Forget Intel: This Fast‑Moving CPU and GPU Innovator Is the Higher‑Upside Bet for Long‑Ter

January 29, 2026

Intel still needs time to capitalize on the AI chip market’s growth, but its rival is already making solid progress in this space.

Intel (INTC 0.26%) has been one of the hottest stocks in the semiconductor space in the past six months. The share price is up an incredible 137% during this period, due to the company’s turnaround efforts and investments by Nvidia, SoftBank, and the U.S. government, which have bolstered the company’s balance sheet.

However, Intel still has a lot of work to do before it can capitalize on the impressive growth opportunity in semiconductors. It wasn’t surprising, then, to see Intel’s stock crashing after releasing its latest quarterly report.

Let’s see why that was the case and take a closer look at another semiconductor stock that’s in a better position to make the most of the artificial intelligence (AI)-fueled growth in the semiconductor market.

Image source: AMD.

Intel’s turnaround is going to take time

Intel reported a 4% year-over-year drop in revenue in the fourth quarter of 2025. The company’s data center and AI (DCAI) segment, however, reported slightly stronger year-over-year growth of 9%. Intel management pointed out on the latest earnings call that its DCAI revenue “would have been meaningfully higher if we had more supply.”

Today’s Change

(-0.26%) $-0.13

Current Price

$48.66

Management estimates that Intel’s supply situation will start improving in the next quarter and continue to improve as the year progresses. As a result, there’s a good chance the stock regains its momentum later in 2026, especially due to the healthy demand for its AI-focused offerings.

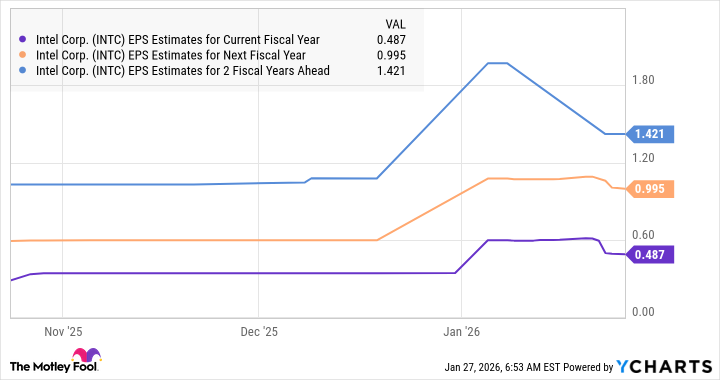

However, for a stock that’s trading at an expensive 88 times earnings, Intel needed to deliver solid guidance to justify its valuation. This is where it failed.

Intel management called for break-even earnings per share in Q2, which will be lower than the year-ago period’s non-GAAP earnings of $0.13 per share, so it’s easy to see why investors were quick to press the panic button. Additionally, analysts lowered their earnings-growth expectations for the next three years.

Data by YCharts.

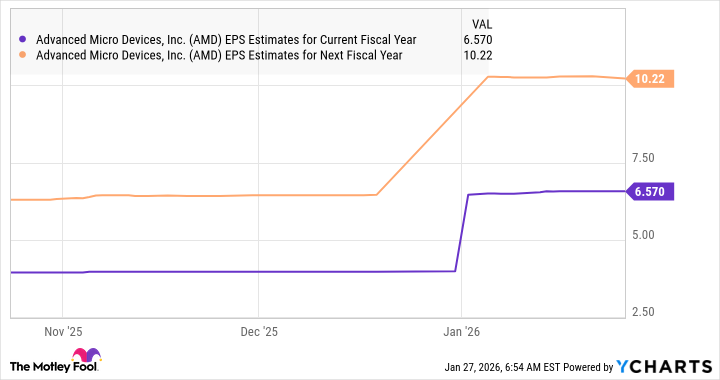

However, that’s not the case with Intel’s rival Advanced Micro Devices (AMD 0.24%). Analysts covering AMD are raising their earnings expectations for the company, which isn’t surprising as it’s poised to capitalize on the growing demand for both data center graphics cards and server-oriented central processing units (CPUs). Let’s see why AMD is likely to deliver bigger gains to investors than Intel in the long run.

AMD is on track to deliver remarkable earnings growth

AMD and Intel serve the same markets — personal computers (PCs) and data centers — with their chips. Both companies make CPUs and graphics processing units (GPUs), which is why you may be surprised to see the stark difference in their financial performance.

While Intel is finding it difficult to grow, AMD is on track to deliver a 32% increase in revenue for 2025. What’s more, analysts expect earnings growth to accelerate in 2026, following a 20% increase last year to $3.97 per share.

Data by YCharts.

It’s easy to see why analysts are bullish about AMD’s prospects. The company has been pushing the envelope on the technology front in both CPUs and GPUs.

AMD’s MI400 data center GPU, which is set to be launched this year, will have almost double the computing power of the previous generation MI350 processor. AMD believes that this processor could help it compete against Nvidia’s next-generation Vera Rubin cards. Even better, AMD points out that the MI500 data center GPU lined up for next year will deliver a massive 1,000x increase in AI performance over the previous-generation MI300 chips.

On the other hand, AMD’s server CPUs are also gaining traction among customers due to their ability to process AI workloads. Its share of server CPUs increased by 3.5 percentage points year over year in the third quarter of 2025 to 27.8%.

AMD estimates that it could capture more than half of the server CPU market in the long run. It’s worth noting that the demand for AI applications will accelerate the growth of the server CPU market. AMD predicts that the server CPU market could generate more than $60 billion in revenue in 2030, up from $26 billion last year, clocking an annual growth rate of 18% through the end of the decade.

If AMD captures half of this market, driven by the deployment of its Epyc server processors by large hyperscalers and AI companies, its server CPU revenue could hit $30 billion by the end of the decade. Given that AMD is estimated to have generated $34 billion in revenue last year, the server CPU business alone could move the needle in a big way for the company.

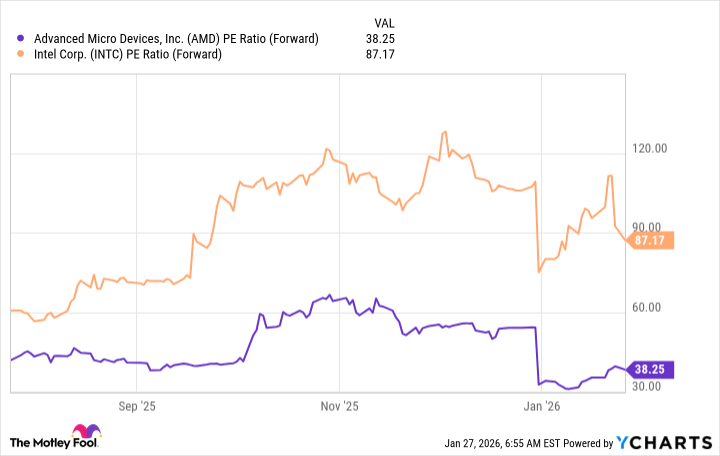

Another reason why it would be a good idea to buy AMD stock over Intel right now is the valuation. This is evident from the following chart.

Data by YCharts.

The market could reward AMD’s accelerating earnings growth with a premium valuation in the future. That may not be the case with Intel, considering its expensive multiple and poor growth. As such, buying AMD stock over Intel looks like the right thing to do as the former’s market-share gains and product-development moves could lead to impressive stock-price upside in the long run.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}