This Is One of the (Very Few) Downsides of Buying Index Funds Like SPY

March 18, 2026

The biggest reason for owning an index fund like the SPDR S&P 500 ETF Trust (SPY 1.40%) or the Vanguard S&P 500 ETF (VOO 1.38%) is always sound. That is, by owning a cross-section of the market’s major companies, you get lots of diversification. That doesn’t mean your position won’t occasionally lose ground, since stocks tend to move higher or lower as a herd. If you’re patient, though, the strategy pays off because you’re plugged into the market’s inherent long-term bullishness.

But every now and then, circumstances can cause index investing to work against you.

That’s what happened beginning late last year. Since Nov. 20, the aforementioned SPYders, as well as the S&P 500 (^GSPC 1.36%), have barely broken even (up 1.5%), even though seven of the market’s major sectors have logged nice gains, while its four other key industry groupings have suffered only slightly worse performances.

Here’s what you need to know.

Image source: Getty Images.

Not as well-balanced as you think it’s supposed to be

It seems like a mathematical impossibility — if a well-diversified mutual fund or exchange-traded fund holds stocks from every sector, it should dish out the average performance of those sectors.

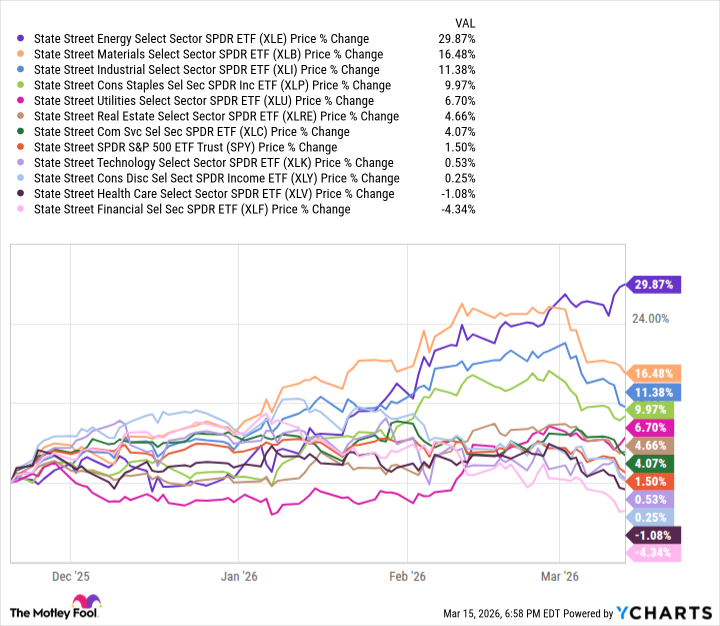

Yet that’s clearly not happening here. As the graphic below illustrates, since Nov. 20, while the S&P 500, SPY, and VOO have logged the tiniest of gains, the State Street Energy Select Sector SPDR ETF has soared nearly 30%. The State Street Materials Select Sector SPDR ETF and the State Street Industrial Select Sector SPDR ETF have also been unusually strong, up more than 16% and 11% (respectively) during this stretch. At the other end of the spectrum, the State Street Financial Select Sector SPDR ETF lost more than 4%. Healthcare, technology, and discretionary stocks have all lagged the S&P 500 over the course of the past four months.

The average performance of these 11 sectors during this time frame? A gain of 7.1% — not bad for four months. Yet these ETFs and the underlying index haven’t done much better than break even.

What gives? It’s pretty simple, actually: The S&P 500 and its exchange-traded funds aren’t sector-balanced. These are cap-weighted funds, and only cap-weighted. The table below lays out the relative weighting of each major sector to the index and, therefore, the relative impact of any changes in these sectors’ values on the S&P 500’s value.

| Sector | Weighting of S&P 500 |

|---|---|

| Technology | 33.4% |

| Financials | 12.2% |

| Telecom | 10.6% |

| Healthcare | 9.9% |

| Industrials | 9.5% |

| Discretionary | 8.9% |

| Consumer staples | 5.3% |

| Energy | 3.7% |

| Utilities | 2.5% |

| Basic materials | 2% |

| Real estate | 2% |

Data source: State Street Investment Management.

Connect the dots. SPY and VOO have been disappointing of late despite strong performance from sectors like energy and materials because those sectors are underrepresented. Simultaneously, the financial and technology stocks that have lost the most ground since late November account for a disproportionately greater share of the S&P 500.

It matters enough to merit a strategic response

None of the major market indexes is ever perfectly balanced (sector-wise), for the record. And most of the time, this imbalance doesn’t really matter; as noted above, most stocks tend to rise and fall together regardless of their sector. The past several weeks have been pretty unusual.

Nevertheless, if you’re a fan of index investing, you need to know this sort of thing is possible. It may even be something you want to plan for, particularly when different sectors reach extreme valuations, or new geopolitical tensions rattle a particular sliver of the market.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}