EV Market Monitor – April 2026

May 15, 2026

The electric vehicle market softened in April following March’s rebound, with performance diverging between the new and used segments. New EV sales declined amid broader weakness in overall vehicle demand, even as elevated fuel prices renewed consumer focus on efficiency. Used EV sales, meanwhile, continued to expand, supported by improving inventory availability and a growing pool of off-lease vehicles.

Recent Cox Automotive research indicates that while higher gas prices are driving increased interest in fuel-efficient vehicles, most shoppers continue to gravitate toward fuel-efficient gas vehicles and hybrids rather than EVs. For many consumers, the path of least resistance remains improved efficiency within familiar powertrains. Taken together, April’s results point to an EV market settling into a more normalized pace and one shaped increasingly by affordability, availability and disciplined inventory management across segments.

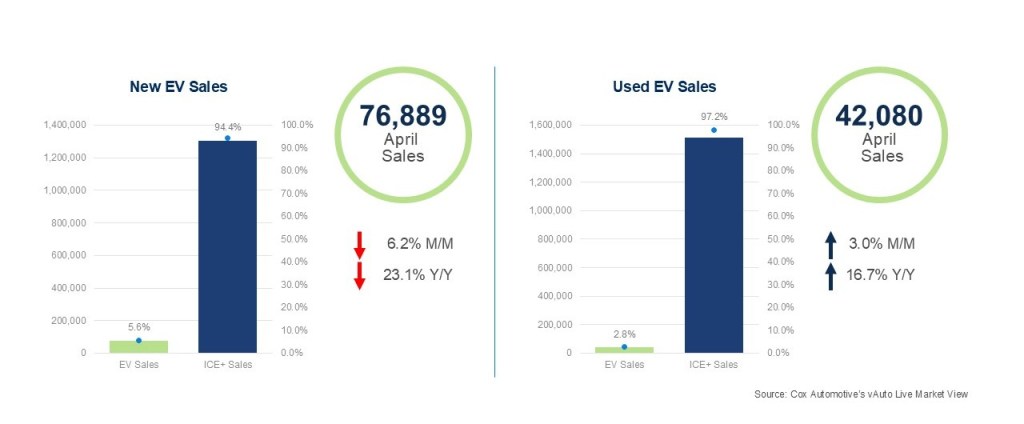

New EV Sales: New EV sales totaled an estimated 76,889 units in April, down 23.1% year over year and 6.2% month over month. EVs accounted for 5.6% of total new-vehicle sales, easing slightly from March as overall new-vehicle demand softened.

Tesla remained the market leader with 37,550 units sold, followed by Chevrolet, Hyundai, Ford and Cadillac. Tesla’s EV market share edged lower to 48.8%, down from March. Most automakers posted month-over-month declines, reflecting broader pullbacks among higher-volume brands. Ford was a notable exception, with EV sales rising 23.9% from March, alongside gains at several smaller-volume manufacturers, partially offsetting the broader market slowdown.

Used EV Sales: Used EV sales reached 42,080 units in April, up 16.7% year over year and 3% month over month, pushing used EV market share to a record 2.8%. Tesla again led with 16,174 units sold through non-Tesla dealers, followed by Hyundai, Chevrolet, Ford and BMW.

After March’s unusually strong surge, April reflected a more normalized pace of growth. Month-over-month gains were broad-based, with many brands posting increases, although declines among several higher-volume makes tempered the overall advance. Even so, the strong year-over-year gain underscores continued expansion in the used EV market as inventory improves and more vehicles age into the secondary market.

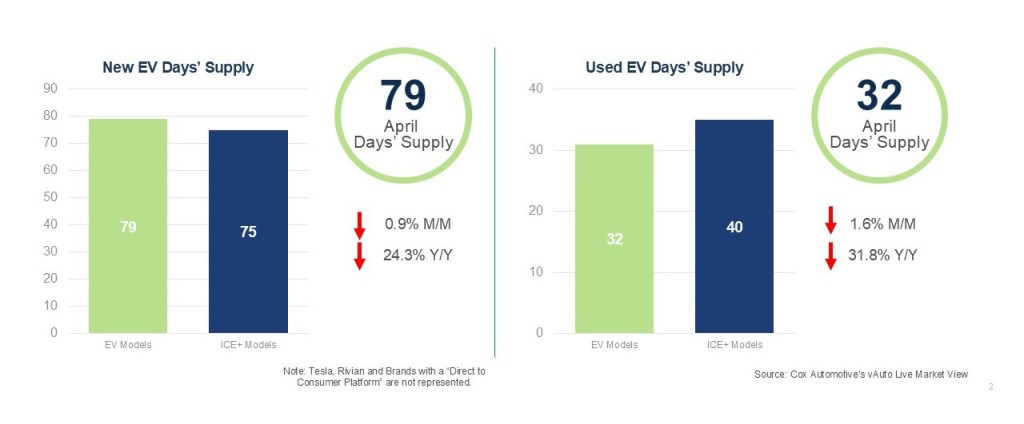

New EV Days’ Supply: Days’ supply edged lower to 79 in April, following a modest upward revision to March. Inventory remains more than 20% below year-earlier levels and near the lowest readings seen so far in 2026, suggesting continued tightening rather than renewed oversupply.

Inventory levels remain uneven by brand. Toyota, Hyundai, Mercedes-Benz and Subaru operated with relatively lean days’ supply in April, while Volkswagen, Nissan and GMC continued to carry elevated inventory positions. Several brands remain well below their mid-2025 peaks, reinforcing a gradual normalization in EV inventories even as variation across manufacturers persists.

Used EV Days’ Supply: Days’ supply fell to 32 in April, down modestly month over month and 31.8% below year-earlier levels. EV days’ supply remained below ICE+ for a second consecutive month. The gap underscores continued tightening in the used EV market and faster inventory turnover relative to the broader used-vehicle segment.

Days’ supply tightened broadly among high-volume brands, led by Chevrolet and Nissan. Tesla, Toyota and Rivian also remained relatively lean at around 28 to 29 days’ supply, reinforcing strong turnover across the used EV market.

Note: Tesla and Rivian figures reflect only vehicles available through traditional dealerships and exclude vehicles at factory-owned outlets.

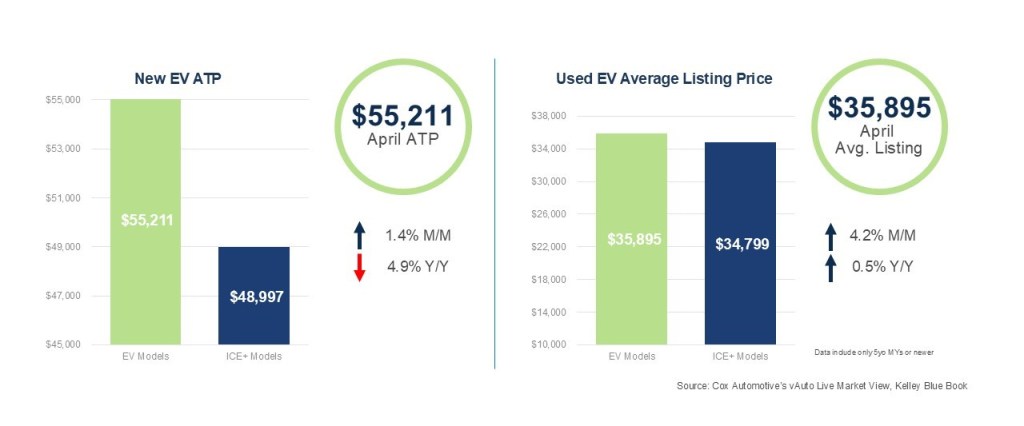

New EV ATP: The average transaction price for a new EV in April was $55,211, up 1.4% month over month but down 4.9% year over year. Incentives edged lower to an average of $7,640, representing 13.8% of ATP.

The month-over-month increase primarily reflected a mix shift rather than broad-based price gains. Volume improved for several higher-priced models, while declines among lower-priced, higher-volume brands, such as Chevrolet and Toyota, shifted the overall mix higher.

Even with Tesla accounting for nearly half of total EV sales and transacting below the industry ATP, stronger sales of higher-priced models lifted the overall average. As a result, the EV price premium over ICE+ vehicles widened modestly in April to approximately $6,214, up from roughly $5,800 in March. Read the April Kelley Blue Book ATP report.

Used EV Listing Price: The average listing price for a used EV was $35,895 in April, up 4.2% month over month and essentially flat year over year, at +0.5%. It was the first positive year-over-year reading since July 2025. The month’s increase was broad-based, with 29 makes posting higher listing prices, including several high-volume brands such as Tesla, up 6.0%; Chevrolet, up 7.7%; Hyundai, up 4.4%; and Ford, up 3.9%. The used EV price premium over ICE+ vehicles widened slightly to $1,096 in April, as both segments posted similar month-over-month gains.

Looking Ahead

Following March’s rebound, April’s results signal a return to a more measured pace across the EV market. Near-term volatility is likely to persist for new EVs as demand responds to broader softness in the new-vehicle market, evolving incentive strategies, uneven inventory positions and continued sensitivity to fuel prices. Tightening days’ supply suggests oversupply pressures continue to ease.

The used EV market remains comparatively well positioned. Improving availability, expanding model-year coverage and faster inventory turnover continue to support steady growth, even as month-to-month performance varies among higher-volume brands. The used EV market is expected to remain a relative bright spot through the remainder of the year.

View Historical EV Market Monitor reports.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}