Hormuz Crisis Forces Rethink on Alternative Marine Fuels Investment

April 16, 2026

The escalation of conflict across the Middle East and the disruption to energy flows through the Strait of Hormuz have introduced a variable into the maritime energy transition that regulatory frameworks were never designed to handle: the possibility that conventional marine fuel becomes unavailable because competing domestic priorities absorb the available supply. This changes the analytical framing for clean shipping in a big way.

Until now, the investment case for alternative marine fuels has been driven by compliance – organized around the International Maritime Organization’s Net-Zero Framework, and the European Union’s FuelEU Maritime regulation and emissions trading system – with energy security treated as background context. The Hormuz crisis forces this to the front, opening an arguably more durable investment rationale for alternative fuels that does not depend on the survival of any regulatory regime.

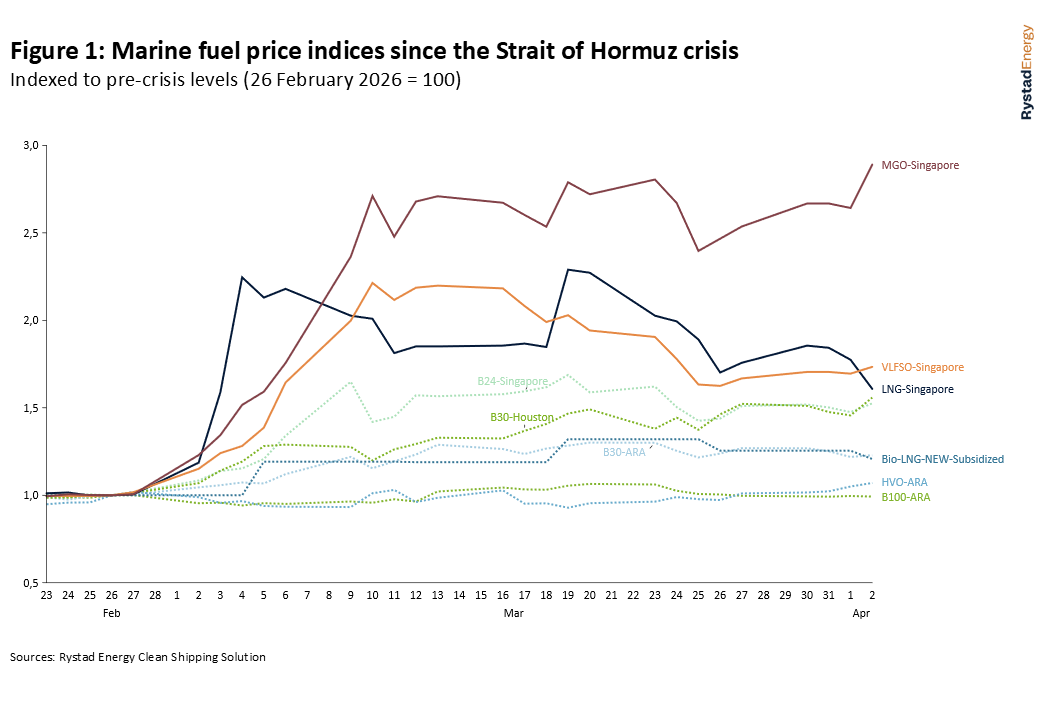

The near-term market impact has been sharp but uneven. Prices for Singapore very low sulfur fuel oil (VLSFO) and low-sulfur marine gas oil (LSMGO) surged in the days following the start of the crisis, driven by supply risk repricing rather than confirmed physical shortages. Rystad Energy’s forecast projects the spike to peak around April to May this year, with LSMGO reaching well above $1,200 per tonne before gradually declining. Normalization is not expected until the middle of next year. However, even without triggering a structural shift in fuel choice, the price dislocation has made a deeper concern more visible: the reliability of conventional bunker supply itself can no longer be assumed.

The crisis also arrives at a moment of deepening regulatory uncertainty. The extraordinary Marine Environment Protection Committee (MEPC) session, which is scheduled for October this year, faces growing opposition, with the US, some major oil producers and Japan all pushing to weaken or replace the NZF. The worst-case scenario for clean fuel investment is not the absence of regulation but ambiguous regulation: a framework adopted in sufficiently diluted form that it generates ongoing uncertainty without providing the carbon-cost clarity needed to drive capital allocation. This is the context in which energy security shifts from supplementary argument to structural substitute.

The crisis reshapes the investment case selectively across individual fuel pathways. Biodiesel faces intensifying feedstock competition from sustainable aviation fuel (SAF) mandates. Compliance economics of bio-liquefied natural gas (bio-LNG) remain attractive for operators with surplus unit (SU) market access, but fleet applicability is narrow and delivery infrastructure immature. Biomethanol’s case is strengthening, anchored by China’s scale and strategic incentive, though supply constraints remain binding. E-methanol shares methanol’s engine compatibility advantages but sits at significantly higher production costs and, without regulatory support to bridge the gap, near-term scaling remains constrained despite the crisis compressing the cost differential at some ports. Ethanol is credible as an energy-security fuel on routes outside EU regulatory jurisdiction but still limited to a small segment of vessels. Ammonia remains structurally behind, requiring simultaneous policy pull and infrastructure investment that energy-security motivation alone cannot yet deliver.

The historical record offers a useful corrective to near-term pessimism. Previous energy shocks have consistently produced lasting structural change rather than temporary price spikes. The Hormuz disruption is likely to follow the same pattern, with one important distinction: alternative fuel technology is already commercially available at meaningful scale. The crisis does not immediately solve infrastructure immaturity, but it creates the political mandate and investment capital to accelerate that build faster than the pre-crisis compliance pathway would have delivered.

For shipowners, energy security can no longer be a background consideration. Voyage planning, bunkering choices and fuel-sourcing decisions now carry supply reliability risk alongside compliance cost risk. No single alternative fuel offers a universal solution, and the right pathway remains highly specific to vessel type, trade route and commercial structure. Those who move early to secure diversified and resilient fuel supply chains will be better positioned to absorb future shocks and to capture the commercial advantage that fuel flexibility increasingly represents.

This article draws on insights from our latest Rystad Energy report, “Hormuz: Impact on clean shipping fuels“. The full analysis is available to clients via the Client Portal.

More Top Reads From Oilprice.com

- TotalEnergies Sees Q1 Profit Surge on High Prices, Strong Trading

- Fire at Domestic Refinery Worsens Australia’s Fuel Supply Crisis

- Iran Suspends Petrochemical Exports to Avoid Domestic Shortages

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}