If I Had $5,000 to Invest in Artificial Intelligence (AI) Right Now, I’d Buy These 2 Stocks Before They Rebound

April 9, 2026

After dominating stock and business discussions over the past few years, artificial intelligence (AI) stocks are still getting a lot of attention — but for the wrong reasons. Through the first quarter of this year, many big-name AI stocks (and tech stocks in general) have started off on the decline.

Some investors are chalking up the sluggish start to an AI bubble “correcting” itself, while others think it means investors are seeking safer investments amid increasing uncertainty in the broader economy.

In either case, a handful of AI stocks look a lot more appealing after their recent declines. And although there’s no guarantee they bounce back in the near future, they’re great long-term investments worth getting into before what I’d consider a close-to-inevitable rebound.

Image source: The Motley Fool.

1. Microsoft

None of the “Magnificent Seven” stocks has had it as bad as Microsoft (MSFT 0.34%). Its stock is down over 21% as of April 6, reducing its market cap to around $2.7 trillion. You can argue that Microsoft’s valuation was high pre-drop, but this has been one of the roughest stretches the company has faced in quite a while.

Microsoft

Today’s Change

(-0.34%) $-1.26

Current Price

$373.07

Some investors haven’t agreed with Microsoft’s AI spending plans and potential slowdown in Azure growth (hence the stock decline), but Microsoft still remains one of the most thorough businesses in the world — regardless of sector.

Whether it’s enterprise software, operating systems, cloud computing, gaming, or hardware, Microsoft has its hands in many industries across the tech world, and thousands of businesses rely on it for their own daily operations. That alone makes it one of the more appealing long-term stocks investors can hold. You get the tech growth opportunities while also getting the long-term stability that you generally see with more “boring” blue chip stocks.

In its latest quarter (ended Dec. 31), Microsoft put up another impressive financial performance. Its revenue increased by 17% to $81.3 billion, its operating income (profit from core operations) increased by 21% to $38.3 billion, and its diluted earnings per share (EPS) increased 60% to $5.16.

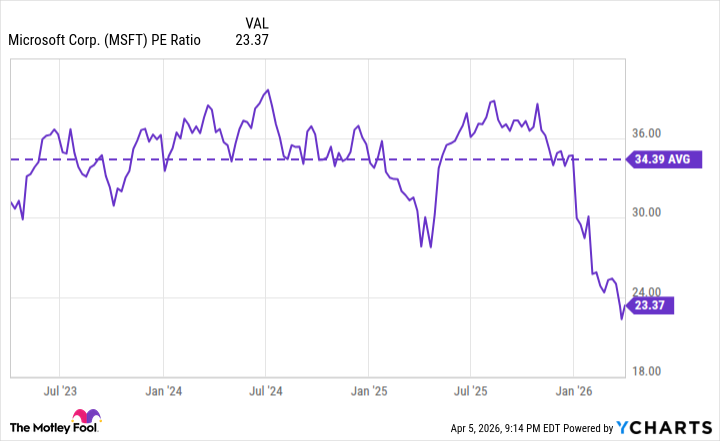

Microsoft is planning to spend over $100 billion in capital expenditures this year — with most of it going toward AI infrastructure — but that’s light work for a company consistently bringing in as much as Microsoft. It’s playing the long game, and its stock looks much more attractive, with a price-to-earnings (P/E) ratio of around 23.3.

MSFT PE Ratio data by YCharts

2. CrowdStrike

Like a handful of other software companies, CrowdStrike‘s (CRWD 7.49%) recent stock struggles can be traced back to new tools introduced by Anthropic, the owner of the popular tool Claude. Anthropic recently launched Claude Code Security, a cybersecurity tool that some fear could disrupt CrowdStrike’s business.

The February announcement led to CrowdStrike’s stock declining by over 17% from Feb. 19 to Feb. 23. It’s now down around 12% year to date through April 6.

CrowdStrike

Today’s Change

(-7.49%) $-31.95

Current Price

$394.56

CrowdStrike is one of the pioneers of AI-native cybersecurity solutions, with its Falcon platform having been released in June 2013. The amount of data CrowdStrike has been able to collect and use to train and refine its AI models is one of its biggest competitive advantages.

That’s not something a competitor can easily replicate; it takes years and trillions of data points collected. CrowdStrike has used this to create industry-leading solutions that many noteworthy companies rely on, including 300 of the Fortune 500.

There may be AI tools that work perfectly well for the average user, but many won’t be nearly as comprehensive as what corporations need. It’s not easy for large corporations to switch cybersecurity providers because of how ingrained many of them are in their daily operations and the logistics involved.

That doesn’t make CrowdStrike’s business disrupt-proof, but it surely helps with its sustainability, and why I think it’s a great long-term option. The stock is currently trading at around 21.4 times its projected sales over the next 12 months. That’s not cheap by most standards, but it’s well below its average over the past few years.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}