POWER

- Torresol Energy

- Enel Spa

- Trivelli Energia srl

- Grün leben GmbH

Recent Developments

- In 2024, Abengoa’s official website highlights its ongoing involvement in solar thermal projects, including EPC services and O&M for parabolic trough and central receiver technologies, but no new CSP-specific announcements were identified post-2020. General solar thermal innovation efforts continue.

- In 2024, Siemens Energy remains a key player in CSP steam turbine and generator technologies, having equipped over 70 CSP plants globally. The company achieved full commercial operations for Noor Energy 1, the world’s largest single-site hybrid CSP-PV project at Dubai’s Mohammed bin Rashid Al Maktoum Solar Park, utilizing molten salt storage for 24/7 dispatchable power.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 8.7 billion |

| Forecast Revenue (2034) | USD 44.0 billion |

| CAGR (2025-2034) | 17.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Parabolic Trough, Linear Fresnel, Dish, Power Tower), By Operation Type (Stand-alone, Storage), By Capacity (Less than 50 MW, 50 MW to 100 MW, 100 MW and Above), By Application (Utilities, EOR, Desalination, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Abengoa, Siemens Energy, Acciona, Aalborg CSP, ACWA POWER, Torresol Energy, Enel Spa, Trivelli Energia srl, Grün leben GmbH |

| Customization Scope | Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}