Tesla preview: Narrative matters more than numbers

April 22, 2026

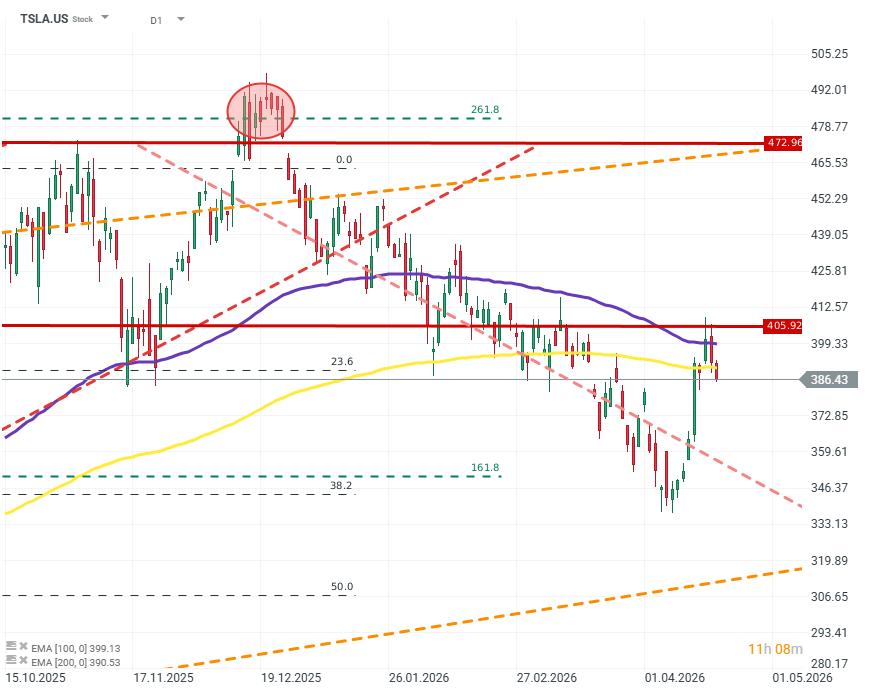

Tesla shares have fallen as much as 30% from their peak at the deepest point of the correction. Ahead of earnings, however, sentiment toward the company has clearly improved—despite signals of difficulties that can be seen in vehicle delivery reports. Do investors have something to wait for?

TSLA.US (D1)

Production and delivery reports point to a large, fundamental problem with Tesla’s business model. The company delivered about 350k vehicles versus production of about 400k. This implies a significant gap between the company’s capacity and actual demand. Creating demand for the product will be much harder than expanding production. Source: xStation5

Expectations for the company as a whole are as follows:

- Revenue: USD 22 billion

- EPS: USD 0.36–0.37

- Gross margin: 17.5%

However, Tesla is a complex and unconventional entity, and market expectations and reactions may prove equally complex and unconventional. Beyond the company-level results, it is also worth paying attention to individual business segments.

The most important segment, automotive, remains under pressure, and nothing indicates that the situation is set to improve. Still, if the company manages to deliver revenue growth, or even better, margin expansion, that could provide significant room for the stock to rise.

The energy systems segment looks much better and is performing strongly on nearly every front, but it will likely remain too small to have a meaningful impact on the company’s overall results.

What will probably determine the market’s reaction to the earnings, however, are the robotaxi, robotics and/or semiconductor segments.

Robotaxis are expected to face a breakthrough moment: the service has been launched in Dallas and Houston, and the long-awaited “Cyber Cab” is supposed to enter production in the coming weeks.

The “Optimus” robot line remains a mystery. Profitability and demand for the company’s products in this area are still a major question mark.

Today’s “wild card” is semiconductor manufacturing and the “terra-fab” initiative. Any tangible success from this initiative could trigger euphoria, while pessimism, caution, or capex above expectations could crush any enthusiasm.

If such signals appear, investors will scrutinize any mentions of Tesla’s cooperation with SpaceX and/or xAI.

The key takeaway ahead of Tesla’s earnings is that, for this company, the share price is likely to be driven more by narrative than by financial data. Promises alone may be enough for the stock to start moving back toward its highs, while disappointment, both in the company’s actual capabilities and in its stated plans and intentions, could crush any positive sentiment.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}