KOSPI Enters the 8,000-Era, and How South Korean Investors View Assets by Category

May 25, 2026

On May 15, as the KOSPI crossed the 8,000 mark for the first time in history and ushered in a full-fledged “8,000 era,” clear differences in investors’ perceptions of individual assets—including domestic stocks, U.S. stocks, and venture investments—came into focus. With the government launching the National Participation Growth Fund (hereinafter, the National Growth Fund), which will invest 150 trillion won over five years in advanced strategy industries, from May 22 through June 11 in a 600 billion won offering, interest from individual investors in investing in unlisted and technology firms is also being highlighted. According to a survey conducted by data collection platform PickPly of 1,000 adults nationwide who are interested in stock investing, investors are taking positioning strategies that are clearly differentiated depending on the nature of the asset.

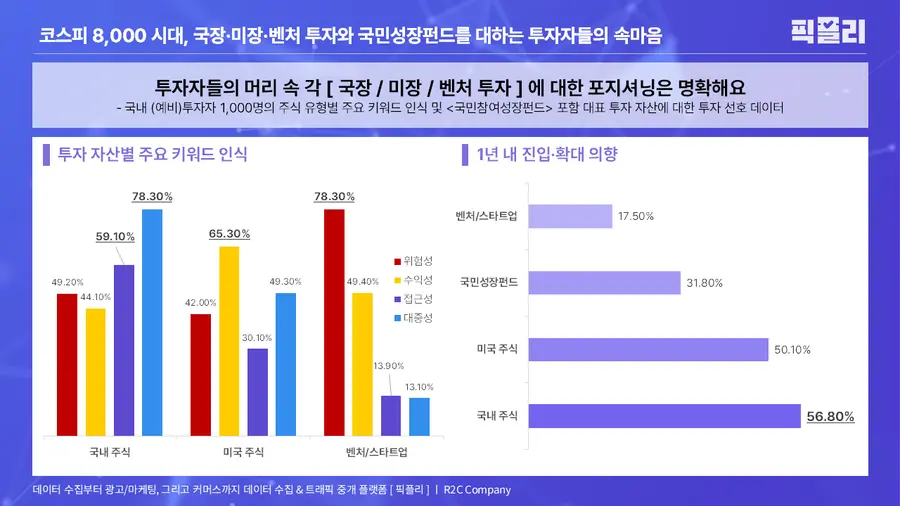

Domestic stocks: accessibility and mainstream appeal; U.S. stocks: profitability; venture investment: risk…distinct perceptions by asset type

The results show that 82.3% of all respondents held domestic stocks, while the share holding U.S. stocks stood at 56.1%. The proportion of people who held no stocks of any kind was only 9.4%. Looking at positive perception keywords by asset type, domestic stocks recorded overwhelming figures in information accessibility (59.1%) and mainstream appeal (78.3%), and also ranked No. 1 in intention to expand investment within the next one year (56.8%). By contrast, U.S. stocks received the highest evaluation in terms of profitability (65.3%). Notably, the perception of risk for U.S. stocks was 42.0%, lower than domestic stocks (49.2%). The analysis suggests that for Korean investors, U.S. stocks have become an asset with strong appeal for returns while carrying relatively less risk. However, the positive perception of information accessibility was only 30.1%, about half of domestic stocks (59.1%). That means domestic stocks still hold the position as the “asset where it is easy to get information.” When it comes to venture and startup investing, 78.3% of investors cited risk, indicating they viewed it as an extremely risky asset. The intention to expand investment within a year was also the lowest at 17.5%.

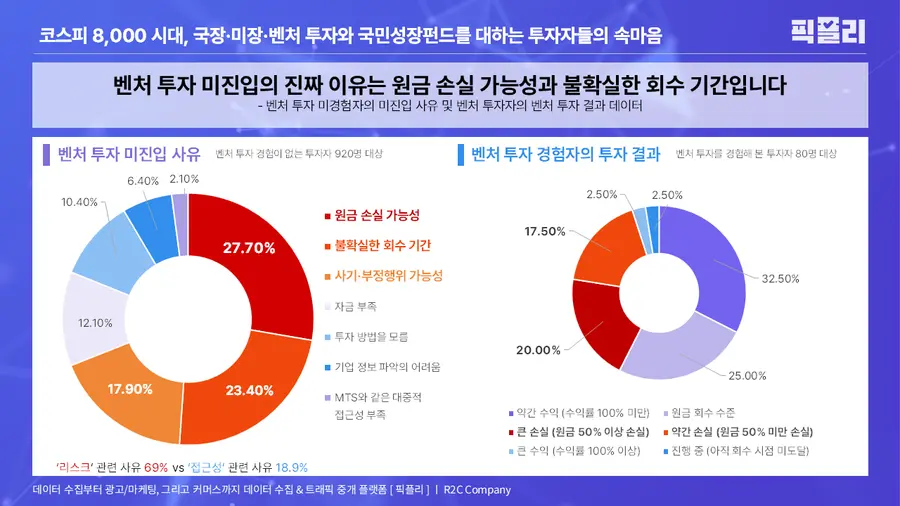

Why people don’t invest in venture capital: 69% “risk”…those with loss experiences outnumber those with profit experiences

In a survey of 920 people who have never had venture investment experience about the reasons they did not invest, risk-related factors accounted for 69% of the total, including the possibility of losing principal (27.7%), an uncertain recovery period (23.4%), and the possibility of fraud or improper conduct (17.9%). Among 80 people with actual venture investment experience, there were more investors who suffered losses (37.5%) than those who made profits (35.0%). And the number of people who experienced major losses—losing 50% or more of their principal (20.0%)—was about eight times higher than those who made gains of 100% or more (2.5%). Investors’ concerns were confirmed not only in sentiment but also in the actual data.

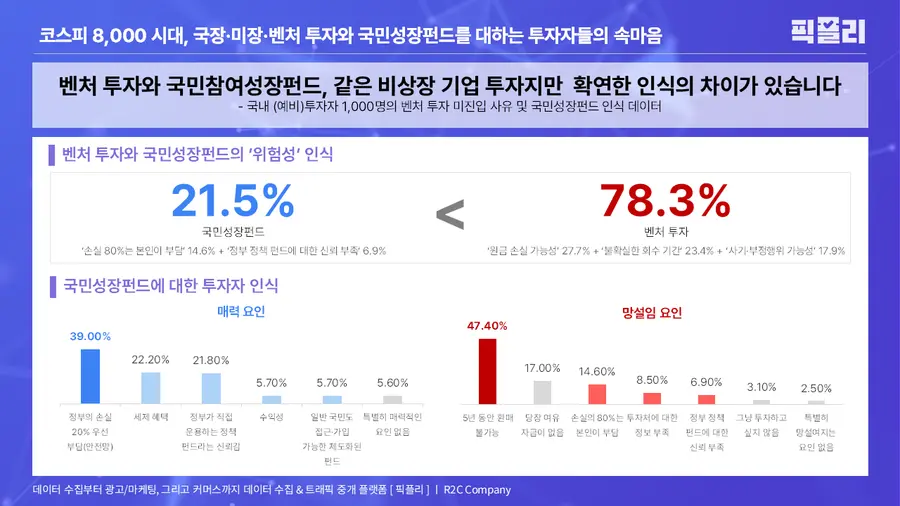

The National Growth Fund, an asset like venture investment, but risk perceptions are less than half

One notable point is that even though it involves investment in unlisted companies, the perception of the government’s National Growth Fund differed sharply from general venture investment. The perception of risk for venture investment was 78.3%, the highest among the three investment assets. But among the factors that make investors hesitate about investing in the National Growth Fund, even when all risk-related items are added up, it was only 21.5% (14.6% “I bear an 80% loss” + 6.9% “Lack of trust in government policy funds”). In other words, even though both investment routes expose investors to the same pool of assets, the perceived weight of risk has been reduced to less than half.

The intention to enter and expand investment in the National Growth Fund within one year was 31.8%, far higher than for venture investment. Investors pointed to the government’s priority assumption of a 20% loss (39.0%) as the biggest attraction of the National Growth Fund. This was followed by tax benefits (22.2%) and confidence in government management (21.8%). Unlike in general venture investment, where investors worried most about principal loss, in the National Growth Fund, the biggest hesitation factor was identified as the lock-up condition that prevents redemption for five years (47.4%), rather than loss concerns (14.6%). This suggests that the government’s institutional safety net significantly eased investors’ risk burdens.

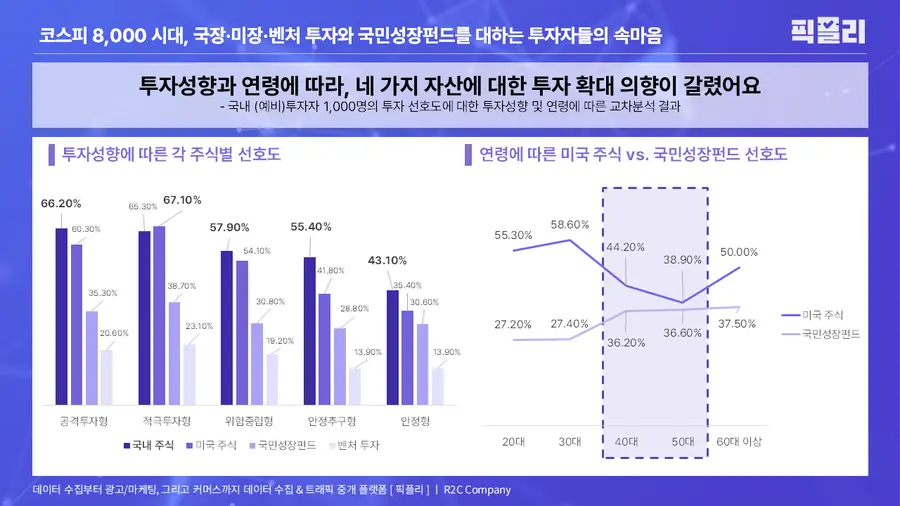

Even with different investment styles, the preference rankings are similar…only active investors say “U.S. stocks are ahead of K-stocks”

The most noteworthy result from cross-analysis by investment style and age group was that in all five style groups—ranging from aggressive investors to conservative ones—the ranking of preferred assets generally followed the order: domestic stocks, U.S. stocks, the National Growth Fund, and venture investment. The ratio distribution across the different styles was also relatively even. However, for active investors, U.S. stocks (67.1%) edged out domestic stocks (65.3%), and it was the only case where the rankings differed. Differences by style also emerged. Active investors showed higher intentions toward the National Growth Fund and venture investment than other groups. Conservative investors, for most assets, took a more cautious stance, but for the National Growth Fund they still showed a preference that did not lag as far. By age, people in their 20s and 30s preferred U.S. stocks more than those aged 40 and above, while the 40-and-over group showed relatively higher preference for the National Growth Fund. Overall, among all age groups except those in their 30s, domestic stocks still showed the highest preference.

With the KOSPI breaking through the 8,000 level and the government opening up the unlisted sector, Korea’s capital market is entering a transition period where familiar areas and new ones coexist. As it has been confirmed that when institutional safety nets allow the public to offset risk, they move into unfamiliar asset classes, observers expect the asset management industry and the startup investment market to focus on designing customized products that meet demands by generation and investment style, and building trust based on data.

* Survey and data collection methods

-

Period: May 15, 2026, 11:19:35 p.m. to May 16, 2026, 10:45:45 p.m. (24 hours)

-

Method: Online (app) first-come, first-served participation

-

Number of participants: 1,000 people, Korean (prospective) investors (PickPly users)

-

Participants’ gender: Men 50.0% (500 people), Women 50.0% (500 people)

-

Participants’ age: 20s 21.7% (217 people), 30s 29.2% (292 people), 40s 27.6% (276 people), 50s 17.5% (175 people), 60s and above 4.0% (40 people)

-

Participants’ occupation: office workers 62.0% (620 people), unemployed/leave of absence 11.0% (110 people), freelancers 10.1% (101 people), self-employed/business owners 8.6% (86 people), college/university students and graduate students 8.3% (83 people)

-

Investment style: stable-seeking 32.3% (323 people), risk-neutral 29.2% (292 people), active 17.3% (173 people), stable 14.4% (144 people), aggressive 6.8% (68 people)

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}