Meta Faces a Multibillion-Dollar EU Fine Risk. Here’s What It Means for the Stock at 17x Earnings

June 14, 2026

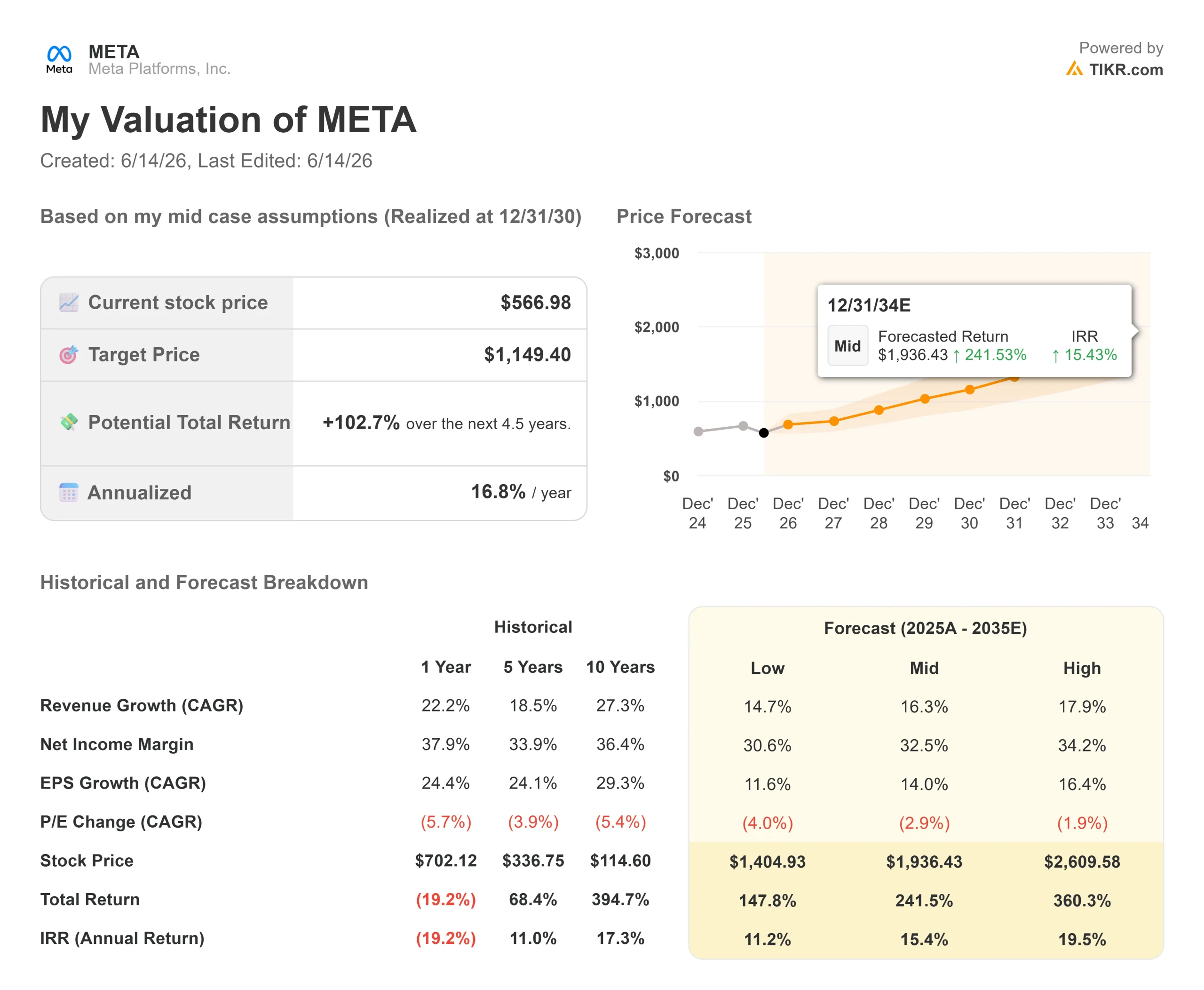

- Current Price: $566.98

- Street Target (Mean): ~$830

- Implied Upside to Street Target: ~46%

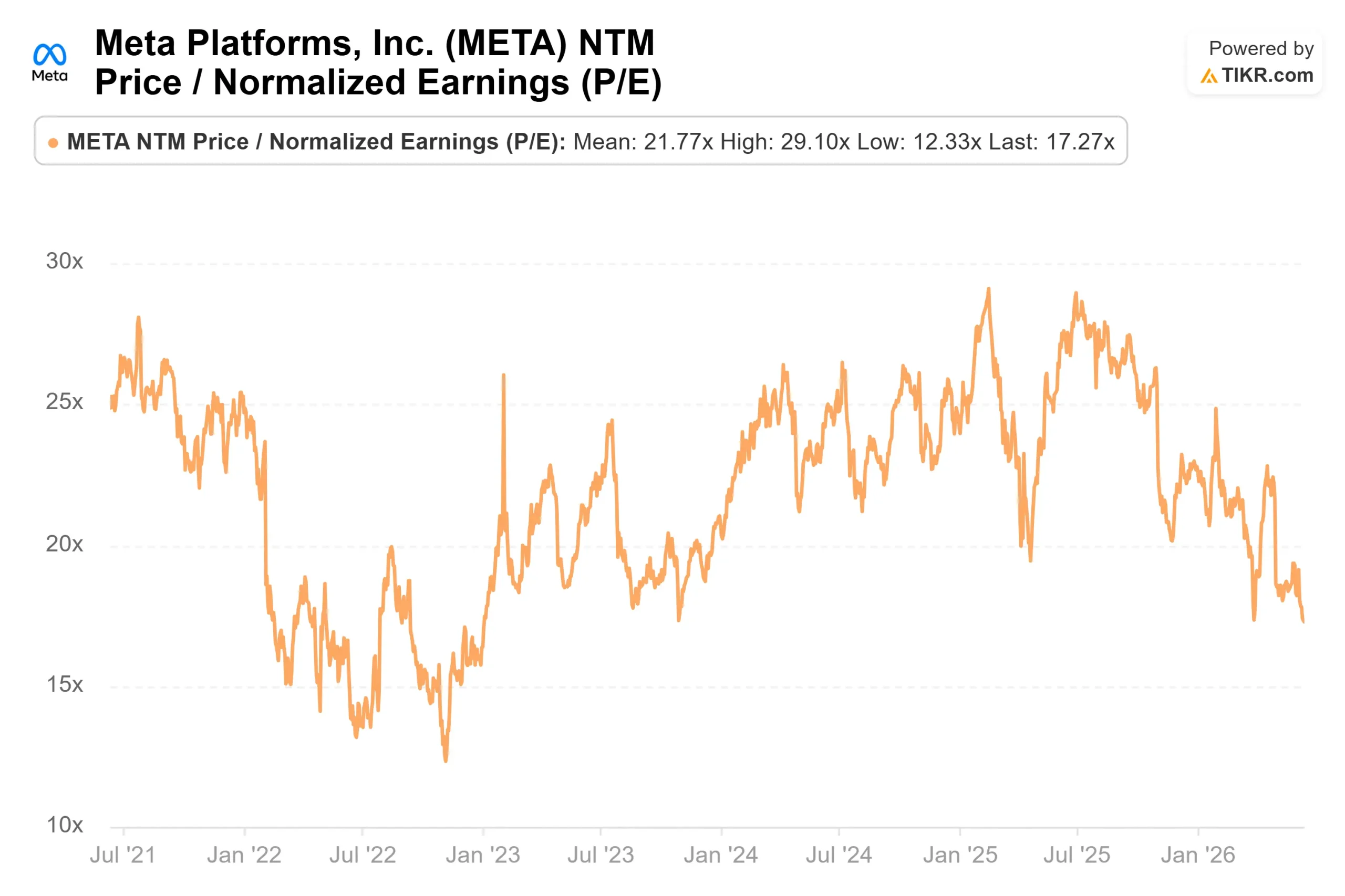

- NTM P/E: 17.27x

- LTM EBIT Margin: 41.2%

- Earnings Reaction: (8.55%) (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Meta Platforms (META) is the world’s largest advertising business, and in 2026, the market is treating Meta stock like a company in trouble. The shares closed at $566.98 on June 12, about 28% below the 52-week high of $796.25 and only 9% above the low. Bulls and bears are not fighting over whether the ad engine works, because it grew 33% last quarter. They are fighting over two things the market cannot yet price: how much Meta’s European regulatory problems will cost, and whether the largest spending program in its history will pay off.

The regulatory question sharpened this spring. On April 29, the European Commission issued preliminary findings that Instagram and Facebook breach the Digital Services Act, the EU’s online-safety rulebook, by failing to keep children under 13 off their platforms. If confirmed, the Commission can impose a fine of up to 6% of Meta’s worldwide annual turnover, which in 2025 revenue would approach $12 billion, plus ongoing penalties until Meta complies. Meta says it disagrees and is rolling out new age-detection tools. The pressure did not ease in June: on June 3, an EU court issued a mixed ruling that struck down the “gatekeeper” label on Facebook Marketplace but upheld it for Messenger.

The fine is a headline. The capital expenditure is the thesis. Meta’s last three quarters have run the same script: management raises spending guidance, investors recoil, the stock falls. Q1 2026 was the latest repeat. Revenue of $56.3 billion beat estimates and grew 33% year-over-year, yet the stock fell 8.55% on the day. The trigger was one line in the outlook: Meta lifted its 2026 capital expenditure forecast to $125 billion to $145 billion, up from $115 billion to $135 billion.

Management was candid about the why. “Our experience so far has been that we have continued to underestimate our compute needs even as we have been ramping capacity significantly,” CFO Susan Li told investors. For a market already nervous about spending, an admission that the company keeps spending more than planned is not reassuring, and multiyear cloud and infrastructure deals drove a $107 billion step-up in contractual commitments in the quarter alone.

CEO Mark Zuckerberg framed the bet plainly. “People will be more important in the future, not less,” he said, casting the spend as a wager that individuals using AI agents, not one centralized system, drive the next wave of value. His road map is the same loop Meta has run for two decades: build leading models, turn them into leading products, then “drive up the efficiency of it towards increasing profitability.” The open question is whether the gap between spending and profit lasts one year or several.

See historical and forward estimates for Meta Platforms stock (It’s free!) >>>

Here is the tension. The ad business is not slowing: impressions grew 19% in Q1, and average price per ad rose 12%, both helped by AI improvements to ad ranking. Meta AI sessions per user climbed into double digits after the launch of Muse Spark, its first in-house Superintelligence Labs model. These are measurable returns, not promises.

Yet the stock trades at an NTM P/E of 17.27x, near the low end of its multi-year range, while its forward two-year revenue CAGR is still 22.6%. The discount to peers is stark. Alphabet trades at 28.78x forward earnings and Reddit at 22.13x, while Meta sits at the cheapest of the group despite owning the widest reach and the highest margin, a 41.2% LTM EBIT margin. The discount is not the fundamentals talking; it is the fear of the spending cycle and the legal overhang.

That fear is not irrational. Free cash flow is set to run thin through 2026 as spending peaks, and the signed commitments leave management little room to pull back. If AI monetization beyond advertising arrives slowly, or the EU fine lands near the top of the range, the multiple could stay compressed well into 2027. The bet here is not that nothing goes wrong. It is that the price already assumes plenty will.

See how Meta Platforms performs against its peers in TIKR (It’s free!) >>>

- Current Price: $566.98

- Street Target (Mean): ~$830

- Implied Upside to Street Target: ~46%

- NTM P/E: 17.27x

See analysts’ growth forecasts and price targets for Meta Platforms stock (It’s free!) >>>

The Street’s mean price target of around $830 implies roughly 46% upside from today’s price, and TIKR’s mid-case model points to even larger gains over its multiyear horizon. The two revenue drivers are continued advertising growth, powered by AI improvements to ad ranking and pricing, and early monetization of newer surfaces like Threads, WhatsApp messaging, and business AI agents. The margin driver is operating leverage in the Family of Apps segment, where AI lifts conversion without a matching rise in headcount. The primary risk is the spending cycle: if the AI buildout does not convert to profit on schedule, free cash flow stays pressured and returns compress.

The upside case is simple: Meta is the lowest-multiple mega-cap advertiser, and any easing of spending or legal fear could re-rate it sharply. The downside case is equally clear: a large EU fine plus a slow AI payoff could keep the stock stuck near current lows.

Watch the next spending update and the margin that comes with it. Meta reports Q2 2026 in late July, with revenue guided to $58 billion to $61 billion. The number that matters is not the top line, which will likely beat; it is whether operating margin holds near 40% while capital expenditure peaks. A margin in the high 30s tells investors the spending is being absorbed. A sharp drop confirms the bears. On the legal front, watch for the Commission to move from preliminary finding to a final decision, which would turn the fine from a risk into a number. Until both resolve, the cheapest mega-cap advertiser in the market stays cheap for a reason the market can name but cannot yet measure.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Meta Platforms, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Meta Platforms alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Meta Platforms on TIKR Free →

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}