Green Energy Market

June 5, 2025

Quick Navigation

Report Overview

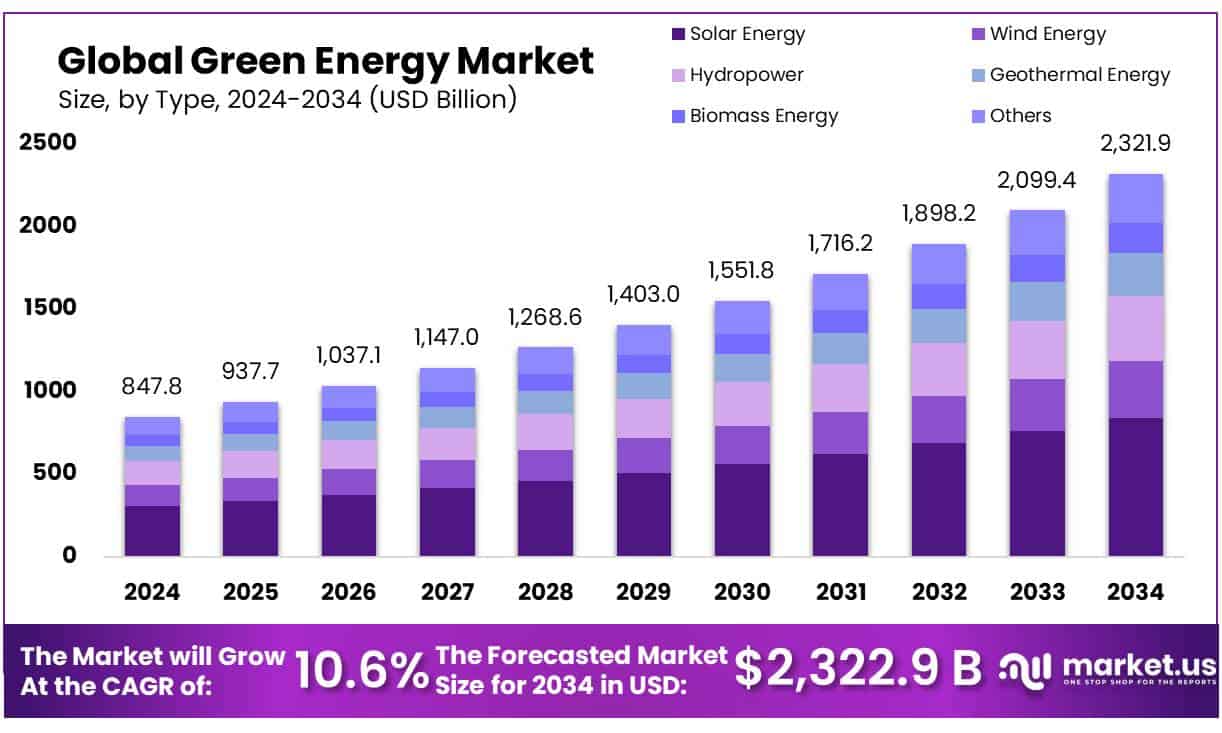

The Global Green Energy Market size is expected to be worth around USD 2321.9 Billion by 2034, from USD 847.8 Billion in 2024, growing at a CAGR of 10.6% during the forecast period from 2025 to 2034.

The Green Energy Cellulose Concentrates industry is emerging at the intersection of sustainable energy and advanced materials, leveraging cellulose—a renewable, biodegradable polymer derived from plant biomass—as a key component in various applications. This sector encompasses the utilization of cellulose in energy storage systems, biofuels, and as functional additives in food and industrial products, aligning with global efforts to transition toward a circular economy.

Driving factors for the growth of this sector include the global push for decarbonization and the transition to sustainable energy sources. Renewable energy consumption in the power, heat, and transport sectors is expected to increase by nearly 60% from 2024 to 2030, boosting the share of renewables in final energy consumption to nearly 20% by 2030, up from 13% in 2023. Cellulose-based biofuels are particularly significant in sectors that are challenging to electrify, such as aviation and marine transport.

Government initiatives play a crucial role in the advancement of GECC. For instance, in the United States, the Department of Energy’s 2023 Billion-Ton Report outlines the potential of biomass, including cellulose, to meet a significant portion of the nation’s energy needs. The report emphasizes the importance of sustainable biomass production and its integration into the energy sector.

In the realm of renewable energy, cellulose-based biofuels are gaining traction. The International Energy Agency (IEA) reports that renewable fuels, including those derived from cellulose, account for nearly 15% of the forecast growth in renewable energy demand from 2024 to 2030. These fuels are particularly expanding in sectors that are challenging to electrify, such as aviation and marine transport.

Key Takeaways

- Green Energy Market size is expected to be worth around USD 2321.9 Billion by 2034, from USD 847.8 Billion in 2024, growing at a CAGR of 10.6%.

- Solar Energy held a dominant market position, capturing more than a 36.2% share of the global green energy market.

- Electricity Generation held a dominant market position, capturing more than a 68.4% share of the green energy market.

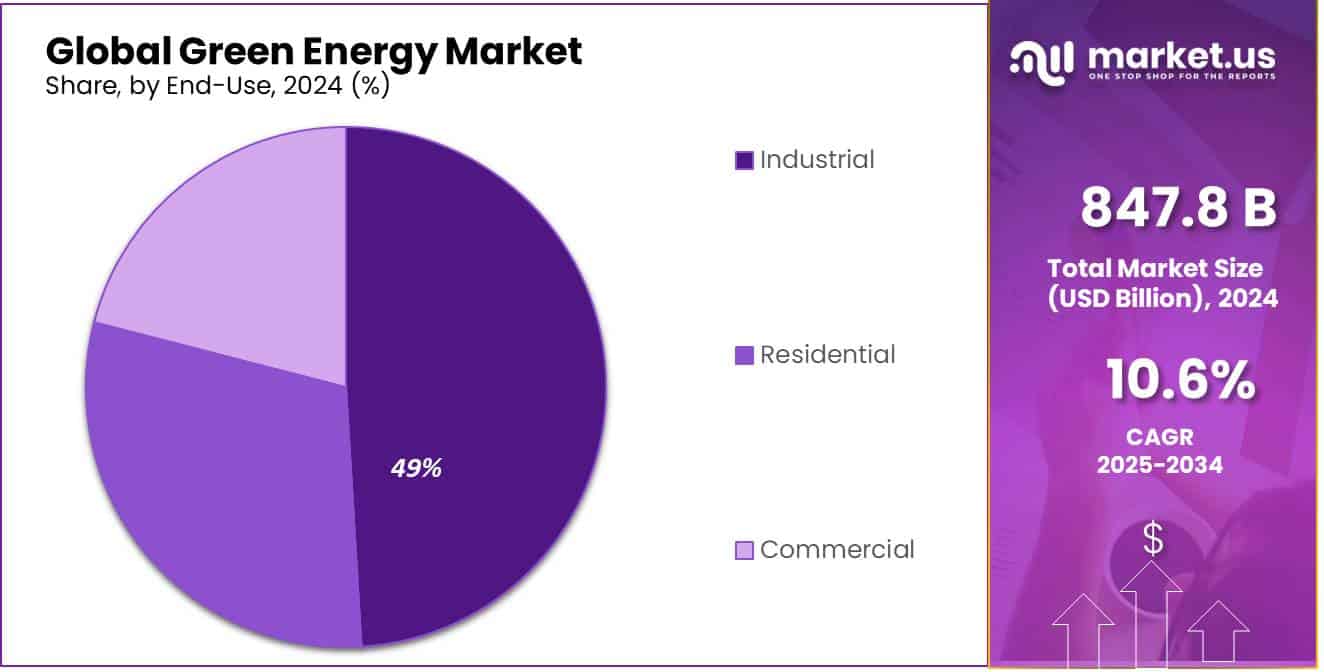

- Industrial sector held a dominant market position, capturing more than a 49.1% share.

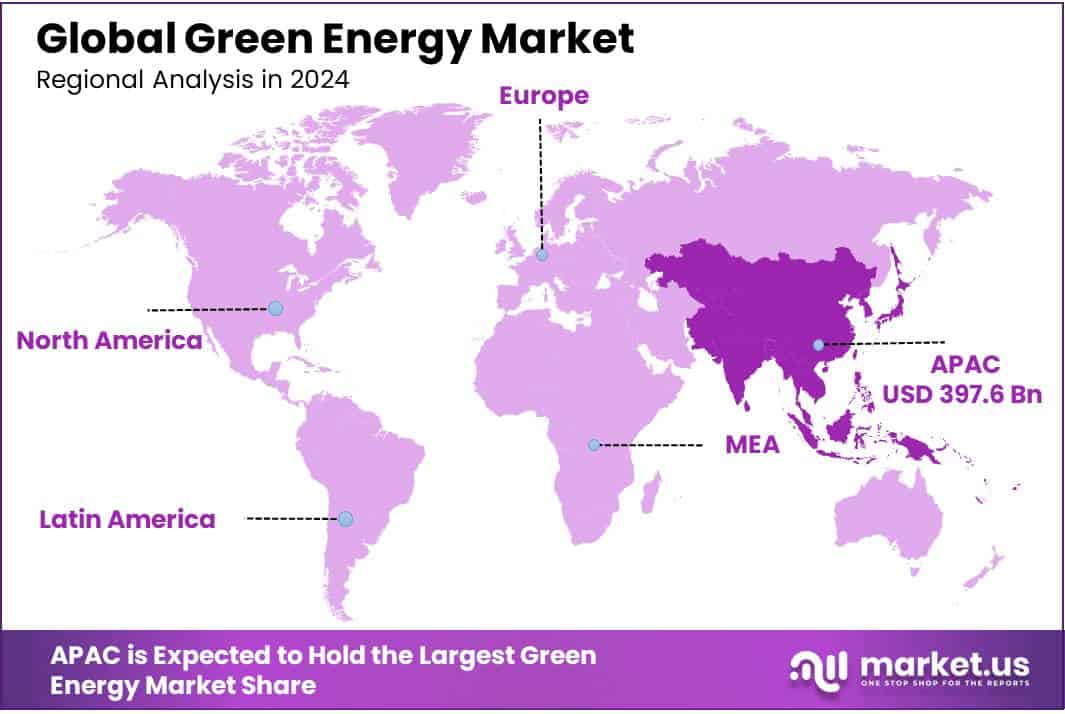

- Asia-Pacific (APAC) region emerged as the dominant force in the global green energy market, securing a substantial 46.9% share, equivalent to USD 397.6 billion.

By Source

Solar Energy leads Green Energy Sources with 36.2% market share in 2024 due to its scalability and falling installation costs.

In 2024, Solar Energy held a dominant market position, capturing more than a 36.2% share of the global green energy market. This strong foothold was primarily due to declining photovoltaic module costs, government-backed solar incentive schemes, and improved panel efficiency. Countries like India, China, and the U.S. aggressively expanded their solar capacity, responding to both energy demand and climate goals. By 2025, solar adoption is expected to increase steadily as grid parity becomes more achievable across emerging markets, reinforcing solar’s leadership among renewable sources.

By Application

Electricity Generation dominates Green Energy Applications with 68.4% share in 2024 driven by rising global energy demand.

In 2024, Electricity Generation held a dominant market position, capturing more than a 68.4% share of the green energy market. This growth was mainly fueled by global efforts to replace fossil fuels with cleaner power sources like solar, wind, and hydroelectric energy. As countries pushed for decarbonization, utility-scale renewable power projects became central to national energy strategies. By 2025, the segment is expected to remain the largest contributor, as investments in grid modernization and clean power infrastructure continue to grow, especially across Asia-Pacific and Europe.

By End Use

Industrial Sector leads Green Energy End Use with 49.1% share in 2024 due to rising shift from fossil fuels.

In 2024, the Industrial sector held a dominant market position, capturing more than a 49.1% share in the overall green energy end-use segment. The growing emphasis on reducing carbon emissions and improving operational energy efficiency has driven large-scale industries to adopt renewable sources such as biomass, solar thermal, and wind power. Heavy manufacturing, cement, and chemical industries especially led the transition, integrating green energy into both process heat and power requirements. This momentum is expected to continue through 2025, supported by stricter emission norms and corporate sustainability targets worldwide.

Key Market Segments

By Source

- Solar Energy

- Wind Energy

- Hydropower

- Geothermal Energy

- Biomass Energy

- Others

By Application

- Electricity Generation

- Heating

- Transportation

- Industrial Processes

By End Use

- Industrial

- Residential

- Commercial

Drivers

Government Initiatives Fueling India’s Green Energy Market

One of the major driving factors for the green energy market in India is the government’s proactive approach through comprehensive policies and substantial investments. These initiatives have significantly accelerated the adoption of renewable energy across the country.

In the fiscal year 2024–25, India achieved a record addition of 30 gigawatts (GW) of clean energy capacity, sufficient to power approximately 18 million homes. This milestone reflects a substantial shift from coal, which previously accounted for 60% of India’s power capacity but has now declined to under 50%. The government’s commitment is further evident in its ambitious target of reaching 500 GW of non-fossil fuel energy capacity by 2030, with nearly 170 GW of renewable energy projects currently in the pipeline.

Financially, the Indian government has raised approximately ₹57,697 crore through sovereign green bonds between FY 2022–23 and FY 2024–25. About 21% of these funds have been allocated to renewable energy projects, underscoring the financial commitment to green energy development.

At the state level, initiatives like the Pradhan Mantri Surya Ghar Muft Bijli Yojana aim to install rooftop solar panels in 1 crore households, providing 300 units of free electricity monthly. This program, with an investment of over ₹75,000 crore, includes subsidies up to ₹78,000 for eligible households. Additionally, Andhra Pradesh has set a target of installing 3 lakh rooftop solar connections by the end of June 2025, contributing to the broader goal of 20 lakh installations by the end of 2025.

Restraints

Regulatory and Infrastructure Challenges Hindering India’s Green Energy Progress

One of the significant challenges facing India’s green energy sector is the complex regulatory environment and inadequate infrastructure, which impede the swift implementation of renewable energy projects. Despite the government’s ambitious target of achieving 500 GW of non-fossil fuel capacity by 2030, several systemic issues have slowed progress.

In 2024, India issued a record 73 GW of utility-scale renewable energy tenders. However, about 8.5 GW of these tenders were undersubscribed, a fivefold increase compared to 2023. This shortfall is attributed to complex tender structures and delays in interstate transmission readiness. Furthermore, approximately 38.3 GW of capacity was canceled between 2020 and 2024 due to issues such as tender design flaws, location or technical challenges, and delays in signing power supply agreements.

Financial constraints also pose a significant barrier. In 2024, India attracted just over $13 billion in green energy investments, falling short of the $68 billion needed annually to meet its 2030 targets. This investment gap is exacerbated by project commissioning delays, land acquisition challenges, and regulatory hurdles, which collectively deter investor confidence.

Additionally, the lack of adequate grid infrastructure hampers the integration of renewable energy into the national grid. Despite adding 30 GW of clean energy capacity in the fiscal year ending April 2025, renewables supplied only 24% of electricity in 2024. This limited contribution is primarily due to integration and grid challenges, highlighting the need for substantial infrastructure development to support the growing renewable energy capacity.

Opportunity

Green Hydrogen: A Promising Avenue for India’s Renewable Energy Expansion

India is making significant strides in the renewable energy sector, and one of the most promising growth opportunities lies in the development of green hydrogen. Recognizing its potential, the Indian government has launched the National Green Hydrogen Mission with a substantial investment of ₹19,744 crore. The mission aims to produce 5 million metric tonnes of green hydrogen annually by 2030, which necessitates the addition of approximately 125 GW of renewable energy capacity dedicated to hydrogen production.

This initiative is not just about energy production; it’s about transforming India’s energy landscape. Green hydrogen offers a clean alternative to fossil fuels, especially in hard-to-abate sectors like steel manufacturing, refining, and heavy transportation. By integrating green hydrogen into these industries, India can significantly reduce its carbon emissions and move closer to its net-zero targets.

The private sector is actively participating in this green revolution. For instance, Bharat Petroleum Corporation Limited (BPCL) has entered into a joint venture with Singapore-based Sembcorp to develop green hydrogen and renewable energy projects across India. This collaboration aims to explore initiatives in green ammonia production, port emissions reduction, and other green fuel technologies.

Moreover, the government’s supportive policies and financial incentives are attracting significant investments. The Production Linked Incentive (PLI) scheme for electrolyzer manufacturing is expected to boost domestic production capabilities, reducing reliance on imports and fostering self-sufficiency in the green hydrogen sector.

Trends

Artificial Intelligence: Transforming India’s Renewable Energy Landscape

One of the most significant trends shaping India’s green energy sector is the integration of Artificial Intelligence (AI) to enhance efficiency and reliability. AI technologies are being increasingly adopted to optimize energy production, forecast demand, and manage grid operations, thereby accelerating the country’s transition to renewable energy.

AI-driven optimization plays a crucial role in integrating renewable energy sources by improving forecasting accuracy by up to 30%. This enhancement enables better planning of energy production schedules, reducing overall costs by 15% and contributing to a stable grid that allows seamless integration of solar and wind energy.

The Indian government has recognized the potential of AI in the energy sector and has introduced several initiatives to promote its adoption. The IndiaAI Mission, approved in 2024, allocated ₹10,300 crore over five years to strengthen AI capabilities, including the development of a high-end common computing facility equipped with 18,693 Graphics Processing Units (GPUs).

Moreover, state governments are also embracing AI to drive innovation in the energy sector. For instance, the Odisha state cabinet approved the Artificial Intelligence (AI) Policy-2025, which includes the ‘Odisha AI Mission’ aimed at implementing AI across different sectors, including energy sustainability.

Regional Analysis

Asia-Pacific Leads Global Green Energy Market with 46.9% Share, Valued at USD 397.6 Billion in 2024

In 2024, the Asia-Pacific (APAC) region emerged as the dominant force in the global green energy market, securing a substantial 46.9% share, equivalent to USD 397.6 billion. This leadership is driven by rapid industrialization, escalating energy demands, and robust governmental support for renewable energy initiatives across key economies such as China, India, Japan, and Australia.

China continues to be at the forefront, contributing approximately two-thirds of Asia’s renewable capacity. In 2024, China added a record 292 GW of solar capacity, up from 257 GW in 2023, reinforcing its position as a global leader in solar energy deployment. India has also made significant strides, tripling its renewable energy capacity over the past decade to reach 232 GW by May 2025, with an ambitious target of 500 GW by 2030.

Australia is experiencing a surge in renewable energy investments, particularly in battery storage. In early 2025, the country committed $2.4 billion to battery storage projects, marking the second strongest quarter on record. Japan, aiming to increase its renewable energy share to 36-38% by 2030, is investing heavily in solar and wind energy projects.

The APAC region’s commitment to renewable energy is further evidenced by its record addition of 450,000 MW of new renewable capacity in 2024, surpassing Europe and North America combined . This growth trajectory is supported by favorable policies, technological advancements, and increasing investments in renewable infrastructure.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Iberdrola stands as a global leader in renewable energy, with a total installed capacity of 62,045 MW, of which 41,246 MW is renewable, as of 2023. In 2024, the company reported a 16.8% year-on-year increase in net profit to €5.612 billion, driven by record investments totaling nearly €17 billion. Notably, 70% of these investments were directed towards the US and UK markets, underscoring Iberdrola’s strategic focus on expanding its international renewable energy footprint.

RWE achieved strong earnings in 2024, with an adjusted EBITDA of €5.7 billion and adjusted net income of €2.3 billion. The company invested €10 billion in expanding its renewable energy portfolio, commissioning new projects with a total capacity of approximately 2 GW. Renewable sources accounted for over 40% of RWE’s electricity production, contributing to a 13% reduction in CO2 emissions compared to the previous year.

SolarEdge Technologies faced challenges in 2024, with total revenues declining to $901.5 million from $2.98 billion in the prior year. Despite this, the company maintained a significant presence in the solar inverter market, with over 3.7 million homes equipped with its PV systems by the end of 2024. Additionally, more than 50% of Fortune 100 companies have adopted SolarEdge technology, reflecting its continued influence in the sector.

Top Key Players in the Market

- Iberdrola

- RWE

- SolarEdge Technologies

- NextEra Energy

- China Longyuan Power Group

- Siemens Gamesa Renewable Energy

- China Three Gorges Corporation

- Orsted

- EDP Renewables

- GE Renewable Energy

- Canadian Solar

- First Solar

- Brookfield Renewable Partners

- Vestas Wind Systems

- Enel

Recent Developments

In 2024, Iberdrola solidified its leadership in the green energy sector by achieving a net profit of €5.612 billion, marking a 17% increase from the previous year.

In 2024, RWE significantly advanced its position in the green energy sector, reporting an adjusted EBITDA of €5.7 billion and an adjusted net income of €2.3 billion. The company invested €10 billion in expanding its renewable energy portfolio, commissioning approximately 2 GW of new capacity across offshore and onshore wind farms, solar plants, battery storage systems, and electrolysers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 847.8 Bn |

| Forecast Revenue (2034) | USD 2321.9 Bn |

| CAGR (2025-2034) | 10.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Solar Energy, Wind Energy, Hydropower, Geothermal Energy, Biomass Energy, Others), By Application (Electricity Generation, Heating, Transportation, Industrial Processes), By End Use ( Industrial, Residential, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Iberdrola, RWE, SolarEdge Technologies, NextEra Energy, China Longyuan Power Group, Siemens Gamesa Renewable Energy, China Three Gorges Corporation, Orsted, EDP Renewables, GE Renewable Energy, Canadian Solar, First Solar, Brookfield Renewable Partners, Vestas Wind Systems, Enel |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}