How Caution and Contrarianism Paid Off for Investors During Q1

April 1, 2025

There are years when nothing happens, and quarters when years happen, to paraphrase Vladimir Lenin. The first quarter of 2025 was a doozy for investors. The Morningstar US Market Index entered correction territory at one point, unsettled by the DeepSeek AI disruption, major policy uncertainty around tariffs, and fears of “stagflation.” “Risk off” has been the dominant market vibe.

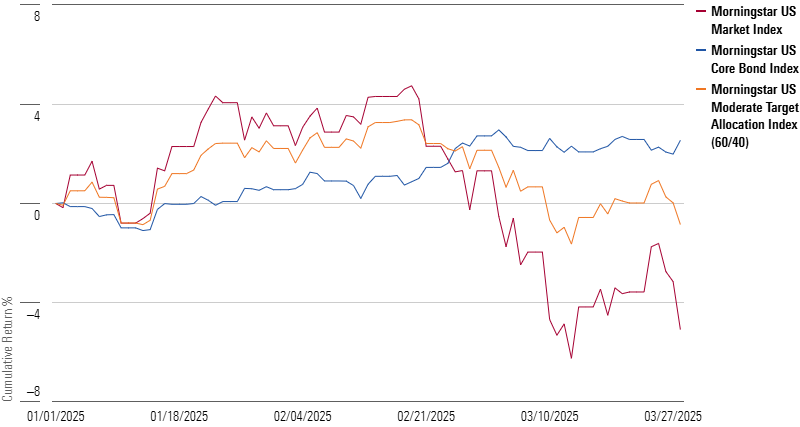

Two broad groupings of investors have fared best so far this year. First, those exposed to a variety of assets limited their losses from stock market selloffs. The Morningstar US Moderate Target Allocation Index, representing a diversified portfolio of roughly 60% stocks and 40% bonds, largely held its value even as stocks were plummeting. Diversification has often felt like a drag in recent years. But owning bonds, as well stocks of different styles and geographies, can pay off in difficult times.

Second, the first quarter has rewarded contrarian investors who pay attention to valuation. At the start of 2025, my colleagues on Morningstar’s research and investment side were sounding caution. “Markets Are Priced to Perfection, but Will It Last?” was the question posed by Morningstar Chief US Market Strategist Dave Sekera. Exuberance around artificial intelligence had fueled a powerful rally. Valuations, especially on the growth side of the US stock market, were looking stretched. In 3 Contrarian Investments for 2025, I highlighted neglected areas where Morningstar saw far more upside potential: international equity markets, US equity market segments beyond growth and technology, and bonds.

There’s no telling what the rest of 2025 has in store. It’s possible that the “rotation” will fade—as did shifts in market leadership in the third quarter of 2024 and 2022. Even if they do, the first quarter’s lessons around the benefits of diversification and the importance of valuation are worth bearing in mind as investors head into the second quarter.

Diversification Isn’t for Suckers After All

US growth stocks have been hot for so long that many investors have neglected other asset classes. Foreign stocks are often considered superfluous. The Morningstar US Market Index has roughly tripled the return of the Morningstar Global Markets ex-US Index in USD terms for the 10 years through 2024. Meanwhile, the growth half of the US stock market trounced the value half over that span. And the Morningstar US Core Bond Index produced an average annual gain of just 1.3% from 2014 through 2024. Many investor portfolios came into 2025 heavily tilted toward recent winners.

But the first quarter of 2025 served up a reminder that, every so often, financial markets convulse. Stocks are called “risk assets” for a reason. Whether caused by tariffs or just a change in sentiment, equity selloffs cause real pain for investors. In What We’ve Learned From 150 Years of Stock Market Crashes, my colleague Emelia Fredlick refreshes a long-running Morningstar study looking at monthly US stock market returns going back to 1886. Putting the first quarter of 2025’s crash in context, Fredlick offers two takeaways. First, “it’s impossible to predict how long a stock market recovery will take” and second, “If you don’t panic and sell your stock holdings when the market crashes, you will be rewarded in the long run.”

Not every investor has a decades-long time horizon, though. My colleague Jeffrey Ptak recently addressed “sequence-of-returns risk‚” concluding that retirees who avoid losses in the early years of their retirement are less likely to outlive their savings. Portfolios heavy on stocks are most susceptible to the kind of losses from which it’s difficult to recover. There’s a reason that bonds are referred to as “ballast,” steadying a portfolio in stormy waters.

High-quality bonds sure provided diversification benefits in 2025’s first quarter. The Morningstar US Core Bond Index, heavy on Treasuries, as well as investment-grade corporate and agency debt, appreciated in value as stocks were falling in February and March. It was partly a flight to safety. Investors may also be anticipating recession and interest-rate cuts.

Whatever the reasons, it’s not the first time bonds have provided safe haven. As recently as the third quarter of 2024, the Morningstar US Core Bond Index rose as stocks fell. In fact, the bond index was in positive territory during three of four equity bear markets this century. The great exception was 2022, when inflation and rapidly rising interest rates undermined both stocks and bonds.

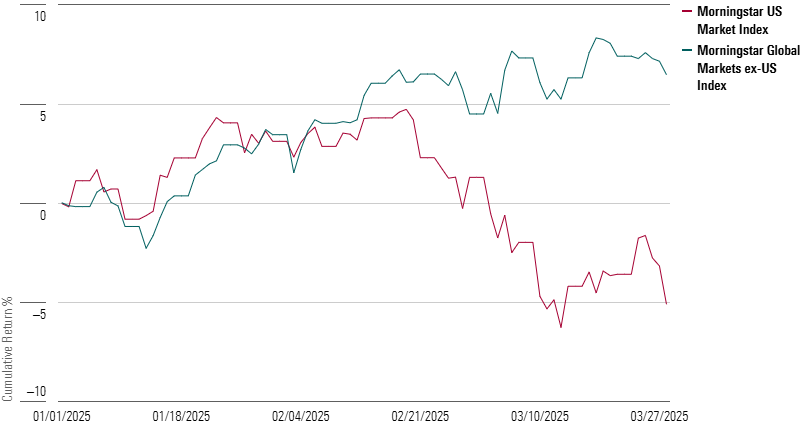

Time will tell whether the first quarter of 2025 is a minor blip or a more lasting inflection point. Regardless, it has provided a reminder that market leadership is changeable. Not only did bonds outperform stocks, but the tables turned within equities. The Morningstar Global Markets ex-US Index was well ahead of its US counterpart, as seen below. European equities rallied on hopes the continent is emerging from its economic and political malaise. The Chinese market performed exceptionally well, boosted partly by the DeepSeek AI effect. Brazil’s stock market, a horrendous performer in 2024, has also posted strong returns so far this year.

Within the US stock market, the pain of 2025’s downturn has been disproportionally felt on the growth side of the market, especially companies tied to the AI theme. Members of the “Magnificent Seven” like Nvidia NVDA, Microsoft MSFT, and Alphabet GOOG are all down this year. So is semiconductor maker Broadcom AVGO. While Tesla TSLA has shed roughly one third of its value, partly on fears that CEO Elon Musk’s political activity will undermine demand, it’s unclear why tariffs, the proximate trigger for the equity market selloff, would impact AI-linked companies more than other parts of the market. It could just be a case of the highest flyers having further to fall.

Buying the Unloved Has Worked in 2025—but Not Everywhere

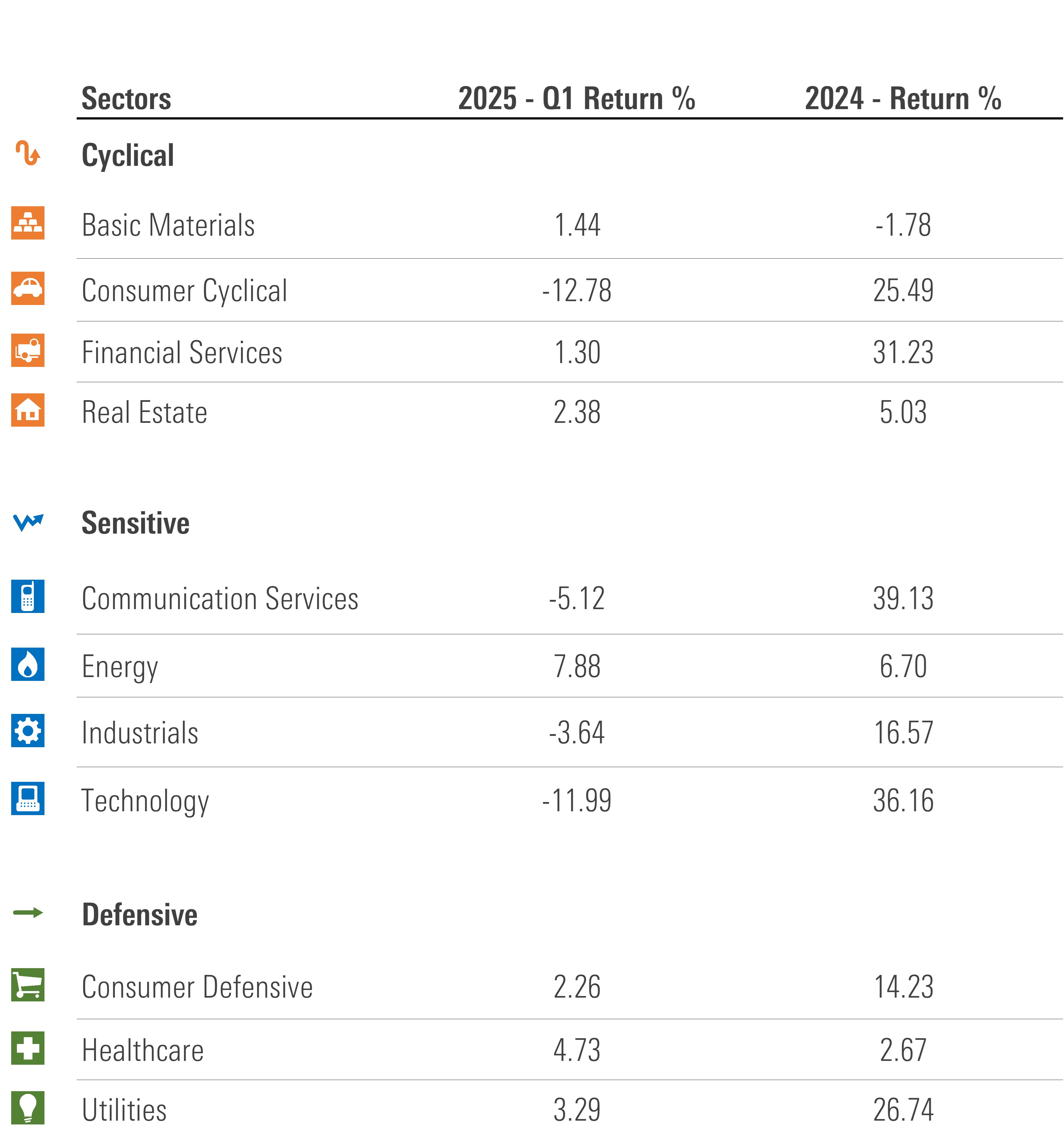

While diversification has protected portfolios so far in 2025, the real winners have been the contrarians. In addition to going global, one of my three takeaways from Morningstar’s 2025 Outlook was to “look beyond large growth and tech.” A bet on value stocks would have paid off, at least in relative terms. The Morningstar US Large-Mid Broad Value Index lost far less than its growth equivalent thanks to constituents like Berkshire Hathaway BRK.A BRK.B, JPMorgan JPM, and Exxon Mobil XOM. The two economic sectors called out by Dave Sekera as most attractively valued coming into 2025—energy and healthcare—have been the best performers of 2025.

Successful valuation calls don’t always play out this quickly. It can take ages for asset prices to converge with fair values, as the “momentum effect” exerts a powerful force on markets. Contrarian investing typically requires patience and intestinal fortitude before an inflection point comes. When market direction does change, momentum investors, who pile into the best performing assets, can get whipsawed. The Morningstar US Momentum Factor Index, which came into 2025 with Nvidia as its top constituent, is in the red so far in 2025.

But even as some underperforming investment “factors” have made a comeback, others continue to languish. US small-cap stocks, another attractive asset class cited by Morningstar’s research and investment team coming into 2025, have failed to benefit from any rotation. The Morningstar US Small Cap Extended Index lost more than the broad stock market in the first quarter of 2025, extending a miserable run of underperformance.

Small caps in the US have lagged in both up markets and down markets, as well as rising and falling interest-rate regimes. Perhaps their day will come. But until then, contrarians who bet big in small caps, die-hard believers in the “size premium,” and those who diversify across the market-cap spectrum, must continue to wait.

At least the diversified have several other asset classes going for them. The nature of diversification is that some portfolio component is always underperforming. But in tricky market conditions like 2025’s first quarter, exposure to a range of assets can work to investors’ advantage. With “uncertainty” clouding markets, staying diversified makes sense going forward. For valuation-driven investors, I recommend Morningstar’s Stock Market Outlook for Q2.

The author or authors own shares in one or more securities mentioned in this article.

Find out about Morningstar’s editorial policies.

Morningstar, Inc., licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. A list of ETFs that track a Morningstar index is available via the Capabilities section at indexes.morningstar.com. A list of other investable products linked to a Morningstar index is available upon request. Morningstar, Inc., does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}