Empowering Poland: The role of international partnerships

December 23, 2024

- Poland, a country historically reliant on energy imports, has proactively engaged in international cooperation to boost its energy security.

- This cooperation extends beyond mere imports to include the exchange of technology and expertise, policy harmonisation, and joint investments.

- These collaborative initiatives are crucial for Poland’s energy transition and essential for achieving energy sovereignty.

- This paper examines Poland’s key international partnerships in energy generation, covering fossil fuels and renewable energy sectors, such as wind, solar, hydrogen, and nuclear power plants.

- It also identifies areas with untapped potential for further cooperation.

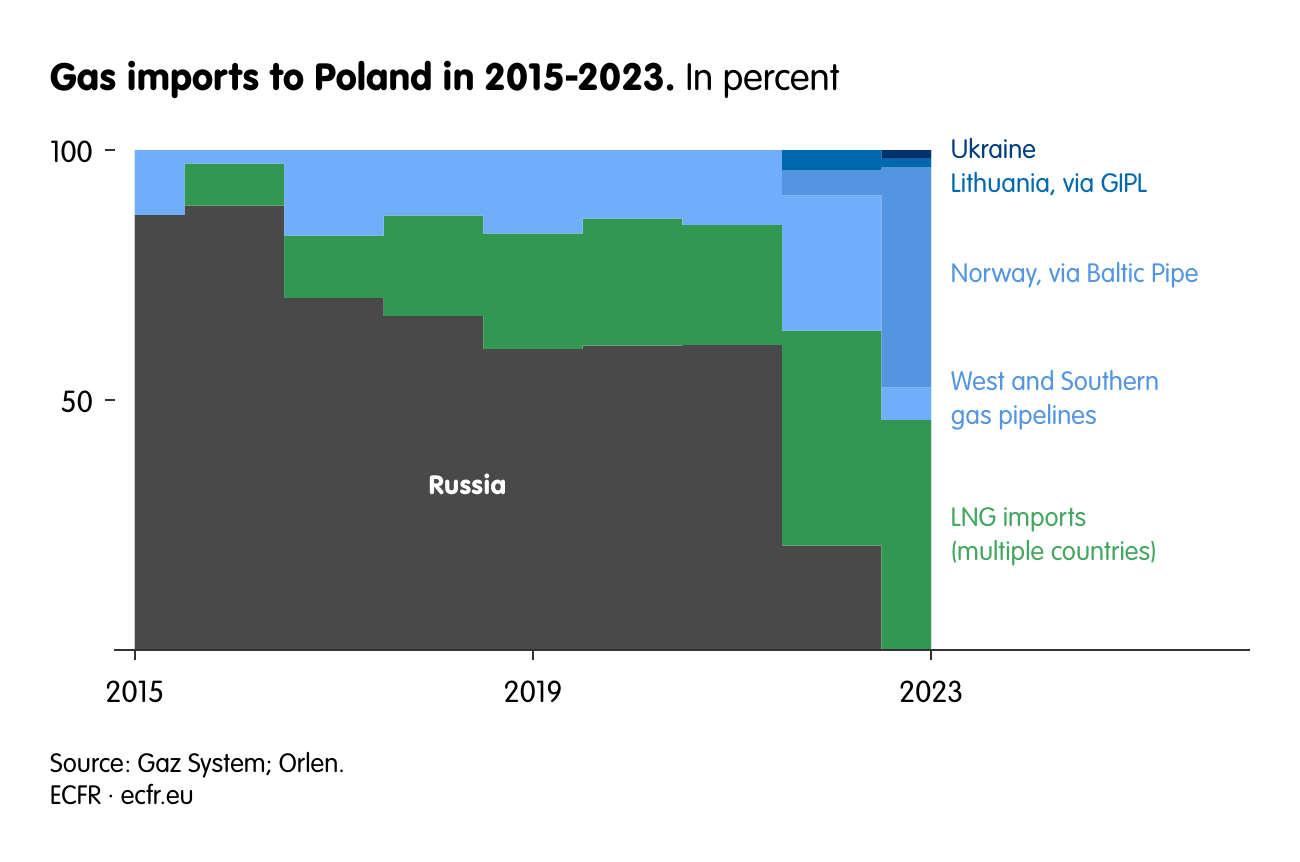

Although Poland has some fossil fuel deposits, mainly coal and to a lesser extent gas and oil, they are not sufficient in terms of consumption needs. Therefore, Poland is heavily dependent on fossil fuel imports, with a significant share historically coming from Russia. In 2016, nearly 89% of Poland’s gas and oil imports came from Russia.

Years before Russia’s invasion of Ukraine in 2022, Poland had been preparing to reduce its dependency on Russian energy supplies. As early as 2016, decision-makers signalled that Poland would not extend its long-term contract with Gazprom after its expiration in 2022.

Since then, Poland has taken several steps to diversify gas supply sources.

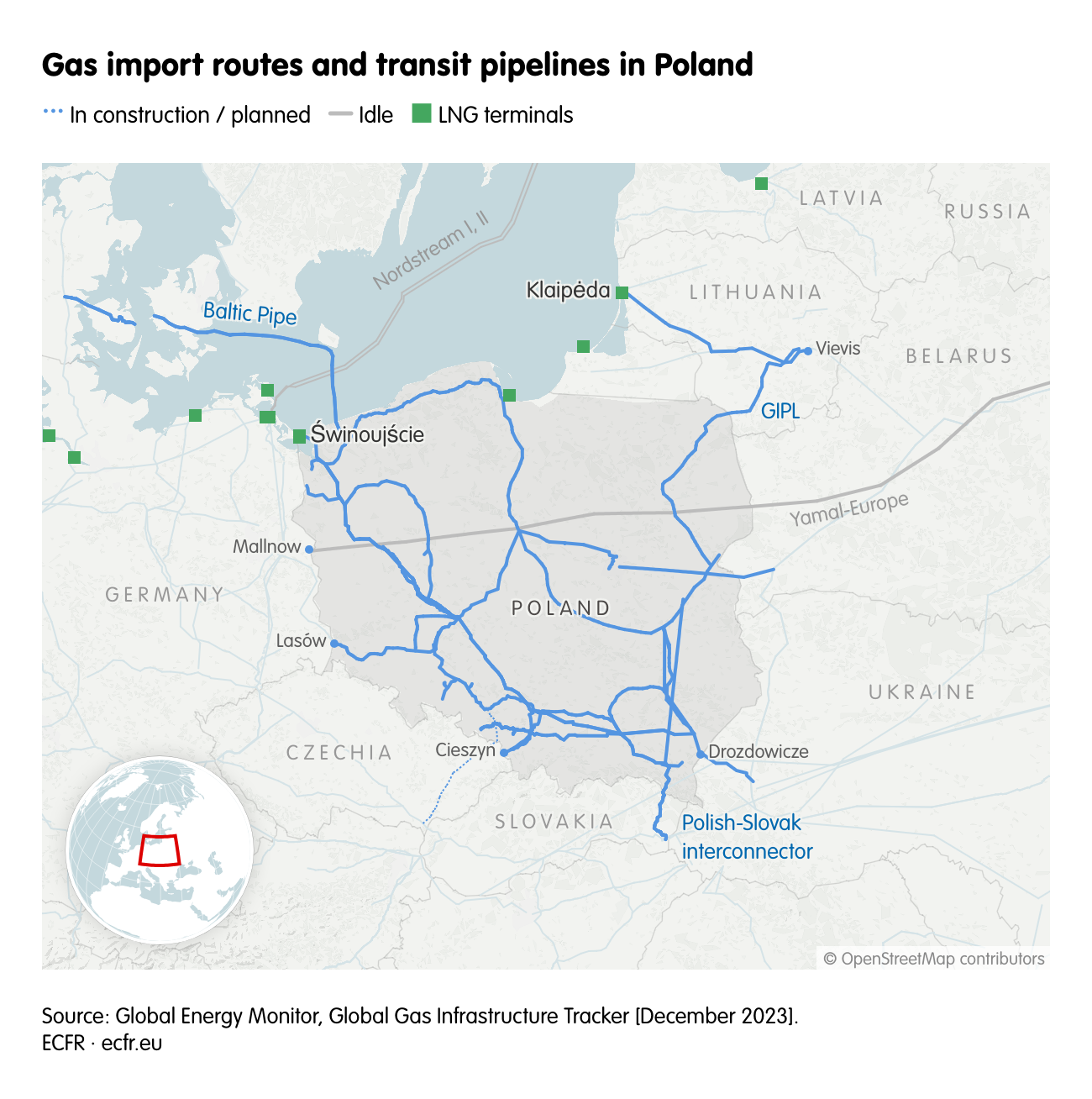

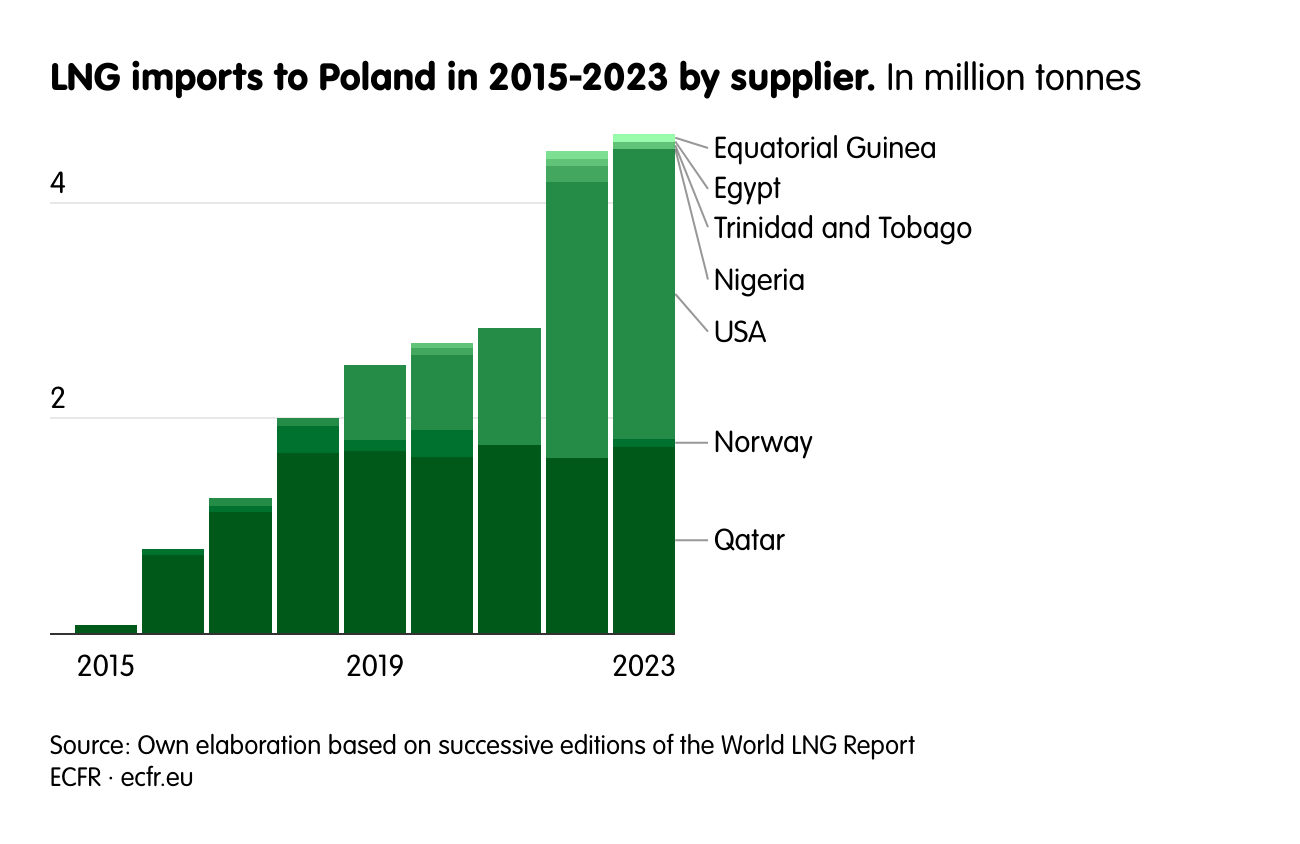

The first step was the regasification of the terminal in Świnoujście in 2015, from where Poland now imports liquefied gas (LNG) from many countries, such as the USA, Qatar, or Norway.

Another major step was building the Baltic Pipe gas pipeline, launched in September 2022, which enables gas imports from Norway via Denmark.

The gas interconnector between Poland and Lithuania (GIPL), launched in May 2022, was also key. Thanks to it, Poland gained access to the Lithuanian LNG terminal in Klaipeda. In the future, GIPL may also be used for hydrogen transport, as already signalled by the Lithuanian operator.

The Polish-Slovak gas interconnector, commissioned in November 2022, is another key link in the North-South gas corridor. It allows Poland to export gas sourced from the Świnoujście terminal to the south and to import gas from LNG terminals and fields in Greece, Turkey, Croatia, the Mediterranean, and the Caucasus via Slovakia, Hungary, and Romania.

With these infrastructure investments, Poland was well prepared when Gazprom first stopped gas exports to Poland in April 2022 (even though the long-term contract was expiring at the end of 2022).

As seen above, the inauguration of Baltic Pipe in 2022 turned Norway into currently one of Poland’s main gas suppliers. But Poland also increased its LNG imports, primarily from the United States. These supplies are based on several long-term contracts that Polish energy companies PGNiG and Orlen have signed with US companies between 2018 and 2023.

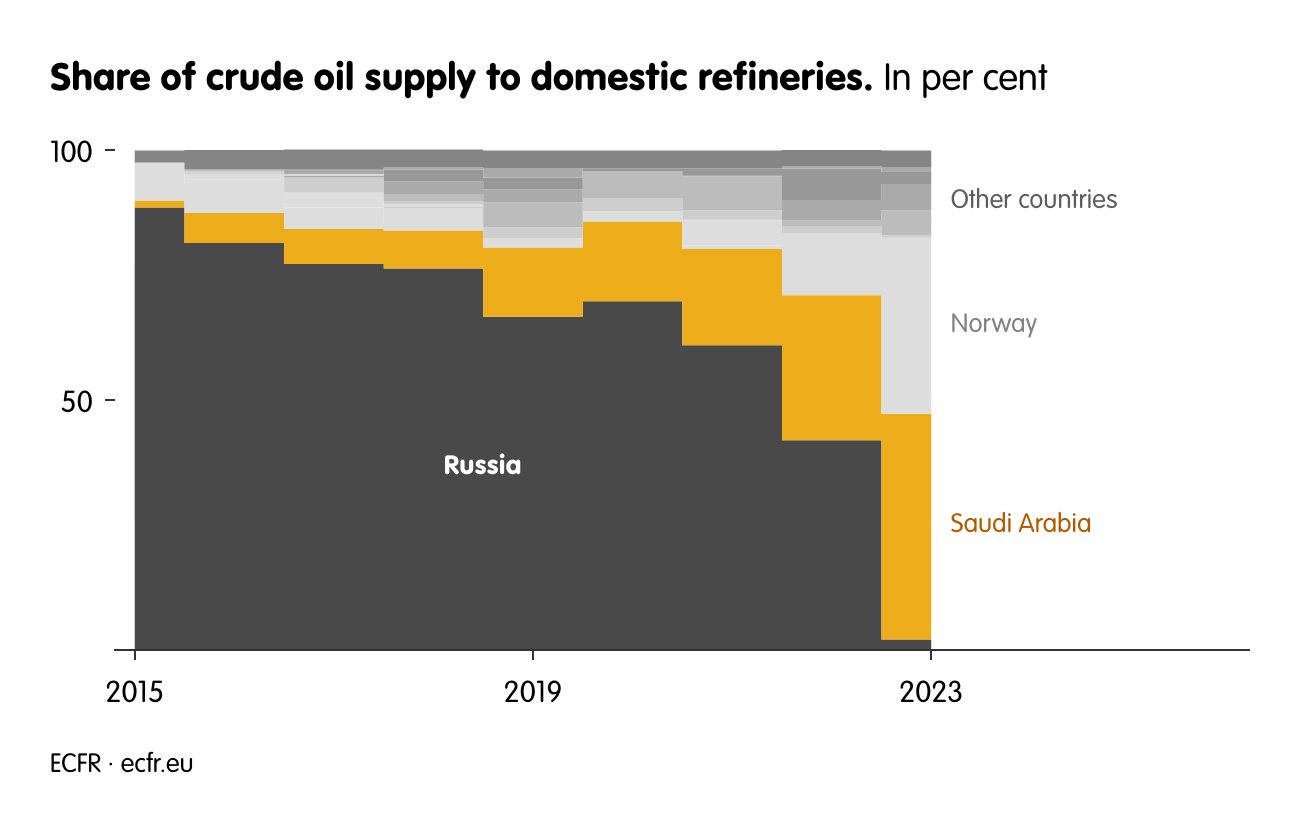

Poland has also been gradually reducing its dependency on Russian oil since 2015, with a dramatic decline in imports after the 2022 invasion of Ukraine. By 2023, Norway emerged as Poland’s second-largest oil supplier after Saudi Arabia. Poland sees fossil fuels from Norway as not only more valuable than those from Russia in terms of security but also more environmentally friendly. This is because Norway uses lower-emission, mostly electrified extraction methods on the Norwegian Continental Shelf.

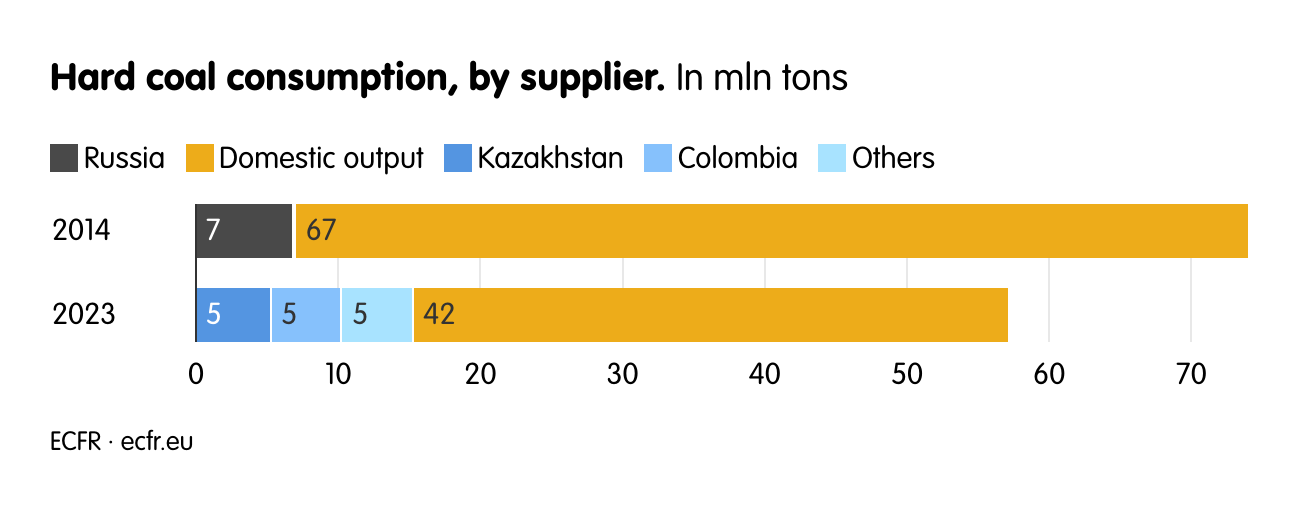

Poland is not only systematically reducing the level of hard coal consumption but is also diversifying its trade partners. Poland’s coal imports from Russia fell to zero following the introduction of EU sanctions on Russian goods.

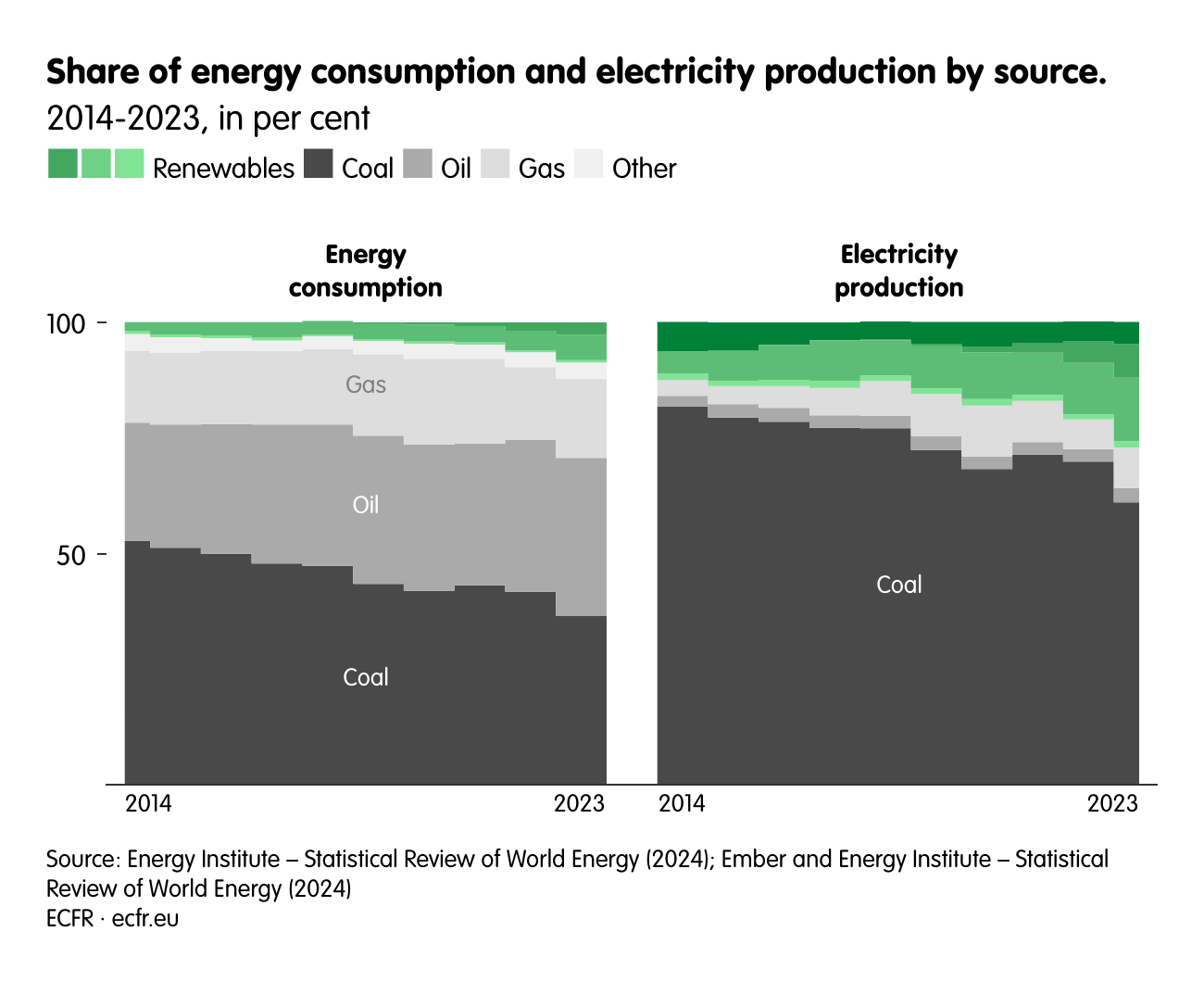

Despite diversifying its fossil fuel supplies and experiencing an overall decrease in dependency, Poland remains heavily reliant on fossil fuels. The next challenge for the country is to accelerate the adoption of renewable energy.

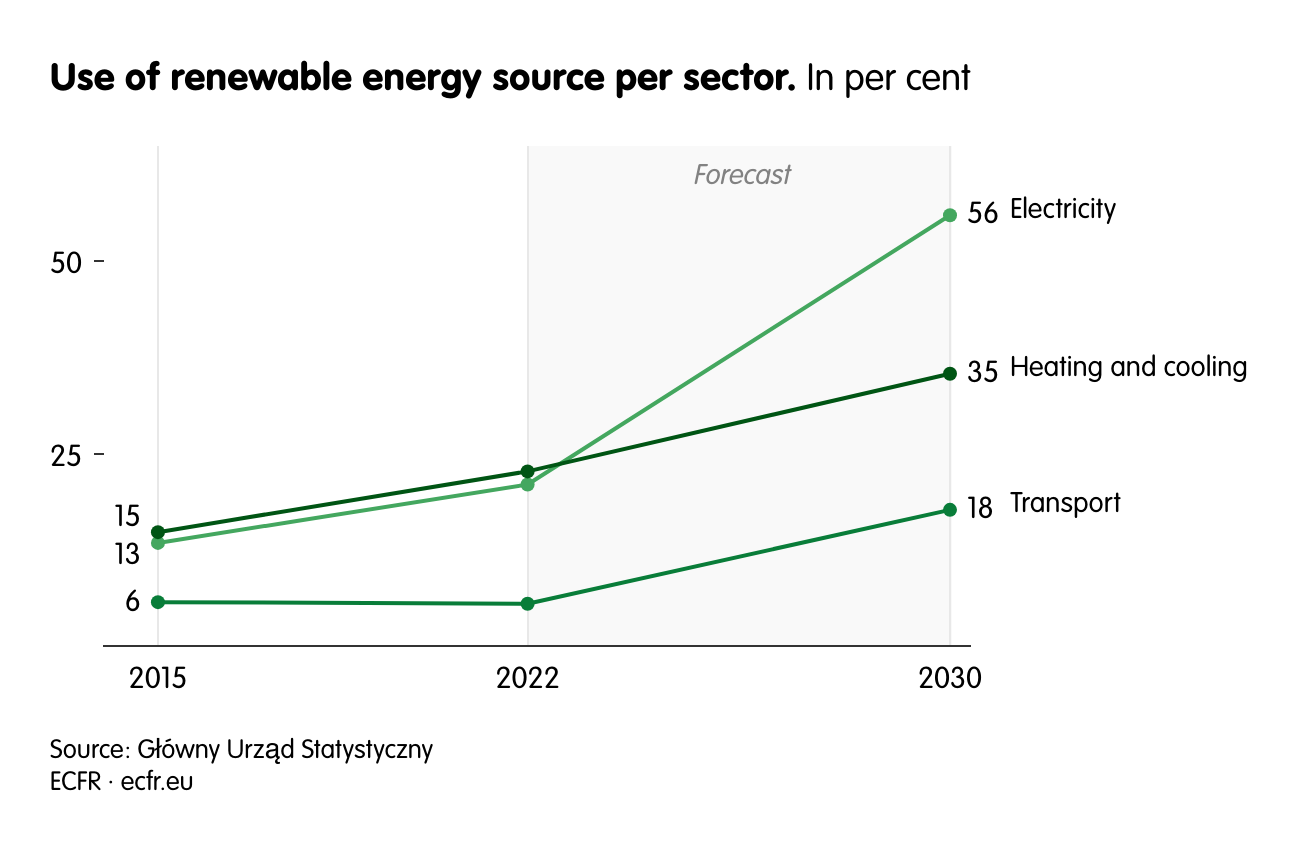

In the draft of the National Energy and Climate Plan (NEPC) presented to the European Commission in September 2024, the so-called ambitious scenario, Poland aims to significantly increase the share of renewable energy sources across the electricity, transportation, and heating and cooling sectors by 2030. To achieve this goal, the Polish government is investing PLN 792 billion in various renewable projects, including wind farms, solar power plants, biomass and biogas facilities and hydroelectric plants.

The overarching objective is to reduce emissions across the economy by 2030 by just over 50% compared to 1990. The government points out that failing to transition will ultimately incur higher costs than the investment necessary to transition. The average annual outlay for transformation is around PLN 158 billion, while the annual cost of maintaining the status quo (including fossil fuel imports, costs related to mitigating smog, costs associated with consequences of natural events, and the value of additional CO2 emissions allowances) would amount to PLN 259 billion yearly.

Although Poland’s energy transition is primarily a national effort, international cooperation can accelerate this transformation. To ensure the energy policy is as effective as possible from the point of view of Poland, it is necessary to cultivate relations with those partners that offer the country comprehensive benefits in the energy sector.

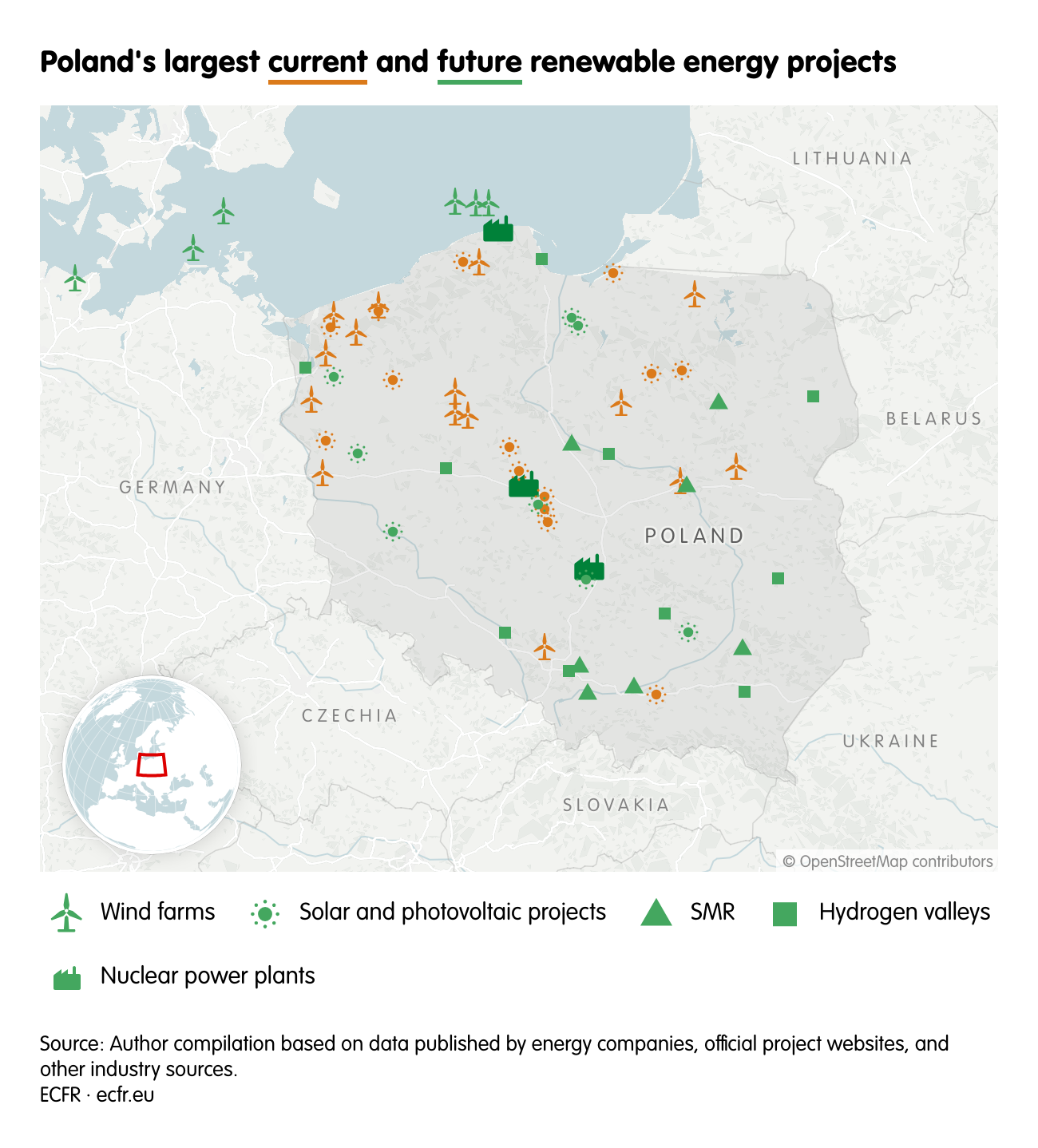

Foreign investors are heavily involved in the development of both onshore and offshore wind energy in Poland. According to the 2023 data, while Poland’s PGE and Polenergia have the most installed wind capacity, international firms such as Germany’s RWE Renewables, Portugal’s EDP Renewables, and French companies Mirova Anemoska and Qair are all actively contributing to Poland’s wind generation industry.

For large offshore wind power development, however, Poland has two major partners that will be essential for the country’s energy transition.

The Norwegian company Equinor is investing in the construction of the three offshore wind farms – Baltic I, Baltic II and Baltic III – in partnership with the Polish company Polenergia. Collectively, the three offshore wind projects are expected to have a capacity of 3,000 MW, accounting for half of the total generating capacity of offshore wind farms planned to be commissioned by Poland by 2030.

In addition, Equinor, through its subsidiary Wento, owns one onshore wind farm and three large photovoltaic farms in Poland, which together produce a total of 280 GWh of electricity, sufficient to meet the needs of 140,000 households. Ultimately, all renewable energy projects by Equinor will have a total capacity of 1.6 GW.

The company Danske Commodities, an energy trading company established in Denmark but 100% owned by Equinor since 2019, is active in selling energy on the Polish energy market. Norwegian company Statkraft, one of Europe’s leaders in green energy production, has a project portfolio of 500 MW in Poland and plans to double that capacity by 2030.

Poland is also the largest beneficiary of Norwegian and EEA funds, which serve as a vital financial resource for the country’s energy transition. These funds, provided by Iceland, Norway, and Liechtenstein, are allocated to a dozen central and southern European countries and the Baltic States in the form of non-refundable aid. Among these, Poland has received the most substantial support, with €809.3 million designated from a total pool of €2.8 billion available for 14 EU countries.

PGE Group, one of Poland’s largest energy companies, is constructing a massive offshore wind project in the Baltic Sea in partnership with the Danish company Ørsted – Baltica Offshore Windfarm, planned to launch in 2030. The project will be implemented in two stages, Baltica 2 and Baltica 3, with a generating capacity of 1.5 GW and 1 GW, respectively. After 2030, the Baltica 1 Wind Farm, with a generating capacity of approximately 0.9 GW, will be added to the portfolio. By acquiring new areas for development in the Baltic Sea, the PGE Group will be able to build further offshore wind farms by 2040.

All three offshore wind farms will provide energy to almost 4 million households in Poland, nearly a third of the total number of households in the country, while avoiding about 8 million tonnes of CO2 emissions per year.

Denmark is also a major supplier of wind turbine imports to Poland, with imports totalling 10.5 million EUR in 2023. The Danish company Vestas, which holds over 16% of the global market in this sector, plans to build a wind turbine blade factory in Szczecin, set to be completed in 2026. The factory will produce turbine blades for both export as well as to renewable energy projects in Poland, including the Baltic Power offshore wind farm.

In addition, Danish company Rambøll has been selected to develop the design for the Baltic II and Baltic III offshore wind farm locations and serves as PGE’s technical advisor for all its offshore wind farm projects. European Energy, another large energy company, is also present in the Polish market, boasting 130 MW of installed capacity in wind and solar in Poland, and more than 5 GW of projects in development (solar, wind, and energy storage).

Cooperation with Denmark is pivotal to accelerating the energy transition in Poland and has the potential to facilitate advancements in other areas too. In April 2023, the gas system operators of Denmark and Poland – Energinet and Gaz-System – signed a memorandum of understanding on accelerating the energy transition and strengthening regional energy security. The agreement addresses both issues related to gas supply through the Baltic Pipe (which runs through Danish territory) and the development of zero-carbon energy projects, including biomethane and hydrogen.

The United States has emerged as a major partner in the Polish nuclear programme, the implementation of which could make a significant contribution to Poland’s energy transition.

Following a 2020 agreement of cooperation in the field of civil nuclear energy, the Polish government selected Westinghouse Electric Company’s AP1000 technology for the construction of Poland’s first nuclear power plant, which will have the participation of Polskie Elektrownie Jądrowe. In September 2023, UScompanies Westinghouse Electric Company and Bechtel signed agreements to form a consortium focused on the design and construction of this facility.

According to a PWC report commissioned by Westinghouse, the construction of six AP1000 units in Poland would result in a 39% reduction in CO2 emissions compared to current emissions from power generation sources, while providing emission-free energy to more than 13 million households. The US is also being considered as a partner in plans to build a second large nuclear power plant in Poland.

Moreover, US companies are seen as important partners in the development of Small Modular Reactors (SMRs) in Poland. Polish company Orlen has been included in the US Phoenix Initiative, a government programme supporting Europe’s transition from fossil fuels to SMR reactors. In total, the US plans to allocate 2 million dollars from the Phoenix programme to projects in Poland, the Czech Republic and Slovakia.

OSGE, a joint venture between the Polish companies Orlen and Synthos, is currently considering seven future SMR locations in Poland, with Canadian company Laurentis Energy Partners as a potential partner. On 14 November 2024, OSGE signed an agreement to collaborate with Laurentis Energy Partners on the creation of a PSAR, the initial safety report required to begin licensing SMR technology.

For now, however, there are not many details on specific SMR projects.

The European Commission’s REPowerEU plan set an ambitious target of producing 35 billion cubic metres (bcm) of biomethane by 2030, with more recent analyses suggesting that production could reach as high as 44 bcm by that time and grow to 165 bcm by 2050. By 2040, Poland is projected to rank as the fifth largest producer of biomethane in Europe, producing over 8bcm.

Achieving these goals will largely depend on favourable political and legal conditions, as well as advancements in technology to optimise green fuel production.

Ukraine presents a significant opportunity for Poland in biomethane collaboration. With the capability to produce up to 22 bcm of biomethane annually, Ukraine can leverage its existing infrastructure, abundant feedstock resources, and extensive arable land for agricultural biomethane production, positioning it as a key exporter to the EU.

Poland and Ukraine have established several key agreements in recent years. On March 16, 2023, GAZ-SYSTEM and the Ukrainian transmission system operator GTSOU signed a memorandum of understanding to develop gas infrastructure and support the transmission of natural gases, including biomethane and hydrogen.

To facilitate this international partnership, regulatory changes in Ukraine are also playing a crucial role. In March 2024, the Ukrainian parliament enacted a law to streamline the customs control and clearance processes for biomethane transported via pipeline, aligning them with those of natural gas.

The potential for international cooperation on energy storage remains largely underdeveloped, with most activity so far involving non-binding talks on joint projects.

But a notable example so far came in December 2023, when Enea Group, a leading Polish energy company, and Spain’s Grupo Cobra, a global leader in industrial engineering and specialised services in the energy sector,signed a letter of intent to develop cooperation in energy storage. This agreement marks the beginning of cooperation for the development of energy storage projects and technologies. The goal is to exchange expertise to launch a pilot energy storage project, working with a large number of renewable energy sources connected to Enea’s distribution network.

Such potential is also underexplored by Dutch companies, which are at the forefront of developing large-scale storage projects in Europe.

Hydrogen is poised to play a pivotal role in achieving climate neutrality by replacing gas and functioning as a means of energy storage. In November 2024, the Polish Parliament approved the Energy Law Amendment Act establishing a regulatory framework for the country’s hydrogen market. It defines key terms such as renewable and low-emission hydrogen and outlines rules for certification, licensing, and system management. The act facilitates the creation of hydrogen system operators, including those for transmission and distribution, and supports research and development in hydrogen technology. It also simplifies hydrogen infrastructure construction to accelerate sector growth. Hydrogen transmission through the gas network remains governed by gas legislation, with provisions allowing doping.

One notable initiative is Poland’s participation in the Nordic-Baltic Hydrogen Corridor project, which is listed as a Project of Common Interest (PCI) under the Baltic Energy Market Interconnection Plan (BEMIP). This project aims to develop hydrogen infrastructure throughout the Baltic region to meet the REPowerEU 2030 targets. Following the finalisation of the pre-feasibility study in 2024, the six transmission system operators are starting to work on national-level feasibility studies. These studies will focus on key aspects, including the pipeline route, compressor station location planning, financial and economic analysis, environmental permitting and safety issues, as well as project timing issues. The work will last until mid-2026.

In June 2024, Gaz System, the Polish gas network operator, signed a memorandum of understanding with eight regional operators to collaborate in developing a hydrogen network and market in the area. The signatories include gas network operators from Poland, Estonia, Denmark, Finland, Lithuania, Sweden, Germany, and Latvia. This cooperation aims to coordinate the efforts of gas transmission system operators in developing hydrogen transmission and storage infrastructure, facilitating the exchange of information regarding the hydrogen market and projects related to the production and demand for renewable hydrogen. The parties also plan to collaborate with European and national institutions within the framework of the EU’s BEMIP initiative.

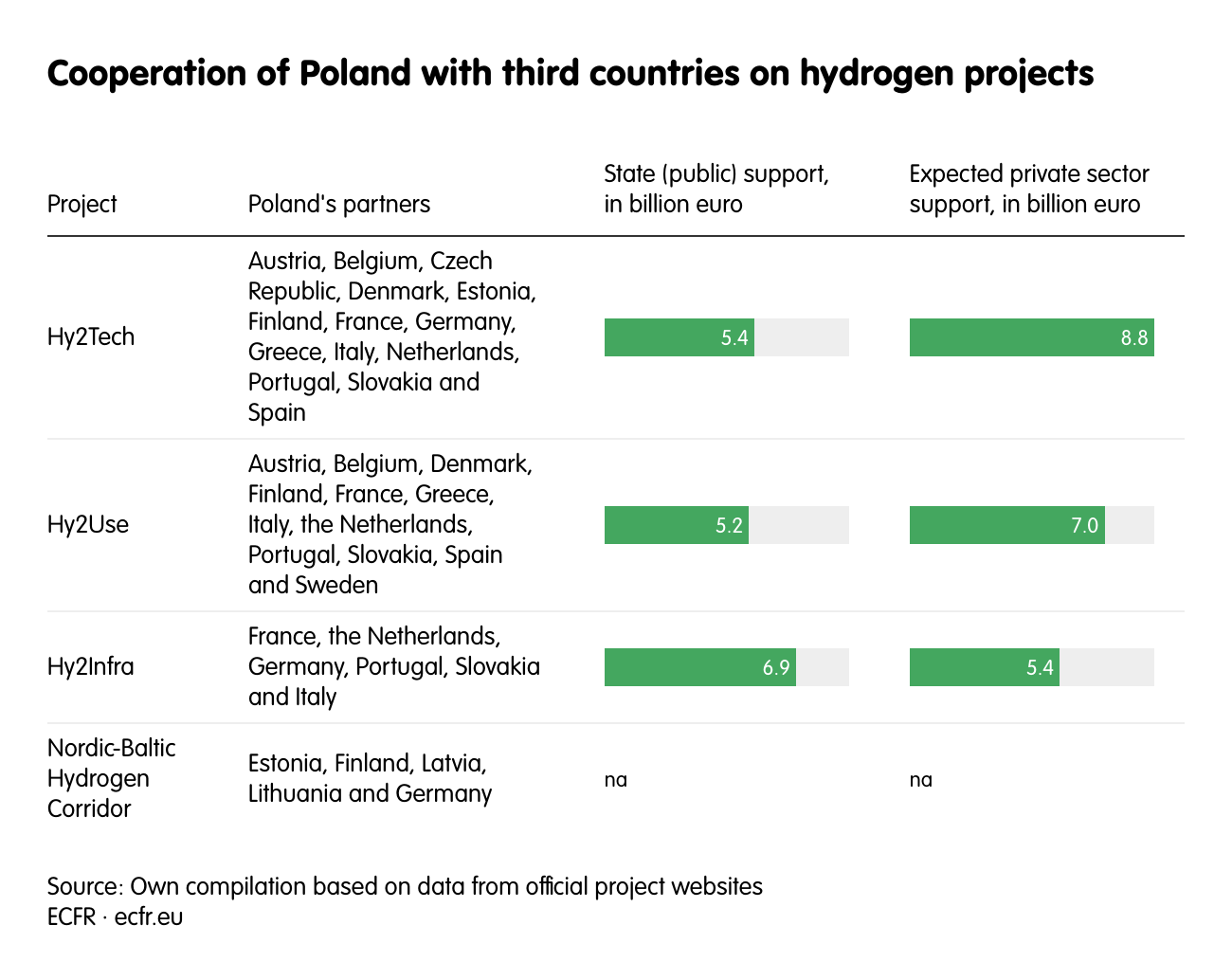

Additionally, Poland has been actively engaged in several hydrogen projects in collaboration with a dozen other EU countries that have received the status of Important Projects of Common European Interest (IPCEI): Hy2Tech, Hy2Use, and Hy2Infra. The first, approved by the European Commission in July 2022, focuses on the development of end-user hydrogen technologies. The IPCEI Hy2Use project focuses on hydrogen applications in the industrial sector. The Hy2Infra project involves investments in infrastructure, which are outside the scope of the first two IPCEI projects. Several IPCEI Hy2Infra projects are expected to be completed in the coming years. The commissioning of the large-scale electrolysers is planned for 2026-2028 and the pipelines for 2027-2029.

Financial support from the EU and international institutions is crucial for advancing energy projects in Poland. Key contributors include the European Bank for Reconstruction and Development (EBRD) and the European Investment Bank (EIB), which focus on financing initiatives for the energy transition.

In September 2024, the European Commission approved a €1.2 billion state aid programme to support investments in strategic sectors, aiding Poland’s transition to net-zero emissions. In October 2023, another €1.2 billion was approved specifically for Polish industrial and mining companies. Additionally, Poland received €244.2 million from the EU Modernisation Fund in 2022 to enhance energy efficiency. According to figures provided by the Ministry of Climate and Environment, Poland can use as much as PLN 539 billion (around €125 billion) from various EU funds to invest in the energy transition until 2027.

In 2023, Poland was the top recipient of EBRD financing within the EU, receiving a record €1.3 billion that contributed to a total of €13.9 billion over 500 projects since 1991. Notably, 75% of the 2023 funds were allocated to green investments aimed at decarbonisation and the energy transition. Key projects funded include PL-SUN’s plans for 16 photovoltaic power plants and initiatives by Baltic Sea Polska II and C&C Wind, both subsidiaries of Eurowatt Green Energy Group. Additionally, the EBRD invested PLN 240 million (approximately €55.8 million) in a local bond issued by Tauron for its decarbonisation strategy and provided a €140 million loan to Baltic Power for an offshore wind project. R.Power, a major photovoltaic farm developer, also received EBRD support.

The European Investment Bank (EIB) reaffirmed its commitment to Poland by providing nearly €5.1 billion in funding in 2023, comprised of €4.67 billion from the EIB and €632 million from the European Investment Fund (EIF). Financing for energy transition projects surged by 80% to €1.78 billion, with green financing rising to 52% of total funding, up from 49% in 2022. In December 2023, the EIB, alongside NordLB, signed an agreement to fund renewable energy projects across the EU, focusing on Poland, Denmark, and Sweden. Additionally, the EIB committed to financing the modernisation of the ENEA electricity distribution network in western Poland.

While Poland is actively enhancing cooperation with key foreign partners, there remain opportunities to strengthen its external energy policy, further supporting the ambitious goals of its energy transition initiatives.

Poland has made notable infrastructure investments in recent years, but finalising the remaining projects would help integrate energy markets in Europe. One such project is the Stork II gas interconnector with the Czech Republic, which faces uncertainty despite a July 2023 declaration from Czech authorities.

Finalising this interconnector would enhance Poland’s gas transmission capacity and strengthen energy security for both Poland and its neighbours. Additionally, Poland should continue developing electricity connections with Lithuania, particularly through the Harmony Link project, and work to synchronise the Baltic States’ power grids with the EU to facilitate electricity transmission.

Improving gas connections with Ukraine could also create new opportunities for energy cooperation and improve energy security in the central and eastern European regions. Integrated gas and electricity networks will bolster the resilience of Poland’s energy system against external disruptions, especially for importing clean energy from Ukrainian sources.

Finally, Poland should intensify collaboration with countries like the Netherlands and Spain, which have significant potential for energy storage development.

As Poland expands its energy infrastructure, it is crucial to avoid investments that could result in ‘stranded assets.’ A prime example is the proposed second floating LNG terminal in Gdansk, which was planned to have a capacity of 4.5 bcm per year. However, an open-season procedure conducted in 2023 revealed insufficient interest from foreign partners, indicating that the investment may be economically unjustifiable. In such cases, Poland should prioritise projects with established profitability and genuine market demand to mitigate the risk of financial wastage.

A key component of Poland’s energy strategy is the advancement of nuclear energy projects. Currently, collaboration with the US dominates the plans for nuclear power plants. However, to enhance the efficiency and flexibility of these initiatives, Poland should diversify its partnerships by engaging with other countries such as France and South Korea. France offers extensive experience in the construction and operation of nuclear power plants, while South Korea could be instrumental in developing small modular reactor (SMR) technology, which may significantly contribute to Poland’s energy mix.

By diversifying its partners, Poland can reduce dependency on a single technology provider and access new financing opportunities and innovative solutions. Such collaboration will also enhance project competitiveness, potentially leading to improved cost-effectiveness and efficiency.

Poland is navigating the challenge of transitioning away from coal as the primary energy source. Strengthening cooperation with countries facing similar challenges, like Germany or the Czech Republic, can yield significant benefits, particularly in sharing experiences and technologies to accelerate the shift to renewable energy sources. Collaborative efforts could focus on developing carbon capture and storage technologies, modernising power grids, and advancing hydrogen projects. To optimise costs and avoid repeating past mistakes, Poland should actively coordinate with other nations facing similar challenges during this energy transition.

One of the primary obstacles to the development of renewable energy sources in Poland is the lengthy administrative procedures. Streamlining the permitting processes for the wind industry is essential to meet the ambitious target of increasing wind power capacity in the Baltic Sea from 3 GW to 20 GW in the coming years, as committed by Poland and other Baltic countries. Accelerating administrative processes can significantly expedite project implementation and attract foreign investors to engage in further RES initiatives in Poland. Additionally, appointing a special government plenipotentiary for offshore wind could provide crucial support to the industry and facilitate more efficient investment.

Hydrogen is becoming increasingly vital in global decarbonisation efforts, and Poland should capitalise on the opportunities available in this sector. While actively participating in various EU multilateral projects, Poland should also strengthen bilateral cooperation with key partners.

Germany, for instance, is already collaborating with Polenergia on advanced hydrogen technologies, making it a valuable ally. Furthermore, Poland has signed a Memorandum of Cooperation on Hydrogen with Japan, which presents new opportunities for producing and distributing renewable hydrogen.

Advancing hydrogen technology can significantly contribute to industrial decarbonisation, create new jobs, and enhance the competitiveness of the Polish economy on the global stage.

Poland should prioritise increasing domestic production of renewable energy source components, such as wind turbines and photovoltaic panels. Currently, heavy reliance on imports, primarily from China and India, poses risks related to supply chain disruptions. Boosting domestic production would not only enhance energy independence but also create new jobs in the sector.

To minimise supply risks, Poland should collaborate with a range of technology suppliers to diversify sources of RES components, particularly considering ongoing global supply chain challenges. Poland should also support and actively engage in EU or multilateral initiatives with other EU countries to jointly source critical raw materials important for advancing the energy transition. Additionally, the financial stability of major wind energy players, such as Siemens Energy, which is facing difficulties due to technical issues with its turbines, should be monitored closely. Ensuring a reliable supply and maintaining the quality of renewable energy technology are crucial for Poland’s energy transition.

The development of electromobility in Poland is essential for the decarbonisation of transport and should be a priority. While the electric vehicle market in Poland is still relatively small, it is experiencing rapid growth; by September 2024, nearly 67,000 electric cars and almost 62,000 hybrids had been registered, reflecting increasing interest in this sector. Concurrently, the charging infrastructure is expanding, with the number of public charging points rising from 6,000 in December 2023 to nearly 8,000 by September 2024.

To support this momentum, Poland should enhance financial assistance for electric vehicle manufacturers and further develop the charging infrastructure. Collaborations with foreign partners like Greenway and Eesti Energia have started to yield benefits in expanding the charging network, but additional investments are necessary to meet growing market demands. It is also important to focus on developing infrastructure and supporting domestic production, particularly initiatives currently underway by Stellantis in Tychy and Gliwice.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}