Leopold Aschenbrenner’s Situational Awareness Fund Just Bought This Nvidia-Backed Neocloud Stock

May 28, 2026

Renting out artificial intelligence (AI) computing power to businesses hungry for GPUs has become one of Wall Street’s most closely watched new investment themes. This emerging class of winners sits at the center of the AI build-out, benefiting from surging demand for compute infrastructure as companies race to train and deploy increasingly large models.

AI researcher-turned-investor Leopold Aschenbrenner’s Situational Awareness Fund disclosed a 5.6% stake in one of the hottest AI-infrastructure companies, Nebius Group (NBIS +8.53%), a company where Nvidia (NVDA +0.80%) will also invest $2 billion by 2030.

Image source: Getty Images.

Wall Street’s appetite for AI infrastructure grows

On May 13, Nebius reported a 684% increase in first-quarter revenue on a year-over-year basis. However, investors did not expect the 43% and 50% positive surprises in EBITDA and adjusted EPS, respectively. The market duly responded with a 24% rise in Nebius’ stock price over the next couple of days.

Yesterday’s disclosure by the $13.7 billion Situational Awareness Fund has only poured more fuel on Wall Street’s growing appetite for AI infrastructure stocks.

Leopold Aschenbrenner, a former researcher at OpenAI, gained widespread attention in 2024 when he published a 165-page essay titled Situational Awareness: The Decade Ahead, where he argues that artificial general intelligence (AGI) would arrive sooner than almost everyone expected and has geopolitical implications.

However, his rising status as an investor may prove to be equally important as his prediction. Despite having no formal investing experience, the 25-year-old launched a fund last year bearing the same name as his essay, quickly attracting significant investor inflows.

The development signals that those once closest to the AI revolution on the technological side of things are now proactively placing their capital behind the technological infrastructure that will drive it. In short, the AI trade is evolving from speculation into a far more sophisticated intersection of researchers, technologists, and investors who see computing infrastructure as the next strategic bottleneck to profit.

The “neocloud” era is here

Unlike traditional cloud giants that offer broad services for websites, databases, and corporate software, Nebius is building out its cloud segment specifically for the AI era. As a “neocloud” provider, it focuses primarily on renting out high-performance graphics processing units (GPUs) used to train and run AI models.

Enterprises and start-ups that suddenly needed enormous amounts of AI computing power often struggled to secure access from larger cloud providers, such as Amazon Web Services, Microsoft Azure, or Google Cloud.

That’s where neocloud providers stepped in. By building GPU-heavy data centers optimized for AI workloads, they offer specialized infrastructure tailored for machine learning developers and inference-heavy tasks.

Investors are increasingly interested in this industry because these firms proverbially sit at the center of the AI boom, supplying the computing backbone needed to power modern artificial intelligence applications.

Nebius Group

Today’s Change

(8.53%) $17.78

Current Price

$226.15

Nvidia’s backing suggests depth

Nvidia’s $2 billion investment in Nebius reflects the chipmaker’s confidence in the neocloud provider’s full AI technology stack that’s required to build, train, deploy, and run artificial intelligence systems — from raw computing hardware all the way to user-facing applications.

Nebius plans to deploy over 5 gigawatts of AI computing capacity by the end of 2030, including multiple gigawatt-scale AI factories across the United States, and will deploy Nvidia’s next-generation hardware, including upcoming GPU architectures like Rubin, Vera CPUs, and Bluefield storage systems. Nvidia is, however, far more closely involved with this project.

The companies will collaborate to build an inference stack for developers and businesses, while also implementing the chipmaker’s monitoring systems for GPU health and software optimization recommendations.

Investors have reacted positively, driving the stock up 103% since the collaboration was announced in March.

Why Nebius has outpaced rivals

Over the past 12 months, Nebius stock has risen nearly sixfold. The real question is whether that surge is actually justified. That should partly answer whether it’s a good investment going forward.

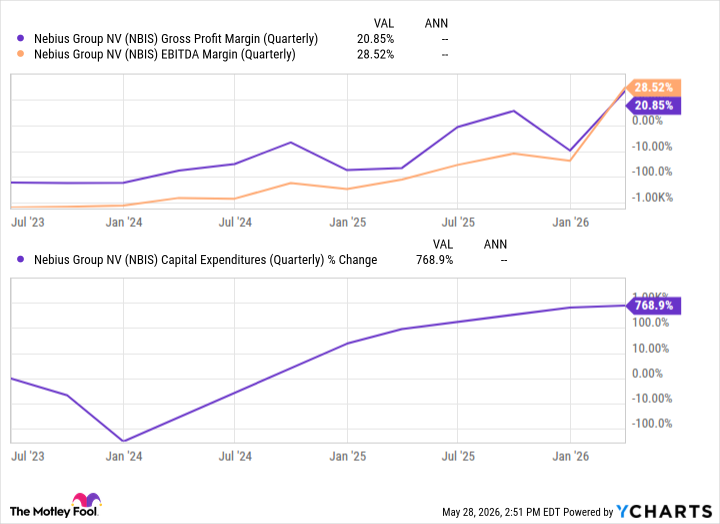

One of the overlooked items in Nebius’s financial performance has been its improving profitability. While revenue growth remains important, investors are ultimately focused on whether that expansion translates into earnings. Nebius hasn’t only been growing superficially, but also showing signs of stronger underlying profitability.

Simultaneously, there has been a significant increase in capital expenditures, suggesting Nebius looks increasingly capable of deploying greater amounts of capital at scale and improving profitability, as seen below.

NBIS Gross Profit Margin (Quarterly) data by YCharts.

Now there are definite risks. Profit margins in the AI-infrastructure space can compress as competition increases. But that isn’t something that can happen overnight, at least not from infrastructure upstarts like Nebius. Among the biggest challenges infrastructure providers face is ensuring uninterrupted access to energy to power AI factories.

Last week, Nebius signed a $2.6 billion deal with Bloom Energy (BE 1.18%) that guarantees 250 megawatts of power capacity and 328 megawatts of installed capacity over the next 10 years. However, that is only a fraction of Nebius’s requirements over the next few years.

However, well-funded hyperscalers could pose significant competition as new AI-specific infrastructure becomes available.

What’s in it for investors?

So the real question boils down to this: Can Nebius maintain or increase profitability as it deploys increasingly huge amounts of capital? Of course, revenue will continue growing as management mentioned in the latest earnings call that “everything we build, we sell.”

Nebius’s greatest advantage lies in being an early mover in implementing the latest available AI chips, given the incredible demand that creates a GPU bottleneck and, hence, the ability to price its offerings at a premium. That isn’t going to go away anytime soon.

Nebius generated less than $900 million over the last four quarters and is currently pricing in revenue expectations of $3.5 billion for 2026 and $11 billion for 2027. At the current market cap of roughly $58 million, the forward price-to-sales ratios for this year and the next are 16.6 and 5.3, respectively.

Whether that valuation is expensive or cheap ultimately depends on investors’ willingness to underwrite long-term growth in AI infrastructure. Given the five- to ten-year horizon typically required to build out large-scale AI capacity, some investors may view current pricing as relatively conservative for a company positioned in one of the most capital-intensive and rapidly expanding segments of the technology industry.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}