Tesla vs Ford: One Is a Disrupter While One Is Quietly Building Legacy

May 5, 2026

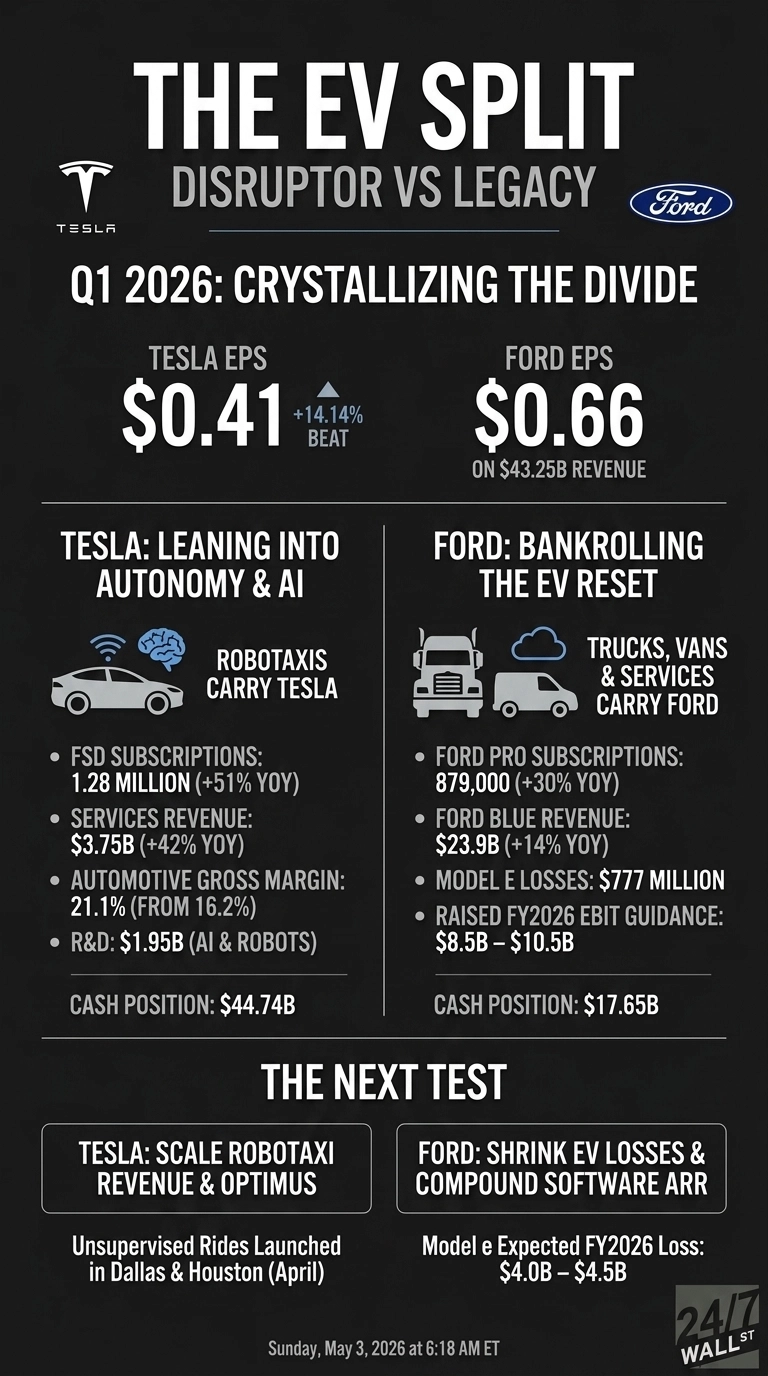

Tesla (NASDAQ: TSLA | TSLA Price Prediction) and Ford (NYSE: F) just reported first quarter results that crystallize the EV split. Tesla leaned into autonomy, AI compute, and humanoid robots while squeezing more margin from its existing fleet. Ford leaned on F-Series trucks, commercial fleets, and software subscriptions to bankroll a costly EV reset. Same industry, very different playbooks.

Robotaxis Carry Tesla. Trucks and Vans Carry Ford.

Tesla’s automotive gross margin expanded to 21.1% from 16.2% a year ago, helped by lower material costs and higher selling prices. EPS came in at $0.41 on revenue of $22.387 billion, with 1.28 million active FSD subscriptions, up 51% year over year. That subscription engine is doing real work. Services revenue jumped 42%, while energy storage slipped 12%, a reminder that battery pack capacity remains the bottleneck.

Ford’s quarter looked nothing alike. EPS hit $0.66 on revenue of $43.25 billion, lifted by Ford Blue’s 14% revenue growth and a $1.3 billion one-time IEEPA tariff benefit. Ford Pro’s commercial software base reached 879,000 paid subscribers, up 30%. Model e still bled, posting a $777 million loss on barely growing sales.

Disruptor Doubles Down. Legacy Triages.

Tesla launched unsupervised Robotaxi rides in Dallas and Houston in April, taped out its AI5 inference processor, and is preparing an Optimus line at Fremont designed for 1 million robots/year. R&D climbed to $1.95 billion. That is a long-duration bet with real burn risk if autonomy timelines slip.

| Lens | Tesla | Ford |

| Core Bet | FSD, Robotaxi, Optimus | F-Series, Bronco, Ford Pro software |

| EV Economics | 21.1% auto gross margin | Model e losing $777M/quarter |

| 2026 Capex Focus | AI compute, semis, LFP cells | $1.5B Ford Energy, UEV platform |

| Cash Position | $44.743B | $17.649B |

Ford’s response is more surgical. CEO Jim Farley said the quarter reflects “the momentum of the Ford+ plan” as the company enters “one of the most intensive product, software and physical services rollouts in our history.” Management raised full-year adjusted EBIT guidance to $8.5 billion to $10.5 billion, even with commodity headwinds running near $2 billion.

The Next Test Is Autonomy Revenue and EV Discipline

I will be watching whether Tesla can turn unsupervised Robotaxi pilots into recurring revenue before AI capex strains free cash flow further. The University of Michigan consumer sentiment index sat at 53.3 in March, a pessimistic backdrop for any premium vehicle.

Keep an eye on whether Ford’s Universal EV platform can shrink Model e’s expected $4 billion to $4.5 billion 2026 loss while Ford Pro keeps compounding software ARR.

Why I Lean Toward Ford for Cash Flow, Tesla for Optionality

Personally, I think both can work, just for different investors. If you want a steadier setup with a 4.97% dividend yield and a forward P/E around 8, Ford fits. The Ford Pro margin at 11.4% and 879,000 paying software users tell me the recurring revenue thesis is real, even as Model e drags. Negative free cash flow of $1.874 billion in Q1 keeps me cautious.

If you can stomach a $1.468 trillion market cap pricing in autonomy that has not scaled yet, Tesla offers the optionality. Reddit’s wallstreetbets crowd is openly leveraged on it, with one widely upvoted post titled “Going Full regard on TSLA. Borrowed 300k+”. I would wait for clearer Robotaxi unit economics before adding exposure.

Search

RECENT PRESS RELEASES

Related Post

{kind=link}

{kind=link}

{kind=link}