IEA’s World Energy Outlook systemically underestimates solar PV development

April 11, 2025

Since its founding in 1973, a fundamental purpose of the IEA has been the coordination of global responses to energy crises. With the ongoing climate crisis, IEA WEO scenarios have become the standard bearer for global energy projections, particularly the newly introduced Net-Zero Emissions by 2050 (NZE) scenario first published in 2021, in the IEA’s mission to aid countries in providing secure and sustainable energy for all. New research from LUT University examines projections in the outlook, representing business-as-usual conditions and the normative, targeting higher levels of sustainability scenarios, in all WEOs published from 1993-2022. The study, titled “Paving the way towards a sustainable future or lagging behind? An ex-post analysis of the International Energy Agency’s World Energy Outlook”, has been published in the scientific journal Renewable and Sustainable Energy Reviews.

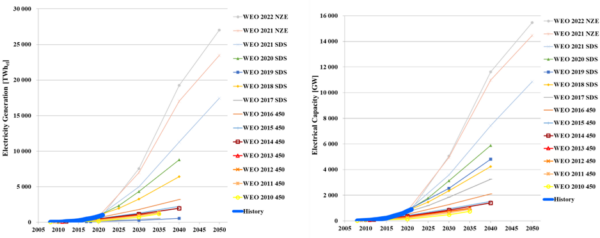

The analysis indicates that, while projections for top-level indicators such as primary and final energy demand have largely been accurate, projections for renewable energy growth across all WEOs have largely underestimated the unprecedented growth in variable renewable electricity, especially solar PV, a finding confirmed by Auke Hoekstra in 2019. The highest solar PV capacity reported is from the 2022 WEO NZE scenario at 15.5 TW by 2050, corresponding to about 27,000 TWh of electricity generation. While these values are within the range of published 100% renewable energy literature, they correspond to only 18% of total primary energy demand. Furthermore, renewable electricity only supplies 40% of primary energy. Conversely, previous research from LUT University has found a global installed solar PV capacity of 63.4 TW, with solar PV electricity generation at 69% of total primary energy demand and all primary renewable electricity generation at 87%. This fundamental finding was later adopted by the international solar PV community and is also monitored by the International Technology Roadmap for PV.

Annual solar PV installations further highlight the underestimations of solar PV growth as annual additions peak in the 2022 NZE scenario at 657 GW/year in 2040 before decreasing in 2050. This maximum solar PV installation rate is only slightly above the total installed capacity in 2024 at 593 GW. Given the rapid growth and low cost of solar PV, global markets for PV can be expected to reach 1 TW/year between 2025 and 2030 and may reach 3 TW/year in the course of the 2030s, well beyond what the IEA has projected. The question then becomes, why do even the most ambitious IEA scenarios lead to limited renewable electrification and growth of solar PV?

A core tenant of renewable energy system transition research is system-wide electrification. The results indicate that the share of electricity in the final energy demand reaches 49-52%, which is largely in line with the electrification of heat demands and road transport through battery electric vehicles and the value of smart charging of electric vehicles and their vehicle-to-grid opportunities. Integration of heat pumps is essential for the electrification of heating, and the 2022 NZE scenario projects that 52% of the building heating demand may be covered by 6.1 TW of heat pumps.

Direct electrification appears to be sufficiently considered in the 2022 NZE; however, this is not sufficient for system-wide defossilization, as the remaining 40-50% of final energy demand will require hydrogen and hydrogen-based fuels for high-temperature heat, long-distance shipping and aviation, and feedstocks in the steel and chemical industries. Fuel and feedstock demand in the 2022 NZE scenario largely appears to be covered by bioenergy and fossil oil. However, power-to-X routes using electricity-based hydrogen have been found to be able to defossilize fuel demands using e-Fischer-Tropsch liquids and e-ammonia. e-Methanol and e-ammonia will also be fundamental for industry to defossilize chemical feedstocks along with e-hydrogen to defossilize primary steelmaking and be supportive for further energy-intensive industries.

Such power-to-X routes, however, require a low-cost renewable electricity input to be economically viable. In turn, global energy systems will gain a significant amount of flexibility as electrolyzers can be operated as excess renewable electricity is available, reducing the quantities of electricity that will need to be balanced by storage. The lack of penetration of power-to-X in the normative WEO scenarios may be a factor limiting solar PV growth. Although hydrogen production in the 2022 NZE reaches about 12,000 TWhH2,LHV, only 41% is used as an intermediate for power-to-X conversion, and 27% of the hydrogen supply is blue hydrogen based on fossil fuels.

Without flexibility from energy system demand, the balancing of variable renewable electricity will have to come from storage, primarily battery storage. Battery storage capacity is available in the more recent WEOs, with the 2022 NZE projecting 3.9 TW by 2050. Previous research from LUT University finds that, by 2050, total battery capacity may reach upwards of 13.5 TW. Investigation into the model used for the WEO suggests that only utility-scale battery storage is included, but distributed prosumer batteries and vehicle-to-grid connections can provide inexpensive distributed storage to help match renewable electricity supply with demand.

All these factors contribute to future energy systems being able to accommodate high shares of solar PV and wind power and can support the development of a larger Power-to-X Economy. The large solar PV cost reductions largely favor sun-rich regions, where the majority of demand growth can be expected. In Pakistan, a “Solar Blitz” is occurring and could be a global example of how developing economies can rapidly install renewable electricity to decarbonize their electricity supplies and leapfrog over the commonly understood carbon intensity associated with economic growth

A similar change can be observed in Ethiopia as battery-based electric vehicles are rapidly being adopted.

If global changes can rapidly occur with enough societal willpower, why should the IEA not inspire global decision-makers with technically and economically feasible scenarios representing a best-case scenario for long-term climate stability – a fully renewable energy supply by 2050 featuring the enormous benefits of solar PV, wind power, other renewables, batteries, electric vehicles, heat pumps, and electricity-based fuels among highly relevant technologies for the arising Power-to-X Economy.

Authors: Gabriel Lopez, Dominik Keiner, and Christian Breyer

This article is part of a monthly column by LUT University.

Research at LUT University [] encompasses various analyses related to power, heat, transport, desalination, and negative CO2 emission options. Power-to-X research is a core topic at the university, integrated into the focus areas of Energy, Air, Water, and Business and Society. Solar energy plays a key role in all research aspects.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Popular content

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}