Tesla Has Reclaimed Its Spot as the Leading Global EV Manufacturer, but Is the Stock a Buy?

April 19, 2026

Based on nothing more than recent headlines, it would be easy to be bullish on beaten-down Tesla (TSLA +2.96%) shares. The stock at one point had fallen 30% from its December peak largely because it lost its global lead to battery-powered electric vehicle (BEV) rival BYD Company (BYDDY 0.56%). Now it has reclaimed that lead.

There’s always more to the matter, though. Indeed, the deeper you dig, the less compelling Tesla stock gets.

Image source: Getty Images.

An encouraging headline, but…

After several months of trailing BYD’s total production of battery-only electric vehicles (or BEVs), Tesla is back on top. The iconic company delivered 358,023 EVs during the first quarter of this year, versus BYD’s count of 310,389 battery-powered electric vehicles sold.

That seems like a much-needed win for existing Tesla shareholders. But it’s not the whole story.

Today’s Change

(2.96%) $11.51

Current Price

$400.41

One of the more important footnotes to add here is that Tesla’s figure fell short of analysts’ expectations for 365,645 vehicles in the quarter. And BYD’s 310,389 was battery-powered automobiles, so that number does not include the 378,604 of its increasingly popular hybrid vehicles it sold last quarter. Tesla doesn’t manufacture hybrid vehicles.

Perhaps worse, Tesla is still losing total market share here and abroad. And in Europe, it’s losing share to BYD.

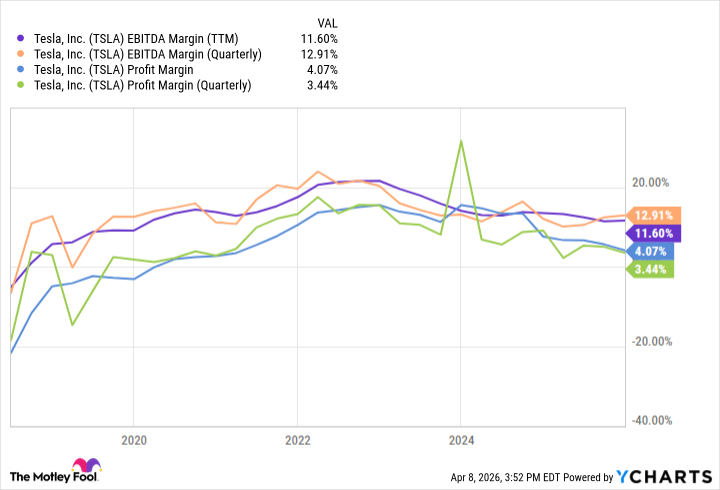

Now, losing share of an ever-growing EV market isn’t necessarily disastrous. It does present a problem that most investors aren’t accustomed to, though: Tesla’s waning pricing power stemming from a bevy of new competition. The company’s adjusted EBITDA margins have steadily slipped from 2022’s peak of nearly 24% to less than 16% last year. Investors just aren’t quite sure how to value Tesla shares under this new paradigm.

TSLA EBITDA Margin (TTM) data by YCharts

Then there’s another thing. That’s the fact that rather than figuring out a way to build more price-competitive (but higher-margin) cars and then generating demand for them, Tesla CEO Elon Musk seems to be ignoring this challenge to focus on the development of autonomous humanoid robots meant to handle household chores and other menial labor. Musk contends these artificial intelligence (AI) androids will cost less than $30,000 each, and go into commercial production sometime before the end of next year.

And perhaps they will.

However, given Musk’s penchant for overpromising, underdelivering, and also overspending, shareholders have room, reason, and the right to question the suggested timeline. Ditto for the development of Tesla’s so-called Cybercab, which is supposed to come at a price point similar to the company’s planned robot, as well as launch at around the same time.

Still too much uncertainty compared to other options

Never say never. Tesla may well change the world with the successful launches of an AI-powered robot and a cost-effective self-driving robotaxi. The company’s electric vehicle business might hold onto its market share, and even start widening its profit margins again.

But interested investors will need far more proof that this could happen than just a positive quarter on the EV front. Other electric vehicle manufacturers aren’t going to simply go away. They’re going to get better, in fact, and become more competitive with Tesla as well as BYD.

It matters because BEVs are still Tesla’s bread-winning business. That’s likely to remain the case for at least the next couple of years. It could remain the case for the next several years, in fact.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}

{kind=link}