Think AWS Is Losing To Azure and Google Cloud? You Need To Hear This Quote From Amazon CEO

February 8, 2026

Amazon is still the cloud computing leader.

It’s no secret that Amazon (AMZN 5.49%) has been losing market share in cloud infrastructure to Alphabet’s (GOOG 2.48%) (GOOGL 2.46%) Google Cloud and Microsoft (MSFT +2.00%) Azure for years now.

That trend continued in 2025. Amazon reported a respectable 20% growth at AWS, but that was well behind Google Cloud at 36%, and Microsoft, which operates on a different fiscal calendar, but reported 39% growth in Azure in its most recent quarter.

Amazon invented cloud computing, or infrastructure-as-a-service (IaaS), as a business more than 20 years ago, and it has been the leader ever since, but the recent gains from Alphabet and Microsoft underscore the larger narrative in AI that Amazon has fallen behind its hyperscaler peers.

However, Amazon CEO Andy Jassy seems to be tired of hearing that, as he gave a robust defense of AWS and reasserted its cloud leadership on Amazon’s recent earnings call.

Jassy told investors, “As a reminder, it’s very different having 24% year-over-year growth on a $142 billion annualized run rate than to have a higher percentage growth on a meaningfully smaller which is the case with our competitors. We continue to add more incremental revenue and capacity than others, and extend our leadership position.”

He also noted that AWS clocked its fastest revenue growth in the last 13 quarters at 24%, and its chips business, led by Graviton and Trainium, which are designed for AI, have reached $10 billion in annual revenue run rate, growing triple digits.

Image source: Getty Images.

Amazon is still the cloud leader

As Jassy said, AWS added more than $21.2 billion in revenue in 2025, compared to Google Cloud, which grew by $15.5 billion.

In Microsoft’s fiscal 2025, which ended in June 2025, Azure grew by roughly $19 billion. AWS is still more than double the size of Google Cloud and significantly larger than Azure.

Amazon is also preparing to outspend its rivals in capital expenditures, targeting $200 billion this year, predominantly for AWS, inclusive of AI workloads, showing it has no intention of yielding that lead.

In addition to its revenue advantage, AWS also generates significantly more profit than its rivals do. In 2025, AWS operating income rose to $45.6 billion, compared to just $13.9 billion for Google Cloud.

Amazon

Today’s Change

(-5.49%) $-12.22

Current Price

$210.47

Is Amazon a buy?

Amazon stock dove after its earnings report on Thursday night. The company reported results in line with estimates, but investors seemed to balk at the $200 billion capex forecast, though Microsoft and Alphabet both received similar responses.

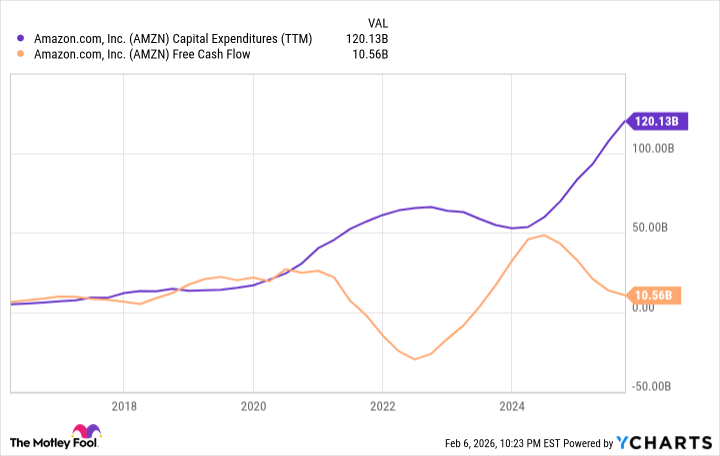

Amazon has been through this kind of cyclical capex spend before in both its cloud computing and e-commerce businesses, and it’s paid off. As you can see from the chart below, free cash flow fell sharply after its warehouse ramp during the pandemic, and it’s pulling back again as it accelerates the AWS buildout.

AMZN Capital Expenditures (TTM) data by YCharts

The company generated $139.5 billion in operating cash flow in 2025, meaning the $200 billion target will almost certainly lead to negative free cash flow in 2026.

However, that shouldn’t distract from Amazon’s solid execution. While its results might have only matched expectations, they were still strong. Revenue in the quarter rose 14% to $213.4 billion, and operating income was up 18% to $25 billion.

The stock now trades at a price-to-earnings ratio of less than 30, though that is based on generally accepted accounting principles (GAAP) earnings that include $15 billion in other income, likely from gains in its equity holdings.

Adjusting for that, Amazon looks fairly valued, and the sentiment around the spending boom seems likely to limit the stock’s upside.

That’s not a reason to sell, but Amazon’s upside potential looks limited until it can show its spending boom is paying off.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}