U.S. Private Equity Market Size, Share & Growth, 2034

May 6, 2026

U.S. Private Equity Market Size

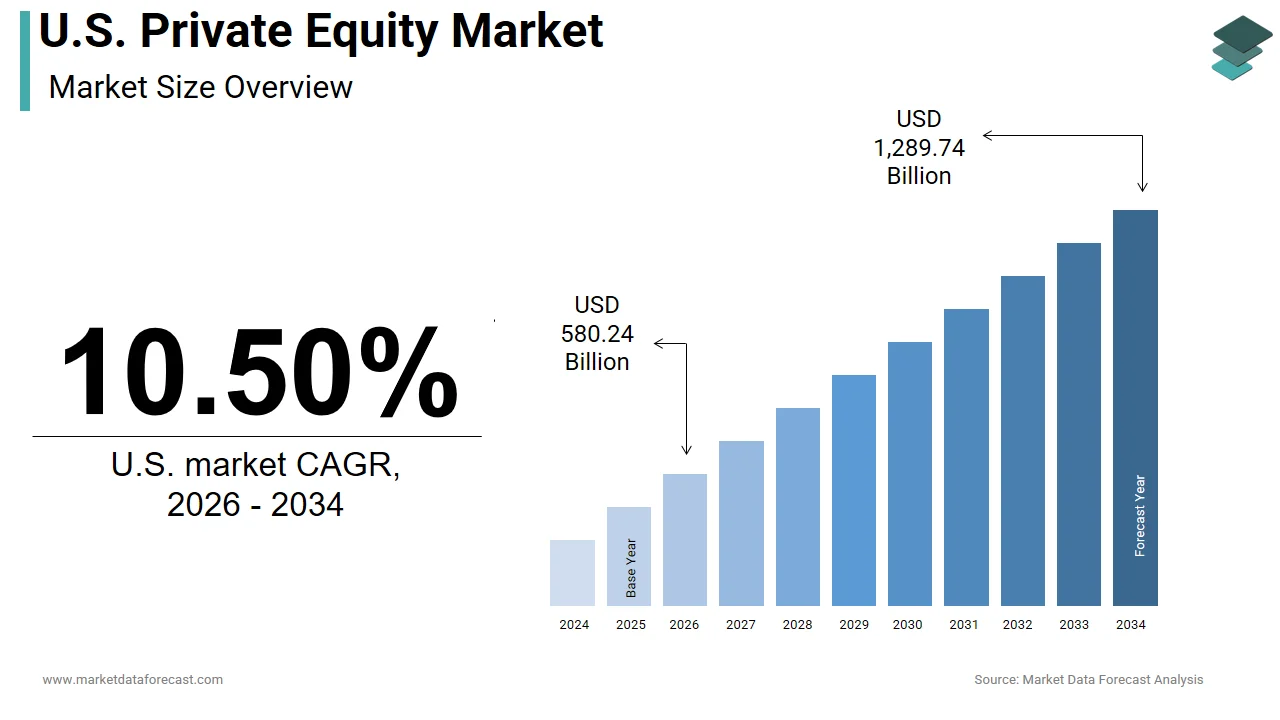

The size of the U.S. private equity market was worth USD 525.10 billion in 2025. The market is anticipated to grow at a CAGR of 10.50% from 2026 to 2034 and be worth USD 1,289.74 billion by 2034 from USD 580.24 billion in 2026.

The United States is likely to maintain its global leadership in alternative investments for the next few years as firms adapt to shifting interest rate environments. Private equity represents a sophisticated ecosystem of alternative investment firms that acquire ownership stakes in private companies or take public companies private to restructure and enhance their value. This sector plays a pivotal role in the national economy by providing capital for growth operational improvements and strategic expansions across diverse industries. The market is characterized by the pooling of funds from institutional investors such as pension funds endowments and high net worth individuals to execute leveraged buyouts venture capital investments and growth equity deals. According to the Federal Reserve, private equity assets under management reached $8.2 trillion in 2023, reflecting the substantial scale of capital deployment. Furthermore, according to the American Investment Council, private equity backed companies contribute significantly to employment with portfolio firms employing over 12 million workers in the U.S. This extensive workforce impact underscores the sector’s influence on labor markets and productivity. The regulatory environment governed by the Securities and Exchange Commission ensures transparency and investor protection while allowing for flexible investment strategies. Interest rate fluctuations set by the Federal Reserve directly impact the cost of leverage which is a critical component of private equity transactions. As per the Chartered Alternative Investment Analyst Association, institutional allocations to alternative investments have risen steadily as investors seek higher returns in a low yield environment. The market dynamics are also shaped by exit opportunities through initial public offerings and secondary sales which determine the liquidity and profitability of investments. These structural elements define a robust and influential financial sector that drives corporate innovation and economic efficiency.

MARKET DRIVERS

Abundant Dry Powder and Institutional Capital Allocation Drive Deal Activity

The substantial accumulation of un-invested capital known as dry powder is one of the major factor driving the growth of the U.S. private equity market. Institutional investors including pension funds sovereign wealth funds and insurance companies continue to increase their allocations to private equity in search of superior risk adjusted returns compared to public markets. According to Willis Towers Watson, private equity allocations among large institutional portfolios have reached approximately 11% reflecting a strategic shift toward alternative assets. This trend is driven by the need to diversify portfolios and mitigate volatility associated with public equities. According to the Pew Charitable Trusts, public pension funds have increased their private equity holdings by 15% over the past five years to meet long term liability obligations. The availability of this capital allows private equity firms to compete for high quality assets and support portfolio companies through economic downturns. As per S&P Global, global dry powder levels exceeded $2.59 trillion with a significant portion designated for US investments. This liquidity ensures that deal flow remains robust even when traditional financing sources tighten. Furthermore the ability to deploy capital quickly provides a competitive advantage in auction processes and negotiated transactions. The consistent inflow of funds from limited partners sustains the operational capacity of general partners to identify and execute value creating initiatives. Consequently the abundance of investable capital acts as a powerful engine for market expansion and transaction volume.

Corporate Carve Outs and Divestitures Create Attractive Investment Opportunities

The rising trend of corporate carve outs and divestitures by large conglomerates is further contributing to the U.S. private equity market expansion. Multinational corporations are increasingly focusing on core competencies and shedding non-essential units to streamline operations and improve financial performance. According to EY, the value of divestiture deals in the U.S. reached $800 billion in 2023 and this indicates the scale of assets available for acquisition. Private equity firms are well positioned to acquire these units as they possess the operational expertise and capital to transform them into independent entities. According to White and Case, carve out transactions accounted for 25% of total private equity deal volume reflecting their importance in the market. These transactions often involve complex separations of IT systems supply chains and human resources which private equity firms manage effectively through dedicated operational teams. As per Deloitte, successful carve outs can generate internal rates of return exceeding 20% by unlocking hidden value and improving operational efficiency. The availability of financing through debt markets further facilitates these transactions allowing firms to leverage their equity contributions. Additionally the transition period allows private equity owners to implement strategic changes without the scrutiny of public markets. This dynamic creates a steady pipeline of investment opportunities that drive market activity and provide avenues for value creation through operational improvements and strategic repositioning.

MARKET RESTRAINTS

Regulatory Scrutiny and Antitrust Enforcement Hinder Transaction Approvals

Intensifying regulatory scrutiny and aggressive antitrust enforcement is impeding the expansion of the U.S. private equity market. Regulatory bodies such as the Federal Trade Commission and the Department of Justice have adopted a stricter stance on mergers and acquisitions particularly those involving large platforms and critical infrastructure. According to the Federal Trade Commission, the number of merger enforcement actions reached a record high in 2023, indicating a more rigorous examination process. This heightened scrutiny extends to private equity acquisitions in sectors such as healthcare technology and defense where national security and consumer protection concerns are paramount. According to Dechert LLP, the average time to complete regulatory review has extended by six months causing delays in deal timelines and increasing transaction costs. As per the Wall Street Journal, several high profile private equity deals have been abandoned or modified due to regulatory objections highlighting the risks involved. The uncertainty surrounding approval outcomes discourages some investors from pursuing large scale transactions and forces firms to allocate more resources to compliance and legal defenses. Furthermore the potential for retroactive challenges or imposed divestitures adds layers of complexity to deal structuring. These regulatory headwinds constrain the pace of deal activity and limit the scope of potential acquisitions particularly in sensitive industries. Consequently the restrictive regulatory environment acts as a significant brake on market momentum and strategic expansion.

Rising Interest Rates and Tighter Credit Conditions Increase Financing Costs

Elevated interest rates and tightening credit conditions is a significant restraint on the U.S. private equity market by increasing the cost of leverage and reducing deal valuations. Private equity transactions heavily rely on debt financing to amplify returns and the cost of borrowing directly impacts the feasibility and profitability of acquisitions. According to the Federal Reserve, the federal funds rate reached a range of 5.25% to 5.50% in 2023, the highest level in over two decades leading to higher yields on corporate debt. According to S&P Global, the volume of leveraged buyout deals declined by 30% in 2023 as higher borrowing costs compressed equity multiples and reduced purchasing power. Lenders have also become more conservative imposing stricter covenants and requiring higher equity contributions from sponsors. As per Reuters, new issuance of leveraged loans dropped significantly reflecting the reluctance of banks to extend credit in a uncertain economic environment. The increased cost of debt service reduces the cash flow available for operational improvements and dividend recapitalizations thereby lowering overall returns. Furthermore the valuation gap between buyers and sellers has widened as sellers resist price adjustments despite higher financing costs. These disconnect leads to fewer closed deals and longer holding periods for existing portfolio companies. Consequently the challenging credit environment restricts the ability of private equity firms to execute new transactions and optimize capital structures.

MARKET OPPORTUNITIES

Expansion into Middle Market Companies Offers High Growth

The expansion into middle market companies is a promising opportunity for the U.S. private equity market by accessing underserved segments with strong growth potential and less competition. Middle market firms typically have enterprise values between $50 million and $500 million and often lack the resources and expertise of larger corporations. According to the U.S. Chamber of Commerce, this segment contributes approximately 33% of the U.S. gross domestic product highlighting its economic significance. Private equity firms can add substantial value by providing capital for expansion professionalizing management teams and implementing operational best practices. According to Forbes, middle market buyouts have consistently delivered higher internal rates of return compared to large cap deals due to lower entry multiples and greater operational improvement opportunities. As per EY, the middle market is experiencing a surge in succession planning needs as baby boomer owners seek exit strategies creating a robust pipeline of acquisition targets. The fragmentation of this market allows private equity firms to consolidate platforms and achieve economies of scale. Furthermore the resilience of middle market companies during economic downturns provides stability and predictable cash flows. By focusing on niche sectors and regional leaders private equity investors can capture value through organic growth and strategic add on acquisitions. This focus on the middle market enables firms to differentiate themselves and generate superior returns in a competitive landscape.

Integration of Environmental Social and Governance Criteria Attracts Capital

The integration of environmental social and governance criteria into investment strategies offers a substantial opportunity for the U.S. private equity market by aligning with investor preferences and regulatory trends. Limited partners are increasingly prioritizing sustainability and ethical practices in their allocation decisions driving demand for ESG focused funds. According to US SIF, sustainable investing assets reached $8.4 trillion reflecting the growing importance of ESG factors. Private equity firms that incorporate ESG diligence and value creation plans can attract capital from institutional investors with strict mandates. According to Reuters, private equity firms with strong ESG frameworks report higher exit multiples and improved operational performance. As per McKinsey, ESG initiatives such as energy efficiency improvements and diversity programs can reduce costs and enhance brand reputation leading to better financial outcomes. The regulatory landscape is also evolving with increased disclosure requirements that favor transparent and responsible investment practices. Private equity firms can leverage ESG improvements to differentiate portfolio companies and appeal to socially conscious consumers and employees. Furthermore the transition to a low carbon economy creates opportunities for investments in renewable energy clean technology and sustainable agriculture. By embedding ESG principles into their investment thesis private equity firms can mitigate risks and unlock new avenues for value creation. This strategic alignment with global sustainability goals positions the market for long term growth and resilience.

MARKET CHALLENGES

Valuation Discrepancies between Buyers and Sellers Impede Deal Completion

Significant valuation discrepancies between private equity buyers and corporate sellers are a major challenge to the U.S. private equity market by stalling negotiations and reducing transaction volume. Sellers often maintain expectations based on peak market valuations from previous years while buyers adjust their offers to reflect higher interest rates and economic uncertainty. According to PwC, the gap between bid and ask prices has widened to historic levels with many deals failing to reach agreement on pricing terms. According to Bloomberg, the number of announced deals that were subsequently terminated increased by 25% in 2023 due to valuation mismatches. This standoff creates a backlog of potential transactions and forces private equity firms to hold onto dry powder for extended periods. As per the Harvard Business Review, the uncertainty regarding future cash flows and exit multiples make it difficult for both parties to converge on a fair value. Sellers may prefer to wait for market conditions to improve while buyers seek deeper discounts to compensate for increased financing costs. This impasse limits the ability of private equity firms to deploy capital and generate returns for their investors. Furthermore the prolonged negotiation process increases transaction costs and consumes managerial resources. Until market expectations align with current economic realities the valuation gap will remain a persistent obstacle to deal flow and market liquidity.

Talent Acquisition and Retention Difficulties Constrain Operational Capabilities

The difficulty in acquiring and retaining top tier talent is further challenging the expansion of the U.S. private equity market. The competitive landscape for skilled professionals in finance technology and operations has intensified driving up compensation costs and turnover rates. According to the Bureau of Labor Statistics, the turnover rate in the financial activities sector reached 15% in 2023 reflecting the instability of the workforce. Private equity firms require specialized expertise to identify deals execute transactions and manage portfolio companies effectively. According to a report from Heidrick and Struggles, the time to fill executive roles in private equity backed companies has increased by 20% due to scarcity of qualified candidates. As per McKinsey, the war for talent is particularly acute in areas such as digital transformation and data analytics which are critical for value creation. The inability to secure key personnel can delay strategic initiatives and hinder operational improvements. Furthermore the high cost of compensation packages reduces the overall profitability of investments and strains budget constraints. Retaining talent also requires robust culture and incentive structures which can be difficult to implement across diverse portfolio companies. Consequently the talent shortage acts as a bottleneck for growth and efficiency forcing firms to invest heavily in recruitment and development programs to maintain competitive advantage.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Industry, and Country. |

|

Various Analyses Covered |

Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

|

Market Leaders Profiled |

Blackstone, KKR & Co., Apollo Global Management, The Carlyle Group, TPG, Bain Capital, Warburg Pincus, Thoma Bravo, Vista Equity Partners, EQT, CVC Capital Partners, Advent International, Permira, Ardian, Hellman & Friedman, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The leveraged buyouts segment dominated the market with the highest share of the U.S. private equity market in 2025. The dominance of leveraged buyouts segment in the U.S. market can be credited to the proven ability of this strategy to generate substantial returns through operational improvements and financial engineering and the availability of debt financing that allows firms to acquire mature companies with stable cash flows using a significant portion of borrowed capital. According to S&P Global, leveraged buyout transactions accounted for approximately 60% of total private equity deal value in the U.S. in 2023 reflecting the preference for this established model. This structure enables sponsors to amplify equity returns while maintaining control over strategic decisions. Data from the Federal Reserve indicates that despite rising interest rates the corporate loan market remains robust with issuance levels supporting large scale acquisitions. The maturity of the US corporate landscape provides a vast pool of targets suitable for buyouts including family owned businesses and corporate carve outs. As per McKinsey, leveraged buyouts have historically delivered internal rates of return averaging 20% outperforming many other asset classes. The ability to implement cost reductions and revenue enhancements post acquisition further validates the model. Furthermore the exit environment for buyout backed companies remains active with consistent demand from strategic buyers and public markets. These factors collectively ensure that leveraged buyouts remain the cornerstone of private equity activity driving the majority of capital deployment and value creation in the sector.

However, the venture capital segment is growing exponentially and is estimated to showcase a CAGR of 15.4% during the forecast period in the U.S. market owing to the surge in technological innovation and the increasing need for early stage funding in sectors such as artificial intelligence biotechnology and clean energy. According to the National Venture Capital Association, venture capital investments in the U.S. reached $170 billion in 2023 highlighting the critical role of this segment in fostering entrepreneurship. The primary catalyst for this growth is the relentless pursuit of disruptive technologies that promise high scalability and transformative impact. According to Crunchbase, AI related startups alone attracted over $40 billion in funding reflecting investor confidence in next generation solutions. The ecosystem support from universities incubators and government grants further accelerates the formation of new ventures. As per the Bureau of Labor Statistics, employment in high tech industries has grown by 10% annually creating a fertile ground for venture backed expansion. Additionally the success of recent initial public offerings and secondary sales provides liquidity events that encourage reinvestment into new funds. The geographic concentration of talent in hubs like Silicon Valley and Boston also sustains momentum. These dynamics position venture capital as a high velocity segment that drives innovation and captures significant value from emerging market trends.

By Industry Insights

The technology segment commanded for the dominating share of the U.S. private equity market in 2025. The growth of the technology segment in the U.S. market is driven by the relentless pace of digital transformation and the high growth potential of software and hardware innovations. According to Forbes, technology related deals accounted for nearly 30% of total private equity transaction value in 2023 underscoring its centrality in investment strategies. Private equity firms are attracted to the recurring revenue models of software as a service companies which offer predictable cash flows and high margins. According to the Bureau of Economic Analysis, the digital economy contributes over 10% to the US GDP reflecting the substantial economic footprint of the sector. The continuous evolution of cloud computing cybersecurity and data analytics creates numerous opportunities for value creation through consolidation and operational scaling. As per Gartner, global IT spending is projected to grow by 8% annually ensuring sustained demand for technology solutions. Furthermore the ability of technology companies to scale rapidly with minimal capital expenditure makes them ideal candidates for private equity ownership. The presence of a deep talent pool and robust intellectual property protections in the U.S. further reinforces this leadership. These factors collectively establish technology as the most attractive and dominant industry for private equity investment.

On the other end, the healthcare segment is expected to exhibit a CAGR of 15.8% in the U.S. private equity market during the forecast period owing to the demographic trends, technological advancements in medical services and the aging population which increases demand for healthcare services and creates opportunities for consolidation and efficiency improvements. According to the Census Bureau, the number of Americans aged 65 and older is expected to reach 80 million by 2040 creating a sustained need for medical care. Private equity firms are actively investing in physician practices hospitals and healthcare technology platforms to capitalize on this demand. According to the American Medical Association, physician practice consolidation activities have increased by 15% in recent years as providers seek economies of scale. The integration of digital health solutions such as telemedicine and electronic health records also attracts significant investment due to their potential to reduce costs and improve patient outcomes. As per the Centers for Medicare and Medicaid Services, national health expenditure is projected to grow by 5.4% annually outpacing general economic growth. Furthermore regulatory changes and value based care models create incentives for operational improvements that private equity firms are well positioned to deliver. These structural and behavioral shifts position healthcare as the most dynamic and rapidly expanding sector for private equity capital.

COUNTRY ANALYSIS

U.S. Private Equity Market Analysis

The United States is likely to maintain its status as the world’s most robust private equity market for the next few years due to its unparalleled capital depth and legal certainty. The U.S. stands as the largest and most influential market for private equity globally. This dominant position is supported by a deep and liquid capital market a robust legal framework and a culture of entrepreneurship that fosters innovation and risk taking. The market status in the region is characterized by high levels of institutional participation and sophisticated investment strategies that drive continuous growth. A primary driving factor for this leadership is the presence of major institutional investors such as pension funds and endowments that allocate significant portions of their portfolios to alternative assets. According to the American Investment Council, public pension funds in the U.S. hold over $500 billion in private equity investments providing a stable source of capital. Furthermore the depth of the US capital markets facilitates efficient exits through initial public offerings and secondary sales which are critical for realizing returns. According to the New York Stock Exchange, the US stock market remains the most active venue for listings attracting global investors. The regulatory environment governed by clear securities laws ensures transparency and investor protection encouraging both domestic and foreign capital inflows. As per S&P Global, US based private equity firms manage the majority of global dry powder enabling them to pursue large scale transactions. Additionally the concentration of industry expertise in financial hubs like New York and Boston creates a competitive ecosystem that drives innovation. These structural advantages solidify the U.S. as the central hub for private equity activity and market development.

COMPETITIVE LANDSCAPE

The competition in the U.S. private equity market is intense and characterized by the presence of large global firms specialized boutiques and emerging managers. Major players compete on the basis of deal access capital availability and operational expertise. The market is consolidated among top tier firms that possess significant dry powder and established track records. Differentiation is achieved through sector specific focus areas such as technology healthcare or energy where specialized knowledge drives value. Firms also compete for talent seeking experienced professionals who can execute complex transactions and manage portfolio companies effectively. The rise of direct lending and alternative credit strategies has intensified competition for yield seeking investors. Exit environments play a crucial role as firms vie for optimal initial public offerings or strategic sales. Regulatory scrutiny adds complexity requiring robust compliance frameworks. Ultimately success depends on the ability to generate superior returns through disciplined investment processes and active ownership. The constant evolution of market dynamics necessitates continuous innovation and adaptation to maintain a competitive edge in this sophisticated financial sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. private equity market include

- Blackstone

- KKR & Co.

- Apollo Global Management

- The Carlyle Group

- TPG

- Bain Capital

- Warburg Pincus

- Thoma Bravo

- Vista Equity Partner

- EQT

- CVC Capital Partners

- Advent International

- Permira

- Ardian

- Hellman & Friedman

TOP PLAYERS IN THE MARKET

- Blackstone Inc stands as a preeminent global investment firm with a dominant presence in the U.S. private equity market. The company specializes in alternative asset management including private equity real estate and credit solutions. Recent actions to strengthen its market position include the strategic expansion of its secondaries business which allows investors to liquidate stakes in existing funds. Blackstone has also increased its focus on thematic investing particularly in technology and healthcare sectors to capture high growth opportunities. The firm leverages its extensive operational expertise to enhance portfolio company performance through digital transformation and cost optimization. By maintaining strong relationships with institutional investors Blackstone ensures consistent capital inflows. These initiatives reinforce its leadership role by delivering superior risk adjusted returns and fostering long term value creation for stakeholders across diverse industry verticals.

- The Carlyle Group is a major global investment firm that plays a significant role in the U.S. private equity market through its diversified investment strategies. The firm focuses on corporate private equity real assets and global credit markets. Recent actions to strengthen its market position include the acquisition of specialized advisory firms to enhance its operational capabilities and sector specific expertise. Carlyle has also expanded its presence in the middle market by launching new funds dedicated to smaller enterprises with high growth potential. The company emphasizes environmental social and governance principles in its investment process to align with investor expectations. By leveraging its global network and deep industry knowledge Carlyle identifies unique investment opportunities. These strategic moves enable the firm to adapt to changing market dynamics and sustain its competitive advantage in the evolving private equity landscape.

- KKR and Co Inc is a leading global investment firm that contributes significantly to the U.S. private equity market through its innovative deal structures and sector focus. The company engages in private equity infrastructure energy and real estate investments. Recent actions to strengthen its market position include the expansion of its insurance asset management platform which provides stable long term capital for investments. KKR has also increased its activity in the technology and media sectors by partnering with industry leaders to drive growth. The firm utilizes advanced data analytics to identify value creation opportunities within portfolio companies. By focusing on operational improvements and strategic add on acquisitions KKR enhances profitability. These efforts demonstrate the company commitment to delivering sustainable returns and maintaining its status as a key player in the competitive private equity environment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. private equity market primarily employ sector specialization and operational value creation to maintain competitive advantages. Firms focus on acquiring companies in high growth industries such as technology and healthcare where they can leverage deep expertise. Strategic initiatives include implementing digital transformation programs to enhance efficiency and scalability of portfolio companies. Investors also prioritize environmental social and governance criteria to attract capital from institutional limited partners. Diversification into credit and real assets provides stable income streams and reduces reliance on traditional buyouts. Additionally firms expand their secondary markets businesses to offer liquidity solutions and manage fund lifecycles effectively. Building robust networks with industry experts and advisors enables better deal sourcing and due diligence. These multifaceted strategies ensure sustained growth and resilience in a dynamic economic environment.

MARKET SEGMENTATION

This research report on the U.S. private equity market has been segmented and sub-segmented into the following categories.

By Type

- Leveraged Buyouts (LBOs)

- Venture Capital

- Real Estate Private Equity

- Distressed and Special Situations

- Others

By Industry

- Technology

- Healthcare

- Consumer & Retail

- Financial Services

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}