Down 15% From All-Time Highs, Is Meta Platforms Stock a Good Buy Right Now?

January 11, 2026

- AI Infrastructure: Meta is ramping up capital expenditures to $70-72 billion in 2025, with even larger growth expected in 2026.

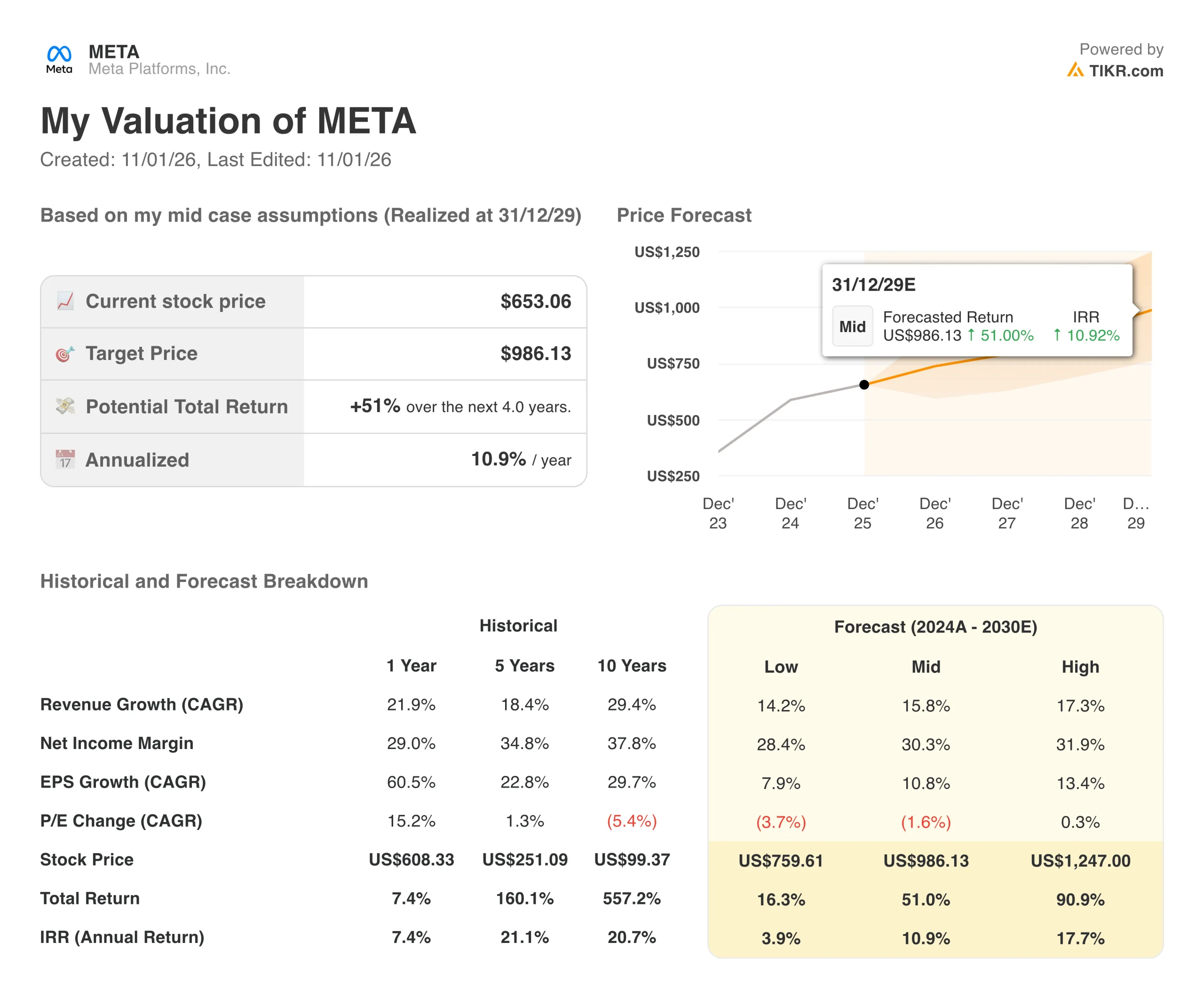

- Price Projection: Based on current momentum, the stock could reach $815 by December 2027.

- Potential Gains: This target implies a total return of 25% from the current price of $653.

- Annual Return: Investors could see roughly 12% growth per year over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Meta (META) isn’t just building AI products—it’s constructing the infrastructure for the next computing era. With 3.5 billion people using at least one of its apps daily, and Meta AI reaching 1 billion monthly users, the company is transforming from a social media giant into an AI-powered platform.

Total revenue in Q3 of 2025 hit $51.2 billion, up 26% year-over-year. Meta Superintelligence Labs is building what CEO Mark Zuckerberg calls “the highest talent density lab in the industry,” while the annual revenue run rate through AI-powered ad tools has reached $60 billion.

Despite this momentum, META stock is trading at $653, down 15% from its all-time high, creating an opportunity for investors who understand where Meta is heading.

See analysts’ full growth forecasts and estimates for Meta stock (It’s free) >>>

We analyzed Meta’s future through the lens of its aggressive AI infrastructure buildout and engagement improvements.

By front-loading capacity for superintelligence while driving immediate gains in recommendation systems, Meta is positioning itself as the essential AI layer for billions of users.

Using a forecast of 18.3% annual revenue growth and 37.4% operating margins, our model projects the stock will rise to $815 within 2 years. This assumes a 21x Price-to-Earnings (P/E) multiple.

That represents a slight compression from Meta’s current P/E of 22.1x. As the company scales AI infrastructure and absorbs higher depreciation costs, some multiple compression is reasonable.

The real value comes from sustained revenue growth and expanding user engagement, not multiple expansion.

Estimate a company’s fair value instantly (Free with TIKR) >>>

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for META stock:

Meta’s revenue engine is firing on multiple cylinders, driven by AI improvements across ads and engagement.

Engagement Momentum: Time spent on Facebook increased 5% in Q3, while Threads grew 10%. Video time on Instagram jumped over 30% year-over-year. These improvements stem from better AI recommendations and the surfacing of fresh content.

Ad Performance: The company is consolidating hundreds of specialized models into fewer, more capable systems. This shift is driving conversion rates higher while reducing complexity. Meta has already cut 100 ad ranking models through its Lattice architecture.

Business Messaging: Click-to-WhatsApp ads grew 60% year-over-year. Business AIs are now handling millions of conversations, with rollouts expanding across markets.

Meta’s margin profile faces near-term pressure from infrastructure investments but shows long-term expansion potential.

Infrastructure Efficiency: The company is seeing 2x price-performance gains per hardware generation and 10x gains per model generation through software optimizations. This means more revenue per dollar of infrastructure.

Capital Allocation: About half of Q3 spending went to short-lived assets (servers) that match contract durations. The other half funds data centers with 15+ year lifespans, providing sustained capacity.

Model Improvements: Consolidating specialized models into unified systems is driving both performance gains and cost efficiencies. Meta cut 100 models in recent quarters and plans to consolidate 200 more.

The market currently values Meta at 22.1x earnings. We chose 21x for our exit multiple to stay conservative.

Quality Premium: Meta deserves a premium to the market average due to its scale (3.5 billion daily users), network effects, and AI leadership position.

Investment Cycle: As infrastructure spending peaks and depreciation increases, some multiple compression is natural. However, the company’s free cash flow generation ($10.6 billion in Q3) supports the valuation.

Build your own Valuation Model to value any stock (It’s free!) >>>

AI infrastructure buildouts carry uncertainty. Here is how Meta stock might perform in different scenarios through 2027:

- Low Case: If revenue growth slows to 14.2% and margins compress to 28.4%, the stock still offers a 4% annual return.

- Mid Case: With 18.3% growth and 37.4% margins (our base assumptions), we expect a 11% annual return.

- High Case: If AI adoption accelerates and Meta captures 31.9% margins while growing at 17.3%, returns could hit 18% annually.

See what analysts think about META stock right now (Free with TIKR) >>>

The range reflects different AI monetization curves. In the low case, infrastructure investments outpace revenue gains, pressuring margins. In the high case, Meta’s recommendation systems and new AI products drive faster monetization than expected.

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}