MicroStrategy Admits a Bitcoin Sale Is Possible—Here’s When

November 30, 2025

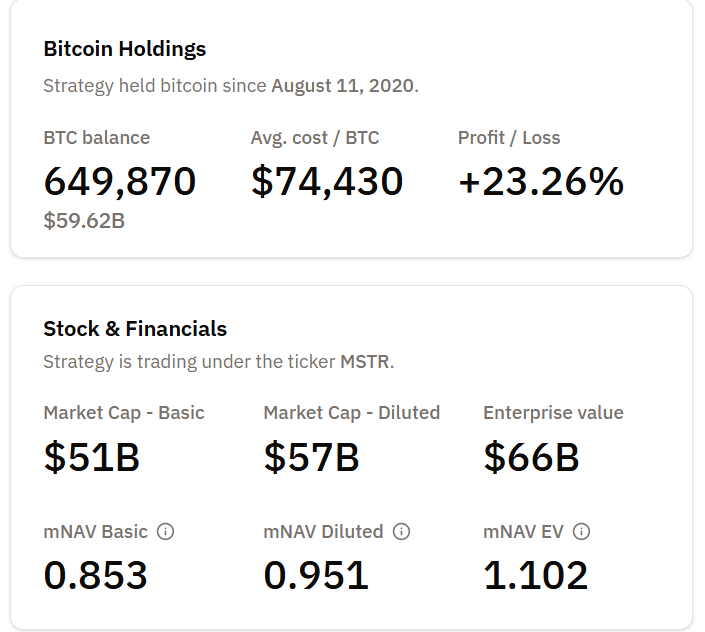

MicroStrategy CEO Phong Le has, for the first time, acknowledged that the company could sell its 649,870 BTC holdings under specific crisis conditions.

This marks a significant shift from Chairman Michael Saylor’s long-standing “never sell” philosophy and signals a new chapter for the world’s largest corporate Bitcoin holder.

SponsoredSponsored

MicroStrategy has confirmed a scenario almost no one thought possible: the potential to sell Bitcoin, its core treasury asset. Speaking on What Bitcoin Did, CEO Phong Le outlined the precise trigger that would force a Bitcoin sale:

- First, the company’s stock must trade below 1x mNAV, meaning the market capitalization falls below the value of its Bitcoin holdings.

- Second, MicroStrategy must be unable to raise new capital through equity or debt issuance. This would mean capital markets are closed or too expensive to access.

Le clarified that the board has not planned near-term sales, but confirmed that this option “is in the toolkit” if financial conditions deteriorate.

This is the first explicit acknowledgement, after years of Michael Saylor’s absolutist claim that “we will never sell Bitcoin.” It shows that MicroStrategy does, in fact, have a kill-switch tied directly to liquidity pressure.

mNAV compares MicroStrategy’s market value to the value of its Bitcoin holdings. When mNAV drops below 1, the company becomes worth less than the Bitcoin it owns.

SponsoredSponsored

Several analysts, including AB Kuai Dong and Larry Lanzilli, note that the company is now facing a new constraint. The mNAV premium that powered its Bitcoin-accumulation flywheel has nearly vanished for the first time since early 2024.

As of November 30, mNAV hovers near 0.95x, edging uncomfortably close to the 0.9x “danger zone.”

If mNAV falls below 0.9x, MicroStrategy could be pushed toward BTC-funded dividend obligations. Under extreme conditions the firm would be compelled to sell portions of its treasury to maintain shareholder value.

The pressure stems from $750–$800 million in annual preferred share dividend payments, issued during MicroStrategy’s Bitcoin expansion.

SponsoredSponsored

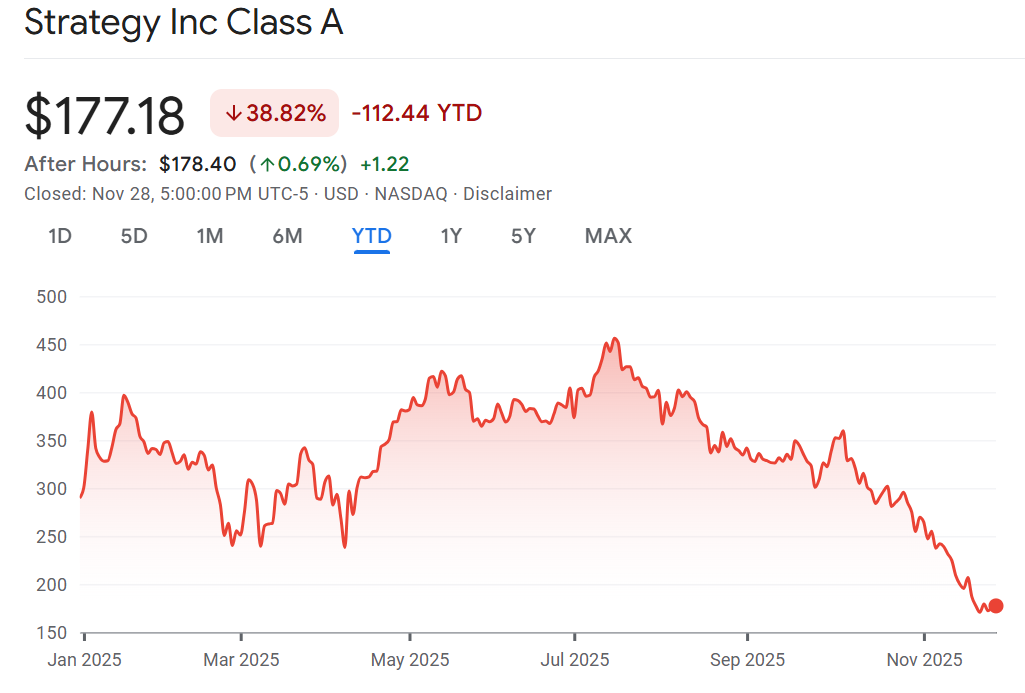

Previously, the company used new equity issuances to cover these costs. With the stock down more than 60% from its highs and market skepticism rising, that avenue is narrowing.

According to Astryx Research, MicroStrategy has effectively transformed into a “leveraged Bitcoin ETF with a software company attached.” That structure works when BTC rises, but amplifies stress when liquidity tightens or volatility spikes.

SponsoredSponsored

SEC filings have long warned about liquidity risk during a deep Bitcoin drawdown. While the firm maintains that it faces no forced liquidation risk due to its convertible debt structure, the CEO’s latest comments confirm a mathematically defined trigger for voluntary sales.

MicroStrategy is the largest corporate BTC holder in the world. Its “HODL forever” stance has been a symbolic pillar of the institutional Bitcoin thesis. Acknowledging a sell condition, even if distant, shifts that narrative toward realism:

- Liquidity can override ideology.

- Market structure matters as much as conviction.

- The Bitcoin cycle now has a new, and measurable, risk threshold: the 0.9x mNAV line.

Investors will watch Monday’s updates closely as analysts track whether mNAV stabilizes or continues slipping toward 0.9x.

Any further weakness in BTC or MSTR stock could intensify scrutiny of MicroStrategy’s balance sheet strategy heading into 2026.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}