Last Week in Crypto: Lending sinks, Ethereum losing ground

April 21, 2025

|

Getting your Trinity Audio player ready… |

Crypto lending shrinks 43% since peak

Last week, Galaxy Digital released a report titled The State of Crypto Lending, which examined both centralized and decentralized lending and borrowing across the crypto ecosystem.

We don’t hear as much about decentralized finance (DeFi) anymore, so let’s quickly revisit what it is. DeFi refers to blockchain-based alternatives to traditional financial services like borrowing, lending, and earning yield on deposits. While DeFi has often been lumped together with non-fungible tokens (NFTs), initial coin offerings (ICOs), and memecoins, it was initially supposed to bring conventional financial services to the blockchain.

What stands out most in the Galaxy report is the scale of the collapse in the crypto lending market, which began to unravel in 2022 and hasn’t recovered since. A leading factor in the demise of the space was that many of the biggest lenders—including Genesis, Celsius Network, BlockFi, and Voyager—all filed for bankruptcy, which wiped out a lot of market value in the process. According to Galaxy, the total size of the crypto lending market was $36.5 billion as of Q4 2024, down 43% from its all-time high of $64.4 billion in Q4 2021.

Galaxy thinks the market will bounce back, as it is already on an upswing from its lows, but I’m personally not so sure. Many people got burned by these lending products, especially if they were holding an instrument offered by one of the companies that collapsed. Beyond that, if you’re new to crypto, the mechanics behind these platforms are more confusing than they are attractive.

On top of that, the demise of some of the large lenders and the well-known stories of risk being mismanaged by them have created a trust problem in the space. When four of the biggest players go bankrupt in the span of two years, it’s hard to convince anyone, especially newcomers, that even though you essentially have the same business model, that “this time will be different.”

I don’t think lending will disappear, but getting new users on board will be an uphill battle unless a real need for these lending services emerges or yields become so attractive that users cannot pass up staking their coins to earn interest.

Donald Trump might be launching a Web3 game

It’s rumored that Donald Trump is launching a crypto game. According to reports, the game allegedly has a Monopoly-like feel and is being spearheaded by Bill Zanker, the same individual who helped launch Trump’s NFTs and memecoin.

While there is not much information on how the game will work or even how cryptocurrency will be involved, what is known is that the game is expected to launch later this month. Unfortunately, Trump and his team could not have picked a worse time to launch, as the Web3 gaming market is shrinking, not growing.

According to DappRadar, investments in Web3 gaming totaled just $91 million in Q1 2025—a 71% drop from Q4 2024. Daily unique active wallets in the space also declined by 3% over the same period, which suggests that the market is cooling off from a user perspective.

Launching a crypto game in this kind of climate may be more of a challenge than it is a financial boon, especially with the memory of Trump’s most recent crypto failure fresh in the heads of potential investors and users: the launch of the $TRUMP memecoin, which has been down more than 85% since its launch date.

Ethereum down 48% in the last year

The past few years have been challenging for nearly every cryptocurrency, but most major coins have seen some kind of rebound over the last year—except Ethereum. While many of the household-name tokens have posted small gains or losses over the last year, Ethereum is down 48% and showing no signs of recovery.

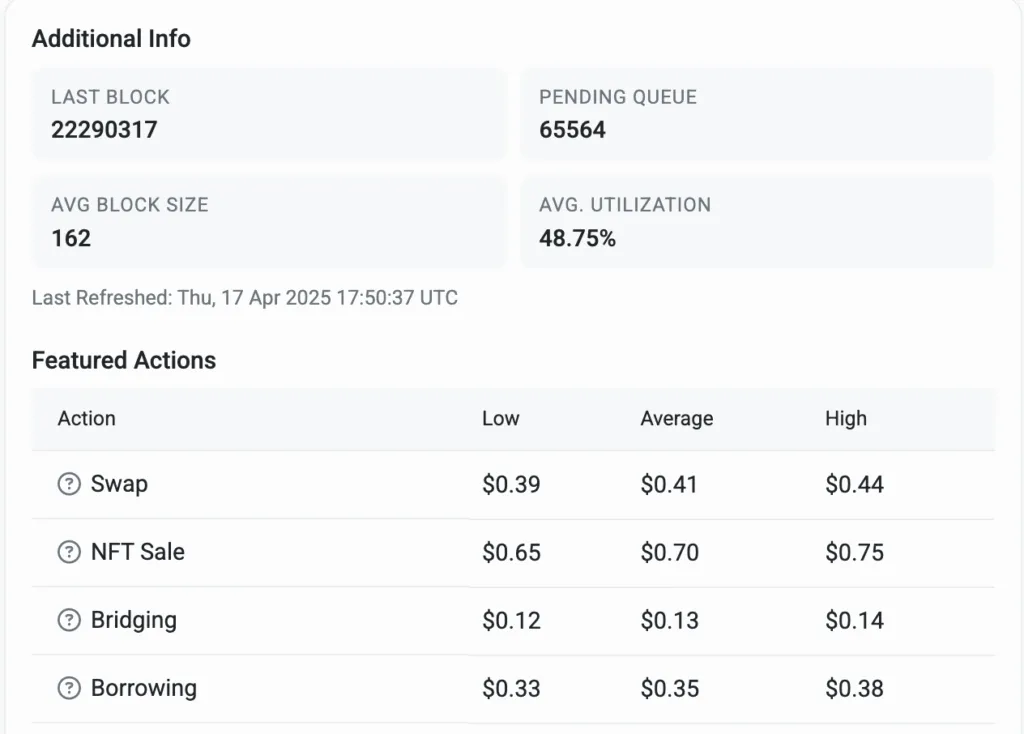

One of the biggest reasons Ethereum is losing ground is simple: cost. Despite network upgrades, the transaction fees on Ethereum remain significantly higher than those on competing chains. At the time of writing, common on-chain actions on Ethereum can cost well over ten cents each, while on some of the top competing chains, those same actions usually cost fractions of a penny.

That may not sound like much, but those fees matter at scale or for users in emerging economies. Whether you’re a founder trying to launch a DeFi product or just someone looking to interact with a decentralized application (dApp), Ethereum can quickly become cost-prohibitive. In some cases, users even have to “top off” their wallets just to afford the transaction fees, which isn’t a great user experience.

But the purpose of this segment isn’t to drag Ethereum, it’s to highlight what Ethereum’s struggles tell us about the broader market.

I think Ethereum’s demise reveals that the market doesn’t care about legacy status anymore—it used to be enough to be one of the first few name-brand coins or tokens that existed. But now, it looks like individuals who are actually using blockchains or interested in using blockchains care more about affordability. To be fair, brand recognition still matters, but just because a blockchain had brand recognition in the past does not mean it will keep that status if it falls out of favor with blockchain enthusiasts. If a blockchain nails those two criteria, it will attract both users and developers.

If it fails in either of those areas—especially while competitors are gaining ground—it risks becoming less relevant. Ethereum still has name recognition, but right now, it is severely lacking when it comes to affordability, which is why creators are opting to use other blockchains, which is drawing users away from Ethereum to these other chains and why the market price is reflecting its dissatisfaction with the Ethereum.

Watch | Mining Disrupt 2025 Highlights: Profitable trends every miner should know

Recommended for you

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}