Is Tesla (TSLA) Pricing In Too Much Growth After Recent Share Price Pullback?

April 11, 2026

- If you are wondering whether Tesla’s share price still reflects its true value, you are not alone, especially with so many opinions on what the stock is really worth.

- Tesla closed at US$348.95 recently, with returns of 38.3% over 1 year, 88.6% over 3 years, and 41.5% over 5 years, alongside shorter term moves of a 3.2% decline over 7 days, an 11.7% decline over 30 days, and a 20.3% decline year to date that may be changing how some investors view its risk and return trade off.

- Recent headlines around Tesla have continued to focus on its role as a major electric vehicle and technology company, and on how sentiment toward growth oriented stocks in general feeds into its valuation. These stories help explain why the share price can move sharply in the short term even when long term views among investors shift more gradually.

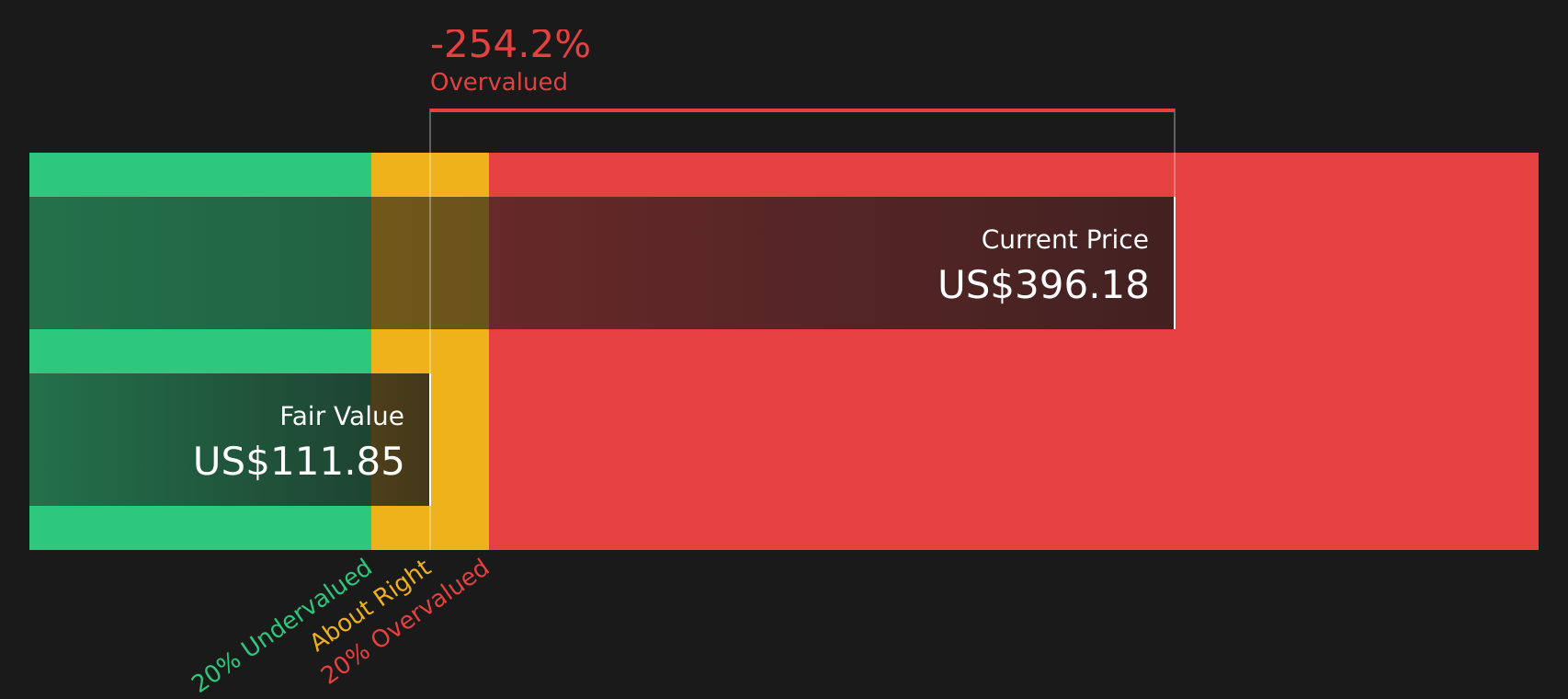

- Despite the strong long term return profile, Tesla currently has a valuation score of 0 out of 6. The next sections will walk through what different valuation methods are saying about the stock today and finish with a more holistic way to think about its value.

Tesla scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Advertisement

Approach 1: Tesla Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth today by projecting its future cash flows and discounting them back to the present.

For Tesla, the model uses a 2 Stage Free Cash Flow to Equity approach based on free cash flow of about $5.3b over the last twelve months. Analyst and extrapolated estimates then project cash flows through to 2035, with Simply Wall St extending forecasts beyond the first few analyst covered years.

Within these projections, free cash flow for 2030 is estimated at roughly $27.1b, with discounted values provided for each year to reflect the time value of money and risk. Adding these discounted cash flows together gives an estimated intrinsic value of US$155.04 per share.

Against a recent share price of US$348.95, the model implies the stock is about 125.1% above this DCF based estimate. This points to Tesla trading well above what this cash flow driven approach suggests.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Tesla may be overvalued by 125.1%. Discover 58 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Tesla Price vs Sales

For profitable companies, price-based multiples are a straightforward way to see how much you are paying for each unit of business performance. In Tesla’s case the preferred metric is the P/S ratio, which compares the company’s market value to its revenue and is often used when earnings are less representative of the business or can be more volatile.

Growth expectations and risk matter because investors usually accept a higher P/S ratio when they expect stronger growth and lower perceived risk. Slower growth or higher uncertainty tends to justify a lower, more conservative multiple.

Tesla currently trades on a P/S of 13.81x. This is well above the Auto industry average P/S of 0.57x and also above the peer group average of 0.78x. Simply Wall St’s Fair Ratio for Tesla is 3.09x, which is a proprietary estimate of what the P/S might be given factors such as earnings growth, industry, profit margin, market cap and key risks.

The Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for Tesla’s specific growth profile, risk characteristics and scale rather than assuming all Auto companies deserve similar multiples.

Comparing the Fair Ratio of 3.09x with the actual P/S of 13.81x suggests Tesla is trading above this benchmark.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Earlier it was mentioned that there is an even better way to think about valuation, so this is where Narratives come in. They give you a simple way to attach a story to your numbers by linking your view of Tesla’s future revenue, earnings and margins to a concrete forecast and fair value that you can compare directly with today’s share price.

On Simply Wall St’s Community page, Narratives are already being used by millions of investors to frame Tesla in very different ways, from fair values around US$30 per share to figures near US$2,500. Each Narrative spells out the assumptions behind that view rather than leaving them hidden.

When you select or build a Tesla Narrative, you are effectively choosing a coherent set of expectations. This could mean a focus on the core auto and energy businesses, a heavier weight on robotaxis and Optimus, or something in between. The platform keeps the forecast and fair value updated when new earnings, news or regulatory developments arrive so you can see how your thesis holds up over time.

For Tesla however we will make it really easy for you with previews of two leading Tesla Narratives:

Fair value: US$2,707.91 per share

Current price vs this fair value: about 87.1% below the narrative fair value

Revenue growth assumption: 77%

- This bullish Narrative breaks Tesla into five major lines, including Optimus robots, energy storage, FSD and software, automotive, and broader energy solutions, and assigns substantial profit potential to each by 2030.

- It applies P/E multiples of 25x to 50x to an estimated 2030 profit figure, discounts those values back, and arrives at fair value ranges above US$2,000 per share, well above recent trading levels used in the Narrative.

- The author sees Tesla as heavily tied to AI, robotics and energy at large scale and accepts significant execution, competition and regulatory risks in return for very large upside potential.

Fair value: US$322.21 per share

Current price vs this fair value: about 8.3% above the narrative fair value

Revenue growth assumption: 18%

- This Narrative focuses on Tesla as a technology driven auto and energy company built around Dojo, FSD, Optimus and Megapacks, but questions how much of that promise is already reflected in the share price.

- It assumes solid growth in automotive, energy storage and services, but treats Tesla as best valued on P/S, with expectations for strong execution balanced against concerns over sensor choices, regulation and competitive responses.

- The author highlights meaningful long term opportunities in autonomy and grid scale storage, while arguing that execution risks, technology choices and ambitious timelines can justify a fair value close to recent trading levels.

Do you think there’s more to the story for Tesla? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}