OpenAI partners with Amazon, while Microsoft is purchasing Anthropic models… By 2025, th

December 29, 2025

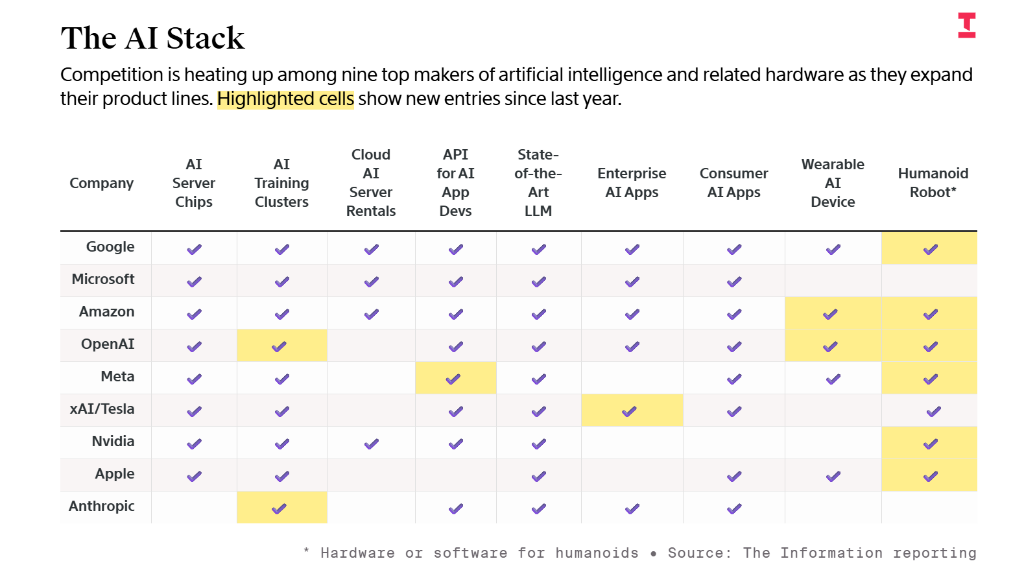

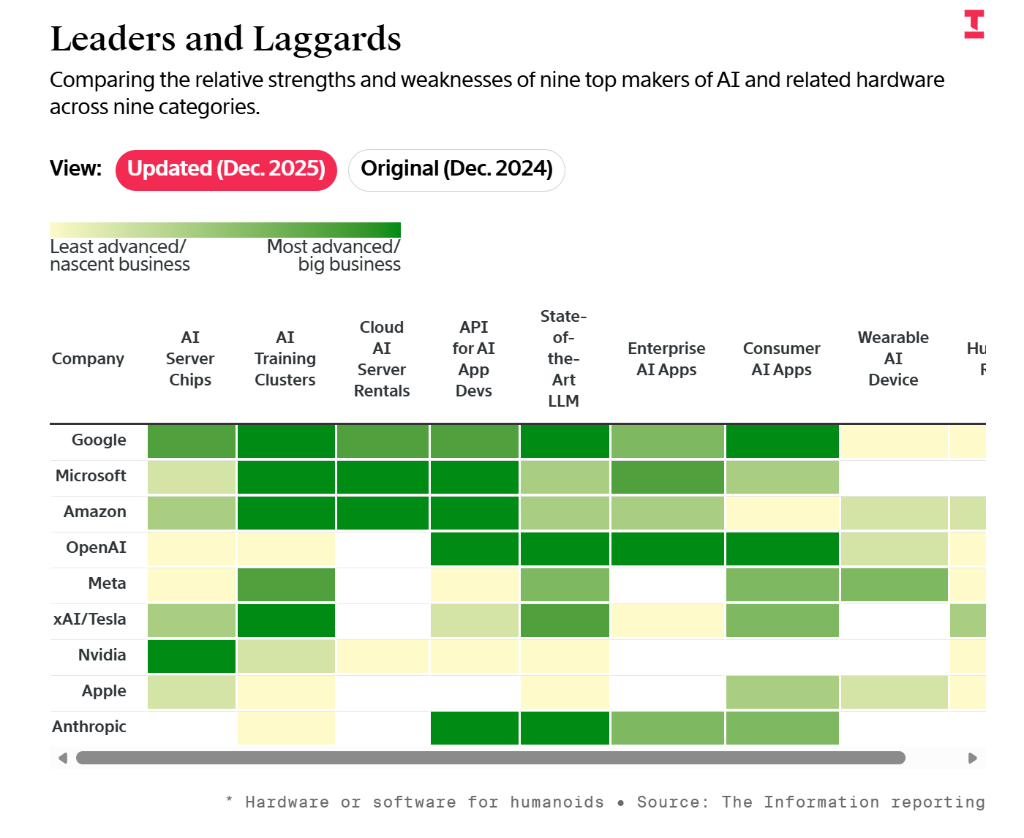

The AI industry is entering a ‘full-stack’ integration phase in 2025, with nine major players expanding their humanoid robotics and hardware portfolios while becoming entangled in more complex interdependencies. Google has emerged as a core supplier through its TPU and Gemini 3; OpenAI has reduced reliance on Microsoft via multi-cloud collaboration; Meta leads in hardware but faces setbacks in model development; xAI and Anthropic are rapidly catching up. This profound reshaping of the industrial chain is prompting all parties to redefine competitive boundaries amid efforts for independence and mutual balance.

The year 2025 is being called the year of industry consolidation for AI giants. According to a report by tech media The Information on the 29th, nine major technology companies, including Google, Meta, OpenAI, and Anthropic, have comprehensively expanded their AI ‘full-stack’ capabilities over the past year. Nearly all participants have started venturing into humanoid robotics technology, but this race for independence has instead made them more interdependent.

The industrial landscape has undergone significant changes. OpenAI has expanded its cloud service cooperation from $Microsoft (MSFT.US)$ to $Amazon (AMZN.US)$, reaching a server cooperation agreement valued at $38 billion. Meanwhile, $Microsoft (MSFT.US)$ has shifted to leasing servers to Anthropic and is purchasing Anthropic models for products like Office 365 Copilot, even though it could obtain the models for free through its partnership with OpenAI.

$Alphabet-C (GOOG.US)$ has emerged as the biggest winner in this competitive landscape, with its Tensor Processing Units (TPUs) securing a $20 billion order from Anthropic, while also negotiating a chip supply agreement with $Meta Platforms (META.US)$ . The company is set to begin large-scale delivery of $NVIDIA (NVDA.US)$ servers to OpenAI starting in 2025, becoming a technology supplier to at least five competitors.

$Alphabet-C (GOOG.US)$ has emerged as the biggest winner in this competitive landscape, with its Tensor Processing Units (TPUs) securing a $20 billion order from Anthropic, while also negotiating a chip supply agreement with $Meta Platforms (META.US)$ . The company is set to begin large-scale delivery of $NVIDIA (NVDA.US)$ servers to OpenAI starting in 2025, becoming a technology supplier to at least five competitors.

This industry reshuffle is redefining the competitive boundaries of the AI market. Companies are attempting to reduce costs and decrease reliance on key suppliers like NVIDIA by controlling more segments of the industrial chain. However, new alliances have entangled them in even more complex conflicts of interest.

Google Establishes Technological Supply Dominance

Google solidified its full-stack leadership in AI in 2025. Its TPU chip business achieved breakthrough progress, securing a $20 billion order from Anthropic while negotiating usage agreements with Meta. This marks the first time Google has sold TPUs to other cloud service providers. According to employees of competitors like OpenAI, these chips have significantly reduced costs for Google’s AI operations.

Google’s advantage in the large language model domain is equally prominent. The Gemini 3 model released in 2025, trained on TPUs, is considered state-of-the-art in the industry. In addition to technological superiority, Google also reached an agreement with long-term business partner Apple to support Siri queries, effectively replacing OpenAI’s previous role.

This supplier role places Google in a unique position. The company leases TPUs and other cloud servers to developers while providing NVIDIA servers to OpenAI on a large scale in 2025, leaving room for future sales or leasing of TPUs to OpenAI. Google currently provides technical services to at least five competitors.

OpenAI Reduces Dependence on Microsoft

OpenAI’s strategic focus for 2025 is to expand its cloud service relationships beyond Microsoft. The company has reached a server agreement valued at $38 billion with $Amazon (AMZN.US)$ , which may also include a substantial cash component, with plans to collaborate in the e-commerce sector. OpenAI also announced partnerships with $Microsoft (MSFT.US)$ Azure and $Oracle (ORCL.US)$A larger-scale agreement on cloud services.

On the hardware and product front, OpenAI has launched an ambitious plan. The company acquired a design team led by former Apple Chief Designer Jony Ive for $6.5 billion in equity to develop wearable AI devices. Although the product may not be available until 2027, OpenAI has already made strategic moves in multiple areas, including smart glasses, smart speakers, wearable pins, and digital recording devices.

OpenAI has also begun developing or controlling server clusters used for technology research and development, seeking greater autonomy at the infrastructure level. These initiatives indicate that the company is filling gaps across the AI full-stack to compete for the rapidly growing consumer and enterprise AI services market.

Meta leads in devices but lags in models.

$Meta Platforms (META.US)$ Significant progress has been made in the AI hardware device sector, with its Meta glasses placing the company well ahead of competitors like Apple in AI-driven devices, although it remains a niche market. The company also released an application programming interface (API) to sell the Llama model directly to customers, fulfilling earlier expectations.

However, Meta has faced setbacks in core technologies. Llama 4 failed to deliver substantial performance improvements and could not compete with existing leading AI models, causing the company to fall behind in developing cutting-edge proprietary models. To reverse the situation, Meta aggressively acquired talent in 2025, and improvements are expected by 2026.

Meta is seeking additional technical collaborations to address its weaknesses. The company is negotiating an agreement with $Alphabet-C (GOOG.US)$ to use Tensor Processing Units (TPUs), attempting to enhance its AI training capabilities through external chip resources. This strategic shift reflects the pressure Meta faces in developing proprietary models.

xAI and Anthropic are catching up rapidly.

xAI has made advancements in several areas. The company has improved the quality of its large language models and the NVIDIA-based training clusters; however, its LLM still lags behind those of Google, OpenAI, and Anthropic in most real-world applications. xAI’s Grok supports key functionalities for the X application, enhancing user experience, particularly in interpreting previously incomprehensible posts.

Grok appears to have attracted users interested in utilizing chatbots for adult content. xAI is developing an enterprise AI application named Macrohard—a semantic reversal of Microsoft. Another company owned by Musk,$Tesla (TSLA.US)$seems to be in a leading position among major AI companies in the humanoid robotics field, despite challenges such as the ‘hand problem’ faced by its Optimus robot.

According to undisclosed financial data, Anthropic’s product business is thriving. The company has made strides with both enterprise and individual customers and established a significant partnership with Microsoft—Microsoft leases NVIDIA servers for them while incorporating Anthropic models into products like Office 365 Copilot. Anthropic has also embarked on an ambitious plan to develop or control server clusters.

Humanoid robots emerge as a new battleground.

The year 2025 can be called the Year of Robotics, at least for major AI companies. While Anthropic, Meta, and xAI are refining their AI hardware and software product lines, nearly all participants have begun developing humanoid robotics technology.

This shift reflects not only the current competitive landscape of AI but also the vision of humanoid robots operating in every factory and household. Google, Amazon, and OpenAI have all taken steps to develop humanoid robot software or hardware, although these efforts remain in their early stages and face significant challenges. Google, Amazon, and NVIDIA currently seem to focus primarily on software development.

$Amazon (AMZN.US)$ has also made significant advancements in wearable AI devices, advancing in the form of augmented reality glasses. These emerging industries represent the next growth area that AI companies are eager to participate in, while aiming to capture more revenue or achieve long-term cost savings by controlling a more complete AI ‘full-stack.’

Microsoft’s chip progress and NVIDIA’s adjustments

$Microsoft (MSFT.US)$ The only notable progress in the server chip domain comes from its ongoing development of the Maia chip, which still lags behind most competitors. The company’s strategy focuses more on adjustments in cloud services and partnerships—continuing as OpenAI’s primary cloud service provider while expanding cooperation with Anthropic.

NVIDIA has exited direct competition with Amazon Web Services (AWS), Google Cloud, and Microsoft Azure through recent restructuring, though it has not completely left the market. This adjustment reflects the intense competition in the cloud services market and the repositioning of industrial divisions.

Despite efforts by various companies to reduce reliance on key suppliers such as NVIDIA, the company’s GPUs remain central to AI training. Google, Microsoft, and Amazon are all offering server rental services based on NVIDIA chips to other companies, underscoring the enduring importance of this chipmaker within the industry chain.

Editor/Doris

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}