US Cannabis Market

May 14, 2025

Quick Navigation

Market Overview

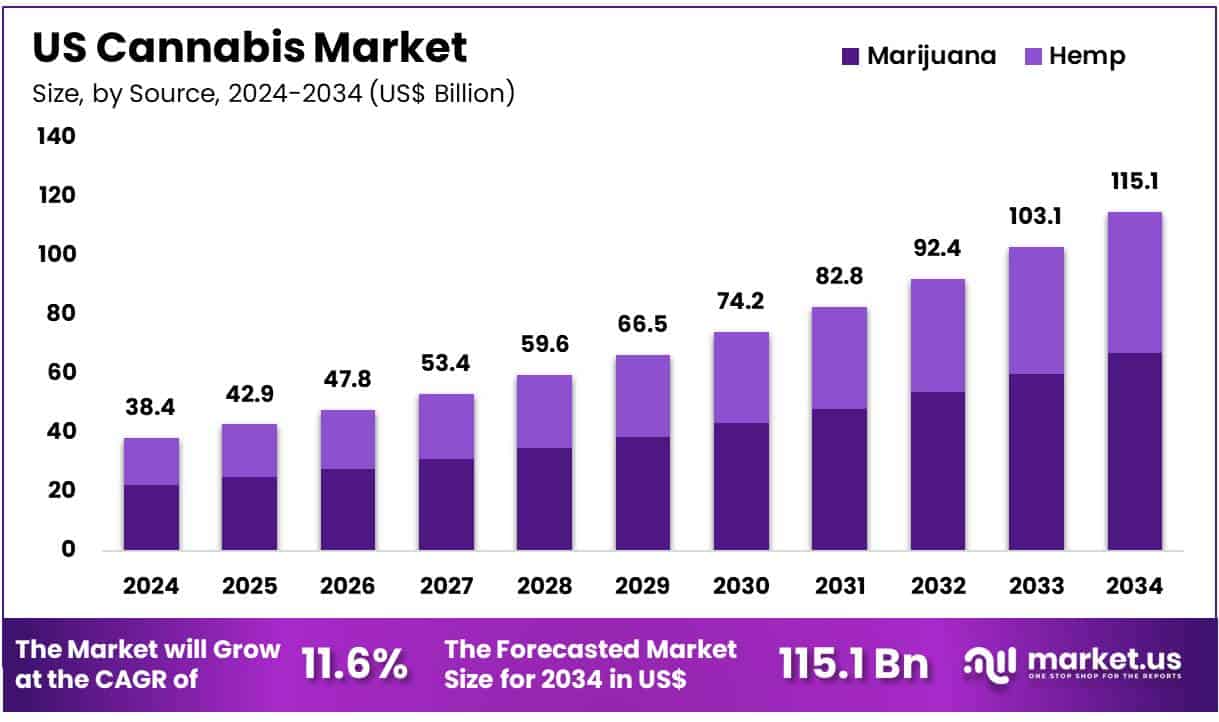

The US Cannabis Market size is expected to be worth around US$ 115.1 Billion by 2034 from US$ 38.4 Billion in 2024, growing at a CAGR of 11.6% during the forecast period 2025 to 2034.

Rising consumer demand for alternative wellness products and the growing acceptance of cannabis for medicinal and recreational use are driving the expansion of the US cannabis market. Cannabis is increasingly used for a variety of applications, including pain management, stress relief, and mental health support, as well as in wellness products such as oils, tinctures, edibles, and topicals. As states continue to legalize cannabis, both medicinal and recreational, new opportunities arise for product innovation and market diversification.

In June 2024, Rodedawg International Industries, Inc. introduced Nutrient CBD, a new line featuring five distinct products, including CBD oil tinctures, topical creams, and a roll-on, catering to consumers seeking plant-based wellness solutions. The increasing trend of cannabis-based health and beauty products, along with the rise in the number of dispensaries, supports the growth of the market.

Additionally, cannabis-infused products, such as beverages and edibles, continue to gain popularity, with consumers opting for alternative consumption methods. Technological advancements in cultivation and extraction processes improve product quality and yield, creating further opportunities for industry players.

As more research supports the therapeutic benefits of cannabis, regulatory frameworks continue to evolve, allowing for more access to cannabis products. With ongoing shifts in consumer preferences toward natural, holistic solutions, the US cannabis market is poised for continued growth and innovation.

Key Takeaways

- In 2024, the market for US cannabis generated a revenue of US$ 38.4 billion, with a CAGR of 11.6%, and is expected to reach US$ 115.1 billion by the year 2033.

- The source segment is divided into hemp and marijuana, with marijuana taking the lead in 2023 with a market share of 58.3%.

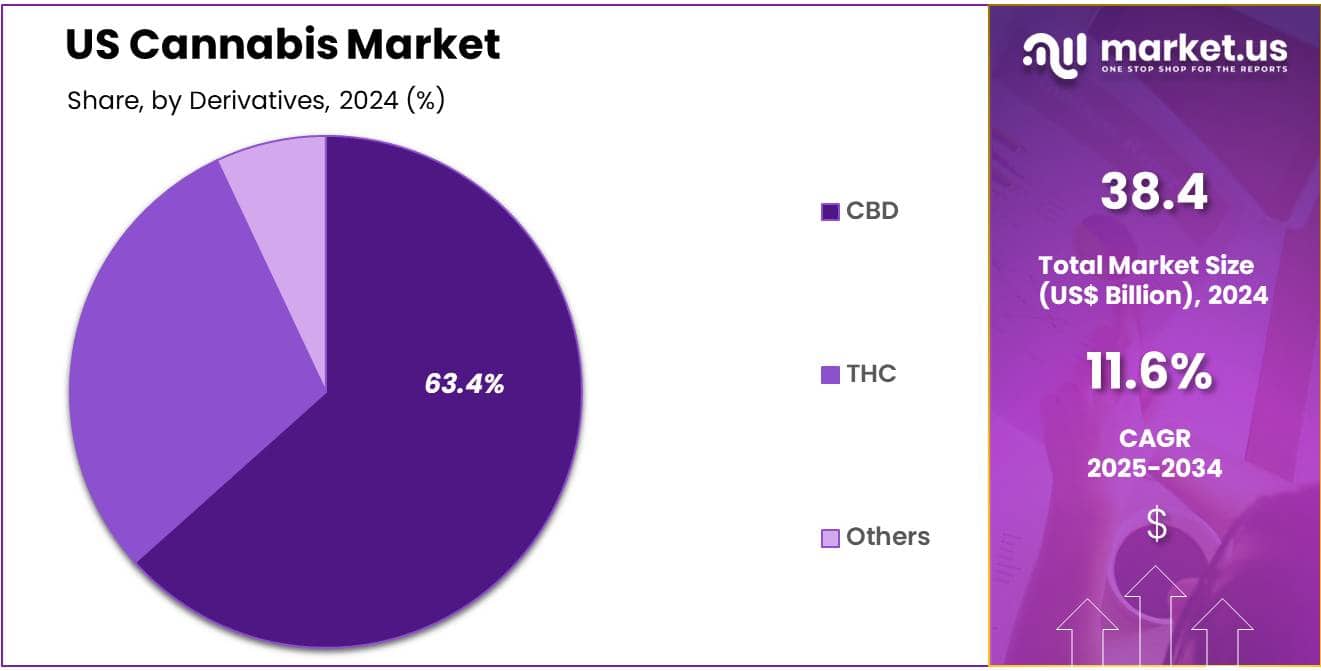

- Considering derivatives, the market is divided into CBD, THC, and others. Among these, CBD held a significant share of 63.4%.

- Furthermore, concerning the cultivation segment, the market is segregated into indoor cultivation, greenhouse cultivation, and outdoor cultivation. The indoor cultivation sector stands out as the dominant player, holding the largest revenue share of 52.5% in the US cannabis market.

- The end-use segment is segregated into industrial use, medical use, and recreational use, with the recreational use segment leading the market, holding a revenue share of 55.7%.

Source Analysis

The marijuana segment led in 2023, claiming a market share of 58.3% owing to the increasing consumer demand for both recreational and medicinal marijuana products. As more states legalize marijuana for recreational use, the market for marijuana-derived products is projected to expand significantly. This growth is driven by the growing public acceptance and changing societal attitudes toward marijuana.

Additionally, the increasing number of marijuana-based therapeutic products, such as pain management solutions and anxiety treatments, is likely to drive demand further. The expansion of the marijuana cultivation industry, along with advancements in product quality and variety, is anticipated to fuel the marijuana segment’s growth in the US cannabis market.

Derivatives Analysis

The CBD held a significant share of 63.4% as the demand for CBD-based products continues to rise across various industries, including health and wellness, cosmetics, and pharmaceuticals. The increasing consumer awareness of the potential therapeutic benefits of CBD, particularly in pain relief, anxiety reduction, and anti-inflammatory properties, is expected to drive the segment’s expansion.

As more states legalize cannabis, the market for CBD is projected to experience significant growth, particularly in the production of tinctures, oils, and edibles. The widespread popularity of CBD as a natural alternative to pharmaceutical drugs is likely to contribute to the continued growth of this segment, especially among health-conscious consumers seeking natural remedies

Cultivation Analysis

The indoor cultivation segment had a tremendous growth rate, with a revenue share of 52.5% owing to the ability to control environmental factors, such as light, temperature, and humidity, leading to higher-quality cannabis products. Indoor cultivation allows for year-round production, making it increasingly popular among growers aiming to meet the rising demand for cannabis.

As the cannabis market expands, indoor cultivation provides a reliable and efficient solution for meeting high-quality standards in both recreational and medicinal cannabis products. Additionally, the increasing adoption of advanced technologies such as hydroponics and automated growing systems is projected to boost the growth of indoor cultivation. The ability to maximize yields and maintain consistent quality is expected to drive further investment in indoor cultivation methods.

End-use Analysis

The recreational use segment grew at a substantial rate, generating a revenue portion of 55.7% as more states legalize cannabis for recreational purposes. The increasing acceptance of cannabis as a recreational product is expected to contribute to the expansion of this segment, with rising demand for products such as edibles, concentrates, and dried cannabis.

The growing number of consumers seeking cannabis for recreational use, coupled with changing attitudes toward its legalization, is likely to drive market growth. As cannabis becomes more mainstream and its legal status continues to evolve, recreational cannabis is projected to become a major driver of the US cannabis market. The expansion of retail outlets and delivery services dedicated to recreational cannabis is expected to further fuel the segment’s growth.

Key Market Segments

By Source

- Hemp

- Hemp Oil

- Industrial Hemp

- Marijuana

- Flower

- Oil & Tinctures

By Deriviatives

- CBD

- THC

- Others

By Cultivation

- Indoor Cultivation

- Greenhouse Cultivation

- Outdoor Cultivation

By End-use

- Industrial Use

- Medical Use

- Chronic Pain

- Depression & Anxiety

- Arthritis

- Others

- Recreational Use

Drivers

Increasing state-level legalization is driving the market

Increasing state-level legalization of cannabis for medical and adult recreational use is driving the US cannabis market. As more states enact laws permitting the sale and use of cannabis, they create entirely new legal markets and expand existing medical programs. This provides consumers with regulated access to cannabis products and generates significant tax revenue for state governments. The growing number of states legalizing reflects an evolving public and political acceptance of cannabis.

By early 2024, 38 states and the District of Columbia had legalized cannabis for medical use, and 24 states and the District of Columbia had legalized it for nonmedical use, significantly expanding the potential consumer base and geographic reach of the legal market. For example, Illinois reported over US$457 million in cannabis tax revenue in 2024, demonstrating the substantial economic activity generated by state-level legalization.

Restraints

Federal illegality and regulatory complexity are restraining the market

Federal illegality and regulatory complexity are restraining the US cannabis market. Despite increasing state-level legalization, cannabis remains classified as a Schedule I controlled substance under federal law. This federal prohibition creates significant challenges for cannabis businesses, including limited access to traditional banking services, restrictions on interstate commerce, and unfavorable tax treatment under IRS Code 280E, which prevents businesses from deducting ordinary business expenses.

Navigating the patchwork of diverse regulations and licensing requirements across different legal states adds further complexity and cost for operators. While the exact financial burden of federal illegality is difficult to quantify with a single government statistic, the lack of access to standard financial services and the punitive tax code significantly constrain growth and profitability for many businesses in the sector.

Opportunities

Potential for federal policy reform is creating growth opportunities

Potential for federal policy reform is creating growth opportunities in the US cannabis market. Changes in federal law, such as rescheduling or descheduling cannabis, would dramatically reshape the industry landscape. Federal reform could unlock access to traditional banking and financial services, enable interstate commerce, and potentially revise the burdensome 280E tax code, significantly reducing operational costs and fostering investment.

The possibility of such reforms attracts interest and capital to the sector, anticipating a more favorable business environment. Legislative efforts at the federal level signal this potential; as of July 2024, bills related to cannabis reform were under consideration in the US Congress, including provisions to study state legalization and regulation, indicating ongoing movement towards potential federal policy changes.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic factors influence the US cannabis market, impacting consumer spending and business operations. Economic conditions, such as inflation and changes in disposable income, directly affect consumer purchasing power for both medical and adult-use cannabis products, particularly in legal markets where purchases are often discretionary.

Inflation also increases operational costs for cannabis businesses, including expenses for cultivation, processing, packaging, and labor, pressuring profit margins. Geopolitical factors have a less direct impact but can influence the cost and availability of imported equipment and supplies used in cultivation and processing if trade relationships are affected.

Despite potential negative economic pressures on consumer spending, the cannabis market in legal states continues to generate significant tax revenue, providing a potentially stable income source for state governments even during broader economic fluctuations.

Current US tariff policies impact the US cannabis market indirectly through the cost of goods used in cultivation, processing, and retail. While direct tariffs on cannabis itself are unlikely due to federal prohibition, tariffs on imported horticultural equipment (like lighting and ventilation systems), laboratory testing equipment, processing machinery, and packaging materials increase the capital and operational expenses for cannabis businesses operating in the US.

These increased costs can affect the profitability of businesses and potentially influence the pricing of legal cannabis products for consumers. Reports in April 2025 indicated that US tariffs could impact the cost of medical devices and laboratory equipment, items relevant to cannabis testing and processing. However, these tariffs could also incentivize domestic production of some equipment and supplies, potentially leading to greater resilience in the supply chain for the US cannabis industry over the long term.

Latest Trends

Growth in social equity initiatives is creating growth opportunities

Growth in social equity initiatives is creating growth opportunities and influencing the US cannabis market. As states implement legal cannabis programs, many are incorporating provisions designed to promote social equity. These initiatives aim to address the disproportionate impact of past cannabis prohibition on marginalized communities by creating opportunities for individuals from these communities to participate in the legal industry through preferential licensing, access to funding, and reduced barriers to entry. This focus on social equity is shaping the market by encouraging diversity in ownership and ensuring that the economic benefits of legalization are more broadly shared.

While comprehensive nationwide data on social equity licenses from a single government source is not readily available, state-level data illustrates this trend; in Illinois, seventy applicants selected in social equity lotteries in 2022 were still in the process of receiving their dispensary licenses in early 2024, demonstrating the ongoing effort to implement these programs.

Key Players Analysis

Key players in the US cannabis market drive growth through strategic mergers and acquisitions, geographic expansion, and product diversification. They acquire regional operators to enhance market presence and streamline operations. Expanding into high-demand states and underserved regions allows companies to tap into new customer bases.

Diversifying product offerings, including edibles, beverages, and wellness products, caters to evolving consumer preferences. Collaborations with established brands and celebrities help build brand recognition and credibility. Additionally, investment in sustainable practices and compliance with regulatory standards ensures long-term operational success.

Curaleaf is a leading cannabis company in the US, operating in multiple states with a focus on medical and adult-use cannabis products. The company offers a wide range of products, including flower, concentrates, edibles, and topicals, under various brand names. Curaleaf has expanded its footprint through strategic acquisitions, such as the purchase of Grassroots Cannabis, which significantly increased its retail presence.

The company emphasizes innovation and customer education, aiming to provide high-quality cannabis products and services to its diverse clientele. With a commitment to community engagement and regulatory compliance, Curaleaf continues to be a prominent player in the evolving cannabis industry.

Top Key Players

- Tilray Brands

- The Cronos Group

- Organigram Holding, Inc

- Irwin Naturals

- CV Sciences, Inc

- Charlotte’s Web

- Canopy Growth Corporation

- Aurora Cannabis

Recent Developments

- In April 2023, Charlotte’s Web, a prominent US hemp company, entered a strategic partnership with AJNA BioSciences PBC, a botanical pharmaceutical developer, and British American Tobacco PLC. The collaboration focused on securing FDA approval for a full-spectrum hemp extract as a regulated botanical drug.

- In April 2023, CV Sciences, Inc. debuted its +PlusCBD Reserve Collection, introducing a premium line of extra-strength gummies. Formulated with full-spectrum cannabinoids, these products are designed to deliver potent relief for moments when heightened support is needed.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 38.4 billion |

| Forecast Revenue (2034) | US$ 115.1 billion |

| CAGR (2025-2034) | 11.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Hemp (Hemp Oil, and Industrial Hemp), Marijuana (Flower, and Oil & Tinctures)), By Derivatives (CBD, THC, and Others), By Cultivation (Indoor Cultivation, Greenhouse Cultivation, and Outdoor Cultivation), By End-use (Industrial Use, Medical Use (Chronic Pain, Depression & Anxiety, Arthritis, and Others), and Recreational Use) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Tilray Brands, The Cronos Group, Organigram Holding, Inc, Irwin Naturals, CV Sciences, Inc, Charlotte’s Web, Canopy Growth Corporation, and Aurora Cannabis. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}